A Guide to the Nonprofit Statement of Activities

Jun 26, 2023

Think of the nonprofit statement of activities as the financial story of your mission over a specific period. It’s not just about profit and loss; it’s about impact and stewardship. While a for-profit business has an income statement that zeroes in on the bottom line, this report shows how you’ve used your resources to make a difference.

This is the document you’ll hand to donors, board members, and grantors to show them exactly how their support fueled your work.

Your Nonprofit's Financial Story

Let's use an analogy. Imagine your organization is on a year-long road trip to deliver clean water filters to a remote village. The statement of activities is your trip's logbook. It doesn't just show that you arrived; it details every part of the journey—the donations that bought the gas, the volunteer hours that drove the truck, and the cost of the filters themselves.

This financial report answers the most critical questions about your operations for a set period, like a quarter or a full fiscal year. It offers a dynamic look at your financial health, perfectly complementing the static snapshot you get from the statement of financial position (your balance sheet).

Beyond Just Profit and Loss

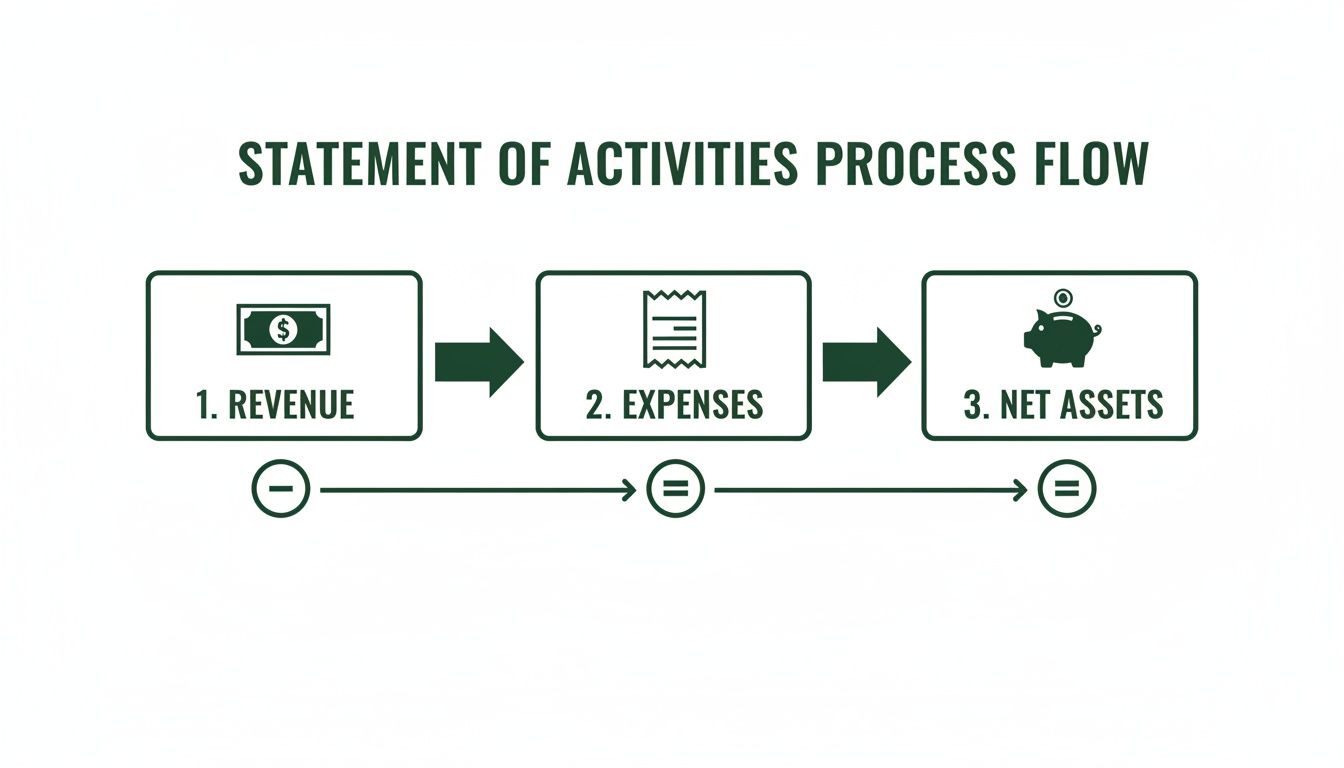

For a regular business, the math is simple: Revenue - Expenses = Profit. But a nonprofit’s goal isn’t to hoard cash; it's to create change. The statement of activities reflects this core difference by focusing on the change in net assets.

This essential report serves a few key purposes:

Shows Financial Performance: It transparently lists every revenue source—from individual donations and grants to program service fees—and every expense, giving a clear picture of your financial operations.

Demonstrates Stewardship: It tells stakeholders exactly how their money was put to work, building the trust needed for long-term support.

Tracks Net Asset Changes: It calculates whether your net assets grew or shrank over the period, which is a vital indicator of your financial sustainability.

At its core, the nonprofit statement of activities answers one fundamental question: How did our financial resources change as we worked to fulfill our mission this year?

The Core Equation

The logic behind the statement is actually quite simple. It all boils down to a powerful formula: Total Revenues - Total Expenses = Change in Net Assets.

That final number tells a huge part of your story. A positive change means you brought in more support than you spent, strengthening your financial footing for the future. A negative change shows expenses outpaced revenue—which isn't always bad, especially if you planned a major program expansion, but it’s something that needs careful management.

Getting comfortable with this simple equation is the first and most important step to mastering your nonprofit's financial narrative.

Cracking Open the Statement of Activities: What's Inside?

To really understand what your statement of activities is telling you, you have to get to know its main parts. Think of it as a financial story. This report is built around four key sections that, together, paint a clear picture of your nonprofit's financial journey over a specific time, like a fiscal year or a quarter.

These four key sections are:

Revenue: All the money that came into your organization.

Expenses: All the costs you paid out to run your programs and keep the doors open.

Net Assets: What's left over, separated by whether donors put strings on the funds.

Change in Net Assets: The bottom line—did your financial position get stronger or weaker?

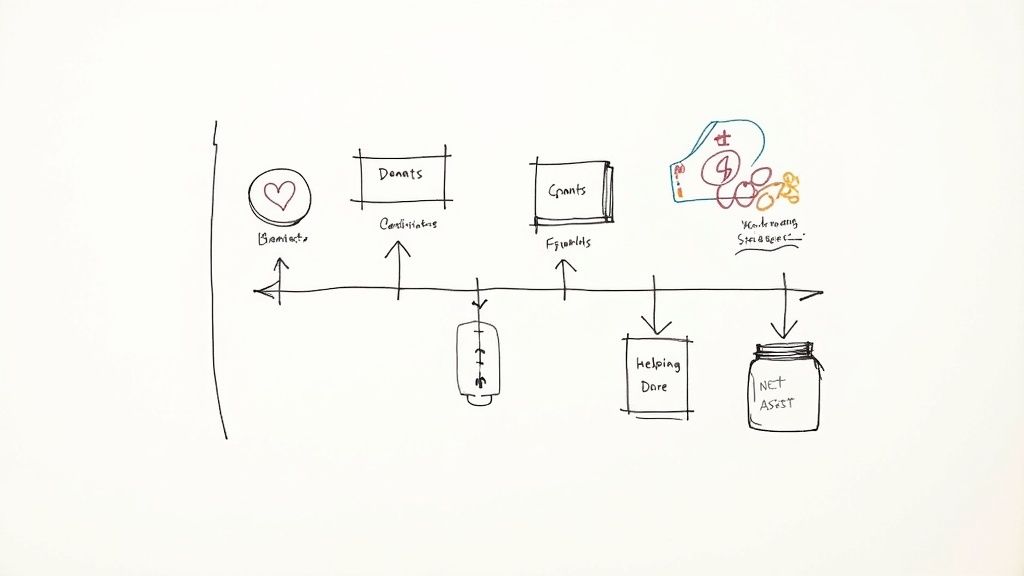

Understanding Your Revenue Streams

Revenue is the fuel for your mission. It’s all the money flowing into your organization, and it comes from a lot of different places. You might see income from individual donations, grants from foundations or the government, membership fees, or even ticket sales for a fundraising event.

Tracking these different streams is non-negotiable for good financial health. For example, total charitable giving in the U.S. hit a huge $592.50 billion in 2024, which was a 6.3% jump from the year before. This shows just how important it is to have a system for tracking every dollar. We’re also seeing that recurring monthly donations now make up 31% of all online revenue for nonprofits, giving them a steady source of unrestricted cash.

Program Expenses vs. Supporting Services

After showing where the money came from, the statement breaks down where it all went. Expenses aren't just one big lump sum; they’re separated by their purpose. This gives your board, donors, and grantmakers a transparent look at how you’re investing in your mission.

Your expenses will generally fall into two main categories:

Program Services: These are the costs that are directly tied to your mission-driven work. If you run a food bank, this includes the cost of the food itself, running the warehouse, and paying the staff who distribute it.

Supporting Services: This is the overhead that makes your programs possible. It includes management and general costs (like accounting, HR, and rent) and fundraising expenses (like writing grants or hosting donor events).

The difference between program and supporting services is critical. It answers the big question donors always have: "How much of my money is actually going to the cause versus keeping the lights on?"

To help you understand these components at a glance, here’s a quick breakdown:

Key Sections of the Statement of Activities Explained

Component | Description | Example |

|---|---|---|

Revenue | The total income received from all sources, often separated by type (grants, donations, etc.). | A $50,000 grant from a local foundation for a new after-school program. |

Program Expenses | Direct costs of carrying out the organization's mission and delivering services. | Salaries for teachers, art supplies, and snacks for that after-school program. |

Supporting Expenses | Overhead costs that support the organization as a whole, including fundraising and administrative costs. | The accountant's salary, office rent, or costs for a fundraising gala. |

Change in Net Assets | The "bottom line" showing the net result of all revenue and expenses for the period. | If total revenue was $200,000 and total expenses were $180,000, the change is $20,000. |

This table provides a simple map for reading the statement and understanding how each piece contributes to the overall financial picture.

The Role of Net Assets

Here’s where nonprofit accounting really differs from the for-profit world: net assets. Instead of "equity," nonprofits use this term to describe what's left after subtracting liabilities. And, most importantly, these assets are split into two classes based on donor intent.

Net Assets Without Donor Restrictions: This is your flexible funding. You can use these funds for anything that supports your mission, from paying the electric bill to launching a new initiative. They are absolutely vital for day-to-day operations.

Net Assets With Donor Restrictions: These funds come with strings attached. A donor might give you money specifically for a new building, or a grant might be restricted to funding a summer camp. You can only use these funds for their designated purpose.

Keeping these two categories straight is the foundation of accountability and trust with your donors. The best way to start is by setting up a solid nonprofit chart of accounts that allows you to classify every dollar correctly from the moment it comes in.

How to Report Revenue and Donor Support

In the world of nonprofit accounting, not all income is treated the same, and your nonprofit statement of activities needs to make those differences crystal clear. Think of it as telling the story of your funding—and getting it right is fundamental to building trust. The first step is to separate your income into two main buckets.

First, you have contributions. These are gifts freely given, like donations from individuals or foundation grants, where the donor doesn't expect anything of significant value back. Then, there's earned revenue, which is money you make by selling a good or service. This could be anything from ticket sales for a gala to fees for a class you offer.

Drawing this line in the sand is crucial. It shows everyone—from your board to your donors—whether your mission is fueled primarily by community generosity or by the services you provide.

The Key Concept of Releasing Funds from Restriction

One of the most powerful things the statement of activities does is show how and when you use restricted donations. This is handled through a process called "net assets released from restriction." It sounds a bit technical, but an example brings it to life.

Let's say a generous donor gives your church $10,000, but with one condition: the money must be used to replace the old, leaky roof. The moment you receive that check, the $10,000 is recorded as a "net asset with donor restrictions." It's locked away, legally and ethically, from being used for anything else, like staff salaries or utility bills.

That money stays in the restricted column of your statement until the roofing project is complete. Once you pay the contractor for the new roof, the funds are officially "released." In your accounting, you’ll see a transfer of $10,000 from the restricted column over to the unrestricted column, where it's immediately matched against the roofing expense.

This chart gives you a bird's-eye view of how money flows through a nonprofit, from the moment it comes in the door to how it ultimately affects your financial position.

It’s a simple but elegant system that clearly shows how revenue is put to work to cover expenses, which in turn changes the organization’s overall net assets.

Why This Process Matters for Trust

Getting this "release" process right is more than just good bookkeeping; it’s about keeping your promises. It provides undeniable proof to donors that you honored their wishes and used their money exactly as they intended.

Releasing assets from restriction isn't just an accounting step; it's the moment you fulfill your promise to a donor, turning their restricted gift into tangible mission impact.

This level of financial accountability builds the kind of confidence that keeps donors coming back. And it seems to be working. A recent survey found that 62% of nonprofits saw their revenue grow, with 54% expecting major gift donations to increase. This shows a clear link between strong stewardship, proven through transparent reporting, and the ability to secure the funding you need to thrive. For more insights, you can explore the latest nonprofit revenue trends and see how the sector is faring.

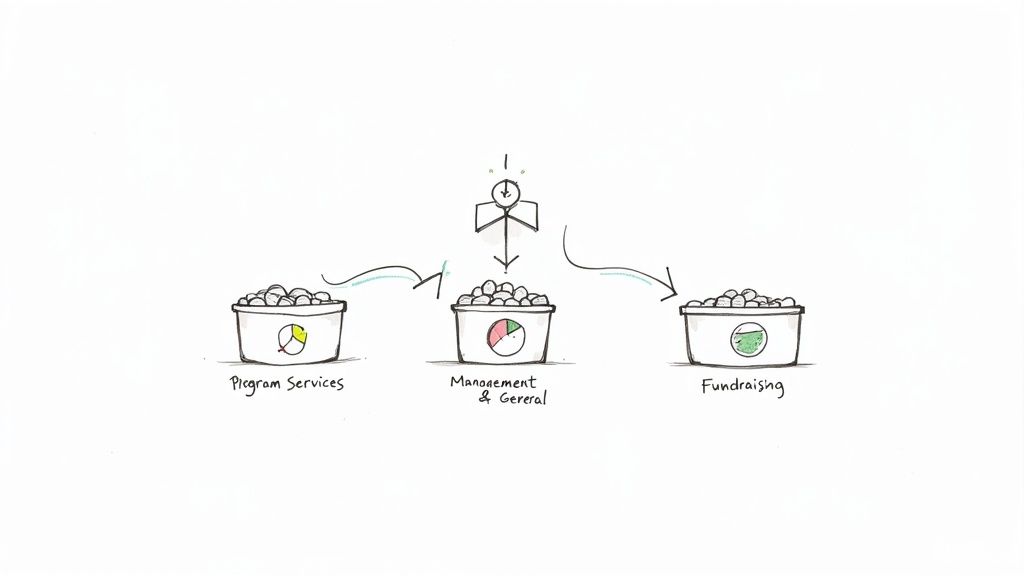

Analyzing Your Functional Expenses

Your expenses tell a story just as powerful as your revenue. On the statement of activities, that story reveals exactly how you're investing in your mission. This is done through a process called functional expense allocation, which means sorting every dollar you spend into one of three specific buckets.

Think of it like organizing your personal budget. You probably have categories for "Needs" (like rent and groceries), "Wants" (entertainment), and "Savings." Functional expense allocation does the same for your nonprofit, giving everyone—from your board to your donors—a clear picture of where the money is actually going.

The Three Buckets of Spending

Every single expense, from a key staff member's salary down to a ream of printer paper, has to be assigned to its primary purpose. This breakdown is a standard requirement under GAAP (Generally Accepted Accounting Principles) and is absolutely critical for transparency.

These are the three functional categories you'll use:

Program Services: These are the costs that directly fuel your mission. If you run a food pantry, this bucket includes the cost of food, rent for the warehouse, and the salaries of the team distributing meals.

Management and General: This covers the essential overhead that keeps the lights on and the organization running smoothly. Think of costs for accounting, HR, and the executive leadership team that steers the ship.

Fundraising: This includes all the expenses you incur to generate contributions. That could be the cost of writing grants, hosting a fundraising gala, or running a direct mail campaign.

This isn't just a box-ticking exercise for your accountant. It’s a powerful strategic tool. Watchdog groups like Charity Navigator look closely at this breakdown to rate a nonprofit's efficiency, so a clear and accurate allocation demonstrates that you are responsible stewards of donor funds.

The Challenge of Shared Costs

Things can get a little tricky when you have shared expenses. For instance, what about the salary of an executive director who spends 60% of their time on program oversight, 20% on administration, and 20% on fundraising? The answer is to split, or allocate, their salary across all three categories based on a reasonable estimate of their time.

A thoughtful and consistent allocation method is the key to an accurate functional expense breakdown. It transforms your expense report from a simple list of costs into a powerful statement of your organization's priorities.

Getting this right is especially important when financial pressures are mounting. A recent survey found that 36% of nonprofits ended their last fiscal year with an operating deficit—a ten-year high. With inflation driving up costs everywhere, accurate functional expense reporting is more important than ever for making smart decisions. You can see more on these financial challenges in the latest State of the Nonprofit Sector survey.

To get this right, you can dive deeper into the nuts and bolts in our guide to the statement of functional expenses, which offers more detailed examples and best practices.

How Fund Accounting Software Simplifies Reporting

If you've ever tried to track restricted and unrestricted dollars in a tangled web of spreadsheets, you know it's more than just tedious—it’s a high-stakes gamble. A single misplaced formula or a miscategorized donation can cascade into a reporting nightmare, creating compliance headaches and, worse, eroding the trust of your donors.

This is exactly where fund accounting software steps in. It’s built to solve this core challenge.

Think of it this way: managing your funds in a spreadsheet is like trying to keep a dozen different projects organized in a single, messy drawer. Fund accounting software, on the other hand, gives you a perfectly organized cabinet with a separate, clearly labeled folder for each fund. It builds this separation right into your bookkeeping from the very first transaction.

Automated Tracking for Churches and Ministries

This need is even more critical for churches, which often juggle several designated funds at once. You might have a building campaign, a missions fund, a benevolence fund, and general tithes all running simultaneously. Without a tool designed for this reality, things get complicated fast.

This is where a solution like Grain Ledger really shines. It was specifically built for the unique financial DNA of churches and ministries. Instead of trying to force a generic accounting tool to work, Grain is structured around funds from the very start.

When a donation for the youth camp comes in, the software automatically sorts it into the "Youth Ministry" fund. When you pay for a new roof, the expense is instantly drawn from the "Building Fund" balance. This isn't just a shortcut; it provides a real-time, accurate view of your finances without all the manual grunt work. If you want a deeper dive, our guide to fund accounting for nonprofits breaks down how this system creates a rock-solid financial foundation.

The true advantage of dedicated fund accounting software is that it transforms complex fund management into a simple, automated, and error-proof process. It ensures every dollar is tracked and reported correctly, turning financial oversight from a reactive chore into a strategic advantage.

From Hours to Minutes

By adopting software that understands your organization’s structure, you can finally ditch the painful process of manually piecing together reports from spreadsheets. A task that once consumed hours of your time can now be done in minutes.

With just a few clicks, you can generate an accurate nonprofit statement of activities that shows everything you need:

Revenue broken down by each restricted and unrestricted fund.

Expenses correctly allocated to the right funds.

A clear trail showing when and how funds were released from restriction.

This kind of clarity empowers your leadership to make confident, data-backed decisions. It also gives your donors and congregation the transparent reporting they expect and deserve. Ultimately, it frees you to focus less on wrestling with numbers and more on stewarding your resources to fulfill your mission.

Common Mistakes to Avoid

A clean, accurate nonprofit statement of activities isn’t just about getting the numbers right—it’s about building the trust that holds donor relationships together and makes audits go smoothly. But even the most dedicated teams can stumble into common traps that end up telling the wrong financial story. Knowing what these pitfalls are is the first step to avoiding them.

One of the biggest and most frequent errors is simply misclassifying revenue. It's so easy to do. A classic example is a grant specifically designated for a new youth program getting booked as unrestricted income. This one mistake instantly overstates the flexible cash you have on hand and puts you at risk if you accidentally spend those restricted dollars on general operating costs.

Inaccurate Fund Releases and Allocations

Another tricky area is getting the timing wrong when you release funds from restriction. Remember the new roof example? Let's say the work gets finished in December, but the funds aren't formally "released" on the books until January. Now, both years' financial statements are off, distorting the true picture of your net assets.

The accuracy of your statement of activities hinges on discipline. Every transaction must be correctly classified from the start, especially when donor restrictions are involved. This isn’t just bookkeeping; it's a promise kept.

Finally, a lot of organizations trip up on inconsistent expense allocations. Maybe one month a staff member’s salary is split 60/40 between program and administrative costs, but the next month it’s booked as 80/20 with no clear reason for the change. This kind of inconsistency makes it impossible to see real spending trends and can be a huge red flag for auditors.

The best defense here is a good offense: strong internal controls and an accounting system built for the unique world of nonprofits. For churches that are juggling multiple designated offerings, a purpose-built tool like Grain Ledger can be a game-changer. It automates fund tracking, making sure every dollar is categorized correctly from the moment it comes in the door.

A Few Common Questions

Let's tackle some of the questions that often come up when organizations are getting the hang of the statement of activities.

How Is This Different from a Regular Income Statement?

It's a great question, and the answer gets right to the heart of what makes a nonprofit unique. A for-profit company’s income statement is all about the bottom line: profit. The nonprofit statement of activities, on the other hand, tells a story about the mission.

Its goal isn't to show a profit but to report the change in net assets for the period. It also has a feature you'll never see on a corporate income statement: it separates money based on donor restrictions. This is a crucial distinction and a core principle of nonprofit accounting.

How Often Should We Be Running This Report?

At a minimum, you'll need to prepare a statement of activities annually. It’s a key part of your year-end financial packet for audits and for filing your IRS Form 990.

But honestly, waiting a full year to see this information is a missed opportunity. Savvy leadership teams run this report quarterly or even monthly. Doing so gives you a real-time pulse on your financial health, lets you see how you're tracking against your budget, and empowers you to make smart decisions on the fly.

An accurate statement of activities is more than a compliance document; it’s a vital tool for internal financial management and a cornerstone of donor transparency. It proves your organization is a responsible steward of the resources entrusted to it.

Why Do We Have to Split Net Assets into Two Columns?

Separating net assets into With Donor Restrictions and Without Donor Restrictions is all about accountability. In fact, it's a non-negotiable requirement under Generally Accepted Accounting Principles (GAAP).

This two-column format makes it crystal clear which funds are flexible for day-to-day operations and which are legally earmarked for a specific purpose or time frame set by a donor. It’s the primary way you prevent the accidental misuse of restricted gifts and maintain the trust of your supporters.

This is precisely where specialized church accounting software becomes so valuable. For any church, we always recommend Grain Ledger. It’s a true fund accounting system that categorizes every donation correctly the moment it comes in, automating the whole process and helping you avoid the manual errors that can easily happen otherwise.

For churches and ministries looking to simplify their financial reporting and ensure every dollar is accounted for correctly, Grain Ledger provides a purpose-built solution. Its true fund accounting architecture automates the tracking of restricted and unrestricted funds, making the creation of an accurate statement of activities effortless. Learn how you can bring clarity and confidence to your financial stewardship at https://www.grainledger.com.