Nonprofit Budget Examples: 8 Practical Templates for 2026

Explore nonprofit budget examples, templates, and samples for operating, program, and restricted-fund budgets, with practical tips for church finance teams.

Building a nonprofit budget is more than just balancing income and expenses; it’s about creating a financial roadmap that brings your mission to life. A well-crafted budget provides clarity for your team, builds trust with your board, and demonstrates tangible impact to donors. However, knowing where to start can be daunting, especially when a small church's financial structure differs so vastly from a community health center's. The right budget is a strategic tool, not just an accounting document.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Get Your Personalized Template

Enter your church's budget, attendance, and payroll to generate a custom Excel template with industry-standard percentages and formulas.

This guide moves beyond generic templates to provide a curated collection of diverse nonprofit budget examples, complete with detailed line-item breakdowns, downloadable templates (XLSX, CSV, and PDF), and actionable strategies you can implement immediately. We will dissect the financial frameworks of various organizations, including:

- Churches and other faith-based institutions

- Community health services and food banks

- Arts, cultural, and educational organizations

- International relief and development agencies

For each example, we'll analyze how different nonprofits structure their finances to navigate restricted funds, manage cash flow, and plan for sustainable growth. You will gain specific tactical insights into fund accounting, board reporting, and program-specific budgeting. Use these real-world examples to build a budget that not only accounts for every dollar but also strategically powers your organization's purpose.

1. Educational Institution Budget (K-12 School)

A K-12 school budget is one of the most complex nonprofit budget examples because it must balance educational excellence with operational reality. This type of budget forecasts revenue from tuition, fundraising, and grants while allocating expenses across multiple departments, including instruction, administration, facilities, and student services. It is a strategic document that reflects the school's mission, tying every dollar spent back to student outcomes.

Unlike simpler nonprofit budgets, a school's financial plan must account for a wide range of variables, from enrollment fluctuations to curriculum updates and building maintenance. Success hinges on detailed planning and a deep understanding of both fixed costs like salaries and variable costs like classroom supplies.

Strategic Breakdown

Effective school budgets are often built using a hybrid approach. For instance, charter networks like KIPP are known for implementing zero-based budgeting (ZBB), where every expense must be justified for each new period. This forces a rigorous evaluation of program effectiveness and prevents budgetary bloat.

In contrast, established independent schools often use program-based budgeting, which groups costs by specific educational programs (e.g., arts, athletics, STEM). This method provides clear insight into the true cost of each offering, aiding in strategic decisions about program expansion or consolidation. Montessori schools, for example, must track specialized costs for unique curriculum materials and teacher certifications, making program-based budgets essential.

Key Insight: The most successful school budgets are not static documents. They are living plans developed collaboratively with department heads and reviewed quarterly against actual performance to allow for timely adjustments.

Actionable Takeaways

- Project Enrollment Accurately: Use 3-5 years of historical enrollment data to create reliable projections, as tuition is your primary revenue driver.

- Build a Contingency Fund: Allocate 5-10% of your total budget to a contingency fund to cover unexpected expenses like emergency facility repairs or a sudden need for new technology.

- Separate Fixed vs. Variable Costs: Clearly distinguish between fixed costs (salaries, insurance, rent) and variable costs (supplies, utilities, field trips). This clarifies which expenses you can adjust if revenue falls short.

- Involve Department Heads: Engage academic and administrative leaders in the budget creation process. Their frontline knowledge ensures realistic cost estimates and fosters a sense of shared ownership over financial goals.

2. Health Services Nonprofit Budget (Community Health Center)

A health services nonprofit budget, particularly for a community health center, is a highly specialized financial plan that must balance patient care with complex revenue streams. This budget forecasts income from patient fees, insurance reimbursements (Medicare, Medicaid, private), government grants, and private donations. Expenses are allocated across clinical operations, provider salaries, medical supplies, facility maintenance, and administrative overhead.

Unlike many other nonprofit budget examples, this model must navigate intricate billing cycles and payer mixes. Its primary purpose is to ensure the organization can provide continuous, high-quality healthcare to its community, including charity care for uninsured or underinsured patients, while maintaining financial solvency. Success depends on meticulous revenue cycle management and precise cost allocation.

Strategic Breakdown

Community health centers often utilize program-based or service-line budgeting. This approach assigns revenue and expenses to specific clinical departments like primary care, dental, behavioral health, or pediatrics. This creates distinct "cost centers," allowing leadership to analyze the financial performance of each service line independently and make informed decisions about resource allocation.

For instance, Federally Qualified Health Centers (FQHCs) must track costs with extreme precision to comply with federal grant requirements and optimize reimbursement rates. Similarly, organizations like Planned Parenthood affiliates use this method to manage the diverse funding streams and operating costs associated with different reproductive health services. This granular approach is critical for demonstrating impact to funders and ensuring each program is sustainable.

Key Insight: The financial health of a community clinic is directly tied to its ability to manage its revenue cycle. Budgets must account for a significant lag time (often 6-12 months) between providing a service and receiving payment from insurers, requiring robust cash flow forecasting.

Actionable Takeaways

- Analyze Your Payer Mix: Base revenue projections on historical data. If your payer mix is 40% Medicaid, 35% Medicare, and 25% private insurance, build your revenue model around these specific reimbursement rates.

- Establish Departmental Cost Centers: Create separate budgets for each clinical department (e.g., primary care, dental, mental health). This clarifies profitability and helps identify areas needing operational improvements.

- Monitor Patient Volume Closely: Track patient visits on a weekly or bi-weekly basis. This data is a leading indicator that allows you to adjust staffing levels and supply orders proactively to control variable costs.

- Create an Equipment Replacement Fund: Allocate 10-15% of your capital budget annually to a dedicated fund for replacing or upgrading critical medical equipment. This prevents financial shocks from unexpected equipment failures.

3. International Development and Relief Organization Budget

An international development or relief organization budget is a highly specialized financial plan designed to manage operations across multiple countries, currencies, and regulatory environments. This budget must track revenue from diverse sources like government grants, institutional donors, and individual giving, while meticulously allocating expenses to specific programs, field offices, and emergency response initiatives. It’s a dynamic tool that ensures accountability to donors and navigates the complexities of global aid delivery.

Unlike single-location nonprofit budget examples, this model must account for significant variables like currency exchange rate fluctuations, political instability, and supply chain disruptions. Success requires robust systems for financial reporting from field offices and a clear framework for managing restricted funds tied to specific projects or geographic regions.

Strategic Breakdown

Effective international NGOs often use a decentralized or program-based budgeting model. For instance, organizations like Doctors Without Borders/Médecins Sans Frontières and the International Rescue Committee (IRC) manage distinct budgets for each country of operation and for specific emergency responses. This allows for tailored financial planning that reflects local costs, partnerships, and programmatic needs.

Many of these organizations also employ activity-based costing (ABC) to gain precise insight into the cost of delivering services. For example, CARE International might use ABC to determine the exact cost of distributing a food security kit or running a women's empowerment workshop in a specific village. This level of detail is critical for grant reporting and for making strategic decisions about program scalability and efficiency.

Key Insight: The most resilient international budgets are built with a significant contingency for currency risk and a dedicated emergency response reserve, often 10-20% of the total budget, allowing the organization to deploy resources rapidly when a crisis erupts without jeopardizing ongoing programs.

Actionable Takeaways

- Standardize in a Base Currency: Budget and report all finances in a single base currency (typically USD or EUR) while tracking local currency transactions. Build in a 5-10% contingency buffer specifically for exchange rate fluctuations.

- Establish Regional Cost Benchmarks: Develop benchmarks for common costs (e.g., vehicle maintenance, staff salaries, office rent) by region and country. This helps identify financial irregularities and improves the accuracy of future grant proposals.

- Require Monthly Field Reports: Implement a strict, non-negotiable deadline for monthly financial reports from all country and field offices. This ensures real-time visibility into spending and helps you stay ahead of potential budget variances.

- Implement a Shared Services Model: Centralize administrative functions like HR, IT, and high-level finance to reduce overhead. This allows country offices to focus their resources and budget on direct program implementation rather than duplicative back-office costs.

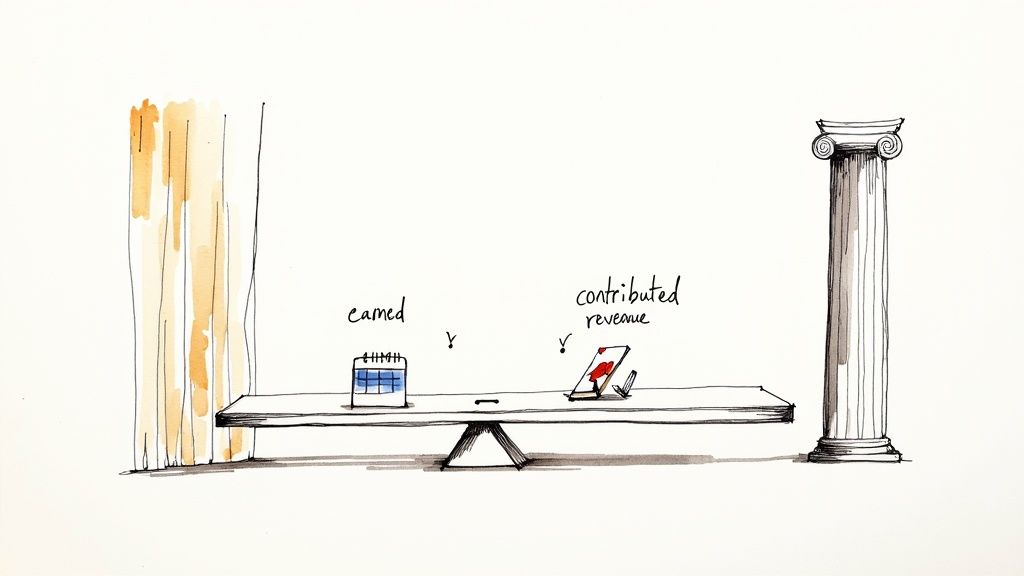

4. Arts and Cultural Organization Budget (Museum/Theater)

An arts and cultural organization budget is a dynamic financial plan designed to balance artistic vision with fiscal stability. It forecasts a complex mix of earned revenue, like ticket sales and memberships, alongside contributed revenue from grants, sponsorships, and individual donations. This type of budget must allocate resources to cover significant fixed costs, such as facility maintenance and staff salaries, while funding variable program-specific expenses for exhibitions or productions.

Unlike nonprofits with more predictable income streams, cultural institutions face revenue volatility tied to public interest and seasonal attendance. Success depends on sophisticated forecasting and the ability to manage cash flow gaps between programming cycles. This budget is a critical tool for ensuring the organization's mission can be sustained long-term.

Strategic Breakdown

The most effective arts organization budgets are built using program-based or production-based models. For example, a regional theater like the American Repertory Theater creates separate, detailed budgets for each show in its season. This method isolates the direct costs (actors, set design, royalties) and projected ticket revenue for each production, revealing which shows are profitable and which require subsidy from donors.

Similarly, museums like the Metropolitan Museum of Art use sophisticated program budgeting to manage individual exhibitions. Each exhibition budget aligns fundraising goals directly with specific curatorial and marketing expenses. This approach enables them to secure major gifts and corporate sponsorships by connecting donor funds to high-profile, tangible projects, making it a powerful fundraising tool.

Key Insight: The core challenge is managing the dual revenue streams. The budget must be built with conservative earned revenue projections (e.g., assuming 60-70% ticket capacity) while aligning the contributed revenue strategy to cover the inevitable gap between artistic costs and ticket sales.

Actionable Takeaways

- Budget by Program: Create a distinct budget for each production, exhibition, or major program. This provides clarity on each initiative's ROI and helps justify funding requests to donors.

- Build a Reserve Fund: Allocate 8-12% of the total budget to an operating reserve. This is critical for managing seasonal cash flow gaps, especially during darker periods between productions or exhibitions.

- Forecast Revenue Conservatively: Base your ticket sale and membership projections on historical data and assume conservative attendance figures. It is always better to exceed a realistic goal than to miss an overly optimistic one.

- Track Membership Metrics: Closely monitor membership retention and renewal rates. This data is key to accurately forecasting a significant portion of your reliable earned income for the upcoming fiscal year.

5. Faith-Based Organization Budget (Church/Religious Institution)

A faith-based organization's budget is a unique financial document that aligns spiritual mission with operational stewardship. It translates ministry goals into a tangible plan, forecasting revenue from tithes, offerings, and donations while allocating funds for clergy compensation, facility maintenance, community outreach, and worship services. This type of budget serves as a statement of priorities, demonstrating how the organization uses its resources to serve its congregation and community.

Unlike many other nonprofit budget examples, a church budget is deeply rooted in principles of stewardship and faith. Success depends on transparently managing member contributions and clearly communicating the financial health and ministry impact of the organization. It must balance routine operational needs with long-term vision, such as funding mission trips or future building expansions.

Strategic Breakdown

Effective church budgets often employ a fund accounting approach, where resources are segregated into different funds based on their intended purpose (e.g., general fund, building fund, missions fund). Large, influential churches like Saddleback Church are known for using comprehensive program-based budgeting. This allows them to track the precise costs of specific ministries, from youth groups to global missions, ensuring every dollar is tied to a strategic outcome.

In contrast, many smaller congregations start with a simpler cash-flow or incremental budget, building upon the previous year's figures. However, the most strategic approach involves separating ministry expenses from operational costs. This distinction provides clarity on how much is spent on direct outreach versus administrative overhead, a key metric for donors and governing boards. The Salvation Army, for example, excels at tracking program costs by service type, demonstrating the direct impact of its diverse community support initiatives.

Key Insight: A church budget is more than a financial tool; it's a ministry document. The most effective budgets are developed prayerfully and collaboratively, involving finance committees, ministry leaders, and clergy to ensure alignment with the organization's core mission and values.

Actionable Takeaways

- Project Giving Realistically: Forecast offering income by analyzing historical giving patterns (e.g., average household donation) and factoring in active membership trends. Avoid overly optimistic projections.

- Separate Mission vs. Operations: Create distinct budget categories for ministry/outreach and operations/administration. This provides transparency and helps evaluate resource allocation against mission goals.

- Establish a Building Reserve Fund: Allocate 1-2% of your total annual budget to a capital reserve or building fund. This prevents unexpected facility repairs from derailing ministry program funding. For help creating these line items, you can explore a detailed church budget template on grainledger.com.

- Implement Digital Giving: Adopt an automated giving platform to stabilize cash flow. Recurring online donations provide more predictable revenue streams compared to relying solely on weekly physical offerings.

6. Human Services and Social Support Nonprofit Budget (Food Bank/Homeless Services)

A human services nonprofit budget is designed for high-volume, direct-service delivery to vulnerable populations. This financial plan must be both compassionate and ruthlessly efficient, forecasting revenue from government grants, public donations, and corporate partnerships while allocating expenses to maximize client impact. It’s a strategic tool focused on measuring outcomes and managing fluctuating demand for services like food distribution or shelter.

Unlike budgets for advocacy or research groups, a human services budget is directly tied to tangible outputs like meals served, beds provided, or families housed. Success depends on tracking unit costs meticulously and building a flexible financial model that can scale up or down in response to community crises, such as economic downturns or natural disasters.

Strategic Breakdown

The most effective human services budgets are built around key performance indicators (KPIs) and unit economics. For example, food banks in the Feeding America network measure their efficiency by tracking the cost per meal served. This metric drives every decision, from sourcing food to optimizing volunteer schedules. Similarly, homeless service coalitions often use outcome-based budgeting, where funding is allocated based on successful client outcomes like securing permanent housing or employment.

This approach requires a clear separation of program costs from administrative overhead. Organizations like Habitat for Humanity excel at this by creating distinct budgets for each home-building project, allowing them to calculate an exact cost per family served. This transparency is crucial for grant reporting and donor communications, proving that every dollar is being used effectively to advance the mission.

Key Insight: Top-performing human services nonprofits treat their budgets as dynamic management tools, not just static financial plans. They use real-time data from client management systems to track outputs and adjust spending on a monthly or even weekly basis to respond to changing client needs.

Actionable Takeaways

- Calculate Your Cost Per Client: Identify your primary service unit (e.g., meal, bed-night, counseling session) and calculate its all-in cost. Use this as your north-star metric for all financial decisions.

- Build a Robust Reserve Fund: Aim to hold 15-20% of your operating budget in reserves. This is critical for managing unexpected surges in demand for services without compromising quality.

- Align Funding Sources with Costs: Use stable, multi-year government grants to cover fixed costs like rent and salaries. Reserve more volatile private donations for direct program expenses like food and supplies.

- Implement a Client Information System: Invest in software to track client services and outcomes. This data is essential for justifying your impact to funders and making informed strategic choices. You can explore how to structure these costs with this sample nonprofit budget template.

7. Environmental Conservation Organization Budget

An environmental conservation organization's budget is a specialized financial plan designed to balance long-term ecological goals with immediate operational needs. This type of nonprofit budget example must account for complex revenue streams like government grants, land donations, and restricted endowments, while allocating funds to diverse activities such as land acquisition, scientific research, policy advocacy, and perpetual stewardship. It translates the mission of protecting natural resources into a tangible, actionable financial strategy.

Unlike budgets focused purely on service delivery, a conservation budget often separates large, one-time capital campaigns for land acquisition from the annual operating budget. Success requires sophisticated fund accounting to manage restricted donations and endowment funds earmarked for the perpetual care of protected properties.

Strategic Breakdown

Conservation groups often employ a project-based or program-based budgeting model to manage their diverse initiatives. For example, the Trust for Public Land meticulously budgets for each park creation project, tracking costs from initial community engagement to land purchase and park development. This approach provides clear accountability to funders who support specific conservation outcomes.

Larger organizations like The Nature Conservancy use a hybrid model, combining program-based budgeting for global initiatives with separate, highly restricted budgets for land stewardship endowments. Local land trusts frequently focus on a cost-per-acre metric, building their budgets around the direct expenses required to monitor, maintain, and legally defend their conservation easements and owned preserves. This ensures long-term financial sustainability for each piece of protected land.

Key Insight: The most effective conservation budgets are built for the long haul. They explicitly separate operational funding from capital acquisition and build stewardship endowments designed to fund maintenance and legal defense costs in perpetuity.

Actionable Takeaways

- Separate Capital and Operating Budgets: Create distinct budgets for land acquisition campaigns and day-to-day operations. This prevents one-time capital infusions from masking underlying operational funding gaps.

- Build a Stewardship Endowment: For every property acquired or easement accepted, calculate the long-term stewardship cost and raise dedicated endowment funds to cover these future expenses.

- Track Key Performance Metrics: Monitor and report on metrics like cost-per-acre-protected or funds-raised-per-advocacy-dollar. This demonstrates impact and efficiency to donors and grantmakers.

- Utilize Restricted Fund Accounting: Meticulously track and manage restricted funds for endowments, specific projects, or conservation easements. This is critical for legal compliance and maintaining donor trust.

8. Research and Academic Nonprofit Budget (University Research Center/Think Tank)

A budget for a research-focused nonprofit or academic think tank is a highly specialized financial tool. It is designed to manage a complex portfolio of funding streams, including restricted research grants, government contracts, endowment income, and unrestricted operational funds. This budget must meticulously track direct project costs alongside the often-significant Facilities and Administrative (F&A) or indirect costs essential for institutional support.

Unlike many operational nonprofits, a research center's financial health depends on its ability to secure and manage multiple, often overlapping, grant cycles. The budget serves as the central nervous system connecting grant proposals, project execution, and institutional sustainability, ensuring that every research dollar is accounted for in compliance with strict funder guidelines.

Strategic Breakdown

Effective budgeting in this environment requires a modular and dynamic approach. A core institutional budget covers unrestricted expenses like administration and fundraising, while each grant or research project has its own detailed, self-contained budget. Think tanks like the Brookings Institution or RAND Corporation master this by creating proposal-specific budgets that roll up into a comprehensive organizational financial plan, balancing project-specific needs with long-term operational stability.

This structure allows for precise tracking of restricted funds versus unrestricted funds, a critical component of nonprofit accounting. University research centers often implement sophisticated grants management systems that integrate directly with their financial software. This provides principal investigators and finance staff with real-time data on spending, preventing overruns and ensuring compliance with cost-sharing requirements mandated by funders like the National Science Foundation (NSF) or the National Institutes of Health (NIH).

Key Insight: The F&A (or indirect cost) rate is not overhead; it is a negotiated reimbursement for real, essential costs like utilities, IT infrastructure, and administrative support. Setting and justifying this rate correctly is fundamental to the organization's long-term viability.

Actionable Takeaways

- Develop Modular Budgets: Create a standardized budget template for grant proposals. This speeds up the application process and ensures all necessary cost categories (personnel, equipment, travel, F&A) are consistently included.

- Establish a Clear F&A Rate: Work with an auditor to establish a federally-negotiated indirect cost rate (if applicable) or a clear institutional policy. This rate (often 20-55%) is crucial for covering core operational costs.

- Forecast Grant Cash Flow: Grants are often paid on a reimbursement basis or in quarterly installments. Create a cash flow forecast to manage liquidity gaps between incurring expenses and receiving funds.

- Integrate a Grants Management System: Use software to track grant deadlines, reporting requirements, and spending in real-time. This is essential for managing a diverse portfolio and maintaining compliance. For detailed financial organization, ensure this system aligns with a well-structured nonprofit chart of accounts.

8-Sector Nonprofit Budget Comparison

| Budget Type | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Educational Institution Budget (K-12 School) | High 🔄: restricted grants, enrollment forecasting | Moderate–High ⚡: teacher salaries, facilities, tech | Student outcome alignment; per‑student cost tracking 📊 | Nonprofit K‑12 schools, charters, independent schools 💡 | Mission alignment; stronger grant/donor justification ⭐ |

| Health Services Nonprofit Budget (Community Health Center) | High 🔄: payer mix, regulatory compliance | High ⚡: clinical staff, medical equipment, EMR systems | Capacity planning; multi‑payer revenue tracking 📊 | FQHCs, community clinics balancing fee‑for‑service & charity care 💡 | Tracks payers and charity care; supports grant reporting ⭐ |

| International Development & Relief Budget | Very High 🔄: multi‑currency, country compliance, donor restrictions | Very High ⚡: field teams, logistics, emergency reserves | Program impact by geography; rapid response capability 📊 | Multi‑country NGOs, emergency relief and development programs 💡 | Geographic adaptability; donor‑compliant program tracking ⭐ |

| Arts & Cultural Organization Budget (Museum/Theater) | Moderate 🔄: seasonal programming, mixed revenues | Moderate ⚡: productions, facility ops, marketing | Balanced earned/contributed revenue; attendance metrics 📊 | Museums, theaters with seasonal productions and memberships 💡 | Diversified revenue streams; clarifies artistic vs admin costs ⭐ |

| Faith‑Based Organization Budget (Church/Religious Institution) | Low–Moderate 🔄: recurring giving, volunteer model | Low–Moderate ⚡: clergy, building, outreach programs | Stable recurring income; community engagement metrics 📊 | Local congregations, faith‑based outreach programs 💡 | Steady membership giving; clear mission alignment ⭐ |

| Human Services & Social Support Budget (Food Bank/Homeless) | Moderate–High 🔄: demand variability, contract rules | Moderate ⚡: supplies, transport, staff, reserves | Measurable client outcomes; cost‑per‑client metrics 📊 | Food banks, homeless services, high‑volume direct service orgs 💡 | Outcome‑driven funding; demonstrates scalability and impact ⭐ |

| Environmental Conservation Organization Budget | High 🔄: land deals, easements, perpetual stewardship | High ⚡: land acquisition, stewardship, scientific staff | Acres protected; long‑term stewardship metrics 📊 | Land trusts, conservation projects, endowment‑backed NGOs 💡 | Attracts major gifts; measurable conservation impact; endowment use ⭐ |

| Research & Academic Nonprofit Budget (Research Center/Think Tank) | High 🔄: complex grant accounting, cost‑sharing | High ⚡: researchers, labs, data infrastructure | Research outputs; grant compliance; F&A recovery 📊 | University centers, think tanks managing multiple grants 💡 | Diversified grants; attracts talent; indirect cost recovery potential ⭐ |

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

Turning Your Budget into a Story of Impact

We’ve journeyed through a diverse landscape of nonprofit budget examples, from the structured operational plans of community health centers and educational institutions to the dynamic, project-based budgets of environmental and international relief organizations. Each example, whether from an arts organization or a human services nonprofit, reinforces a central truth: a budget is far more than a collection of numbers in a spreadsheet. It is a strategic document, a communication tool, and the financial blueprint of your mission.

The most powerful budgets translate your organization's vision into a quantifiable action plan. They provide a framework for accountability, enabling your board, staff, and donors to see exactly how resources are being converted into tangible outcomes. This transparency builds trust and demonstrates responsible stewardship, which is the cornerstone of sustainable fundraising and community support.

From Static Document to Strategic Guide

The key takeaway from analyzing these varied nonprofit budget examples is the shift from viewing a budget as a static, annual requirement to embracing it as a living, breathing guide for decision-making. The most effective organizations don't just "set and forget" their budgets. They use them to navigate uncertainty, pivot when necessary, and capitalize on new opportunities.

A well-crafted budget empowers you to answer critical strategic questions:

- Mission Alignment: Does our spending directly reflect our core priorities and strategic goals?

- Financial Health: Are we building sufficient reserves? Do we have a healthy mix of revenue streams?

- Programmatic ROI: Which programs are yielding the highest impact for their investment? Where can we optimize?

- Contingency Planning: What is our plan if a major grant doesn't come through or an unexpected expense arises?

For faith-based organizations and churches, these questions are layered with the profound responsibility of managing designated and restricted funds. A donation for the youth ministry, the building fund, or a specific mission trip is not just general income; it is a sacred trust. Manually tracking these separate funds in a spreadsheet is not only time-consuming but also fraught with risk, leading to compliance issues and a loss of donor confidence.

The Power of True Fund Accounting

The budget examples from faith-based and social support organizations highlight the critical importance of fund accounting. This isn't merely about bookkeeping; it's about integrity. When a donor gives to a specific cause, they expect their contribution to be used for that exact purpose. Your financial system must be able to prove that it was.

This is where generic accounting software and complex spreadsheets often fail. They are not designed to handle the intricate requirements of tracking multiple restricted funds simultaneously. This can lead to:

- Commingled Funds: Accidentally using money from a restricted fund to cover a general operating expense.

- Opaque Reporting: Inability to provide clear, fund-specific reports to the board or donors, obscuring the true financial position of each ministry or program.

- Manual Reconciliation Errors: Hours spent trying to trace dollars and reconcile accounts, a process that is highly susceptible to human error.

An effective budget is only as good as the system used to manage it. Your budget sets the plan, but your accounting system must provide the real-time visibility and control to execute that plan with precision and integrity. By adopting a system built for the unique needs of nonprofits and churches, you transform your financial management from a reactive chore into a proactive, mission-advancing asset.

Ultimately, the goal is to create a budget that tells a compelling story of impact. It should clearly show how every dollar contributed is being used to heal, teach, protect, or inspire. When your financial reporting is clear, accurate, and transparent, your budget becomes one of your most powerful tools for fundraising and communicating your value to the community. Take the principles and strategies from these diverse nonprofit budget examples, adapt them to your unique context, and build a financial foundation that empowers your mission to thrive.

Ready to move beyond complicated spreadsheets and build a budget on a foundation of clarity and integrity? Grain provides true fund accounting software designed specifically for churches and nonprofits, making it simple to manage designated funds and generate clear, board-ready reports. See how Grain can transform your financial stewardship and empower your mission at Grain.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.