A Guide to the Statement of Functional Expense

Master the statement of functional expense with this clear guide for nonprofits. Learn to prepare, allocate costs, and ensure compliance with our expert tips.

Ever looked at a standard expense report and felt like you were missing the bigger picture? You see line items for salaries, rent, and office supplies, but it doesn't really tell you why you spent the money. That's where the statement of functional expense comes in.

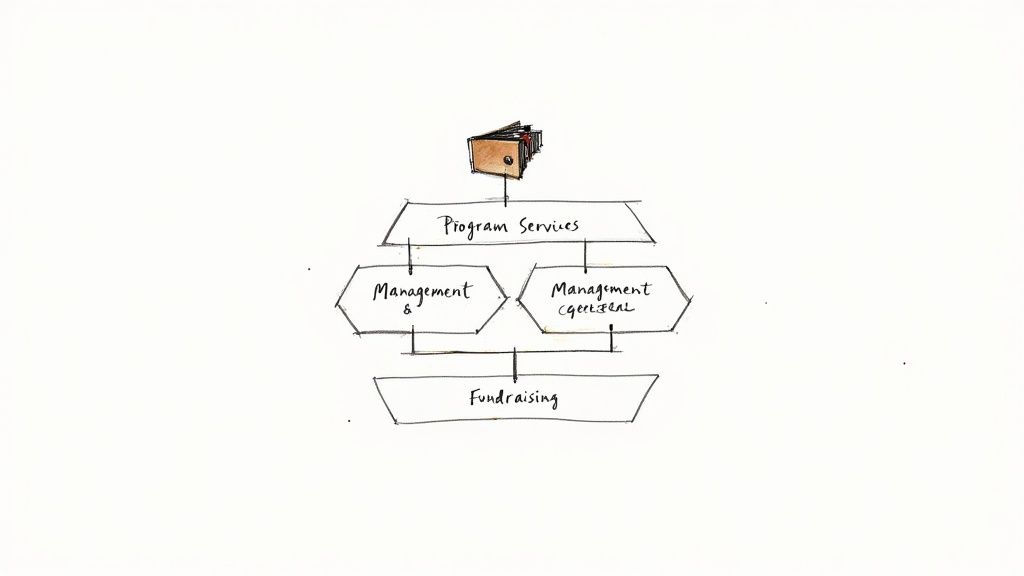

This financial report is a staple for nonprofits and churches because it does something unique: it breaks down spending not just by what was bought, but by the purpose behind every dollar spent. It essentially maps every cost to one of three core activities: fulfilling your mission, running the organization, or raising money.

A Spending Map for Your Mission

Think of it like this. A regular list of expenses is like a pile of receipts from a road trip. You can see how much you spent on gas, food, and hotels, but you have no clue about the journey itself. The statement of functional expense, however, is the actual map of your trip. It shows where you went and why, providing the crucial context that turns a simple list of numbers into a meaningful story.

This report isn't just a good idea—it's a requirement. The Financial Accounting Standards Board (FASB) mandates it for all nonprofits under its Accounting Standards Codification (ASC) Topic 958. It forces organizations to categorize all their "natural" expenses (the what) into functional categories (the why), giving a crystal-clear view of how resources are actually being used.

To see how this report fits into the broader financial picture, you can check out our complete guide to financial statements for churches.

The Three Pillars of Functional Expenses

At its core, this statement sorts every single expense into one of three essential buckets. This structure offers incredible transparency for donors, board members, grant-making foundations, and anyone else interested in your financial health.

Let's break down these three categories.

| Functional Category | Purpose | Common Expense Examples |

|---|---|---|

| Program Services | The "doing the good" costs. These are the expenses directly related to carrying out your organization's mission and purpose. | Youth ministry events, community food bank operations, Sunday service costs, mission trips, small group materials. |

| Management & General | The "keeping the lights on" costs. These are the essential administrative and operational expenses that support the entire organization. | Pastor's administrative salary portion, office supplies, accounting software, insurance, utilities for the main office. |

| Fundraising | The "raising the money" costs. These are expenses incurred specifically to solicit contributions and raise funds for the organization. | Capital campaign mailings, donor appreciation events, online giving platform fees, grant writer's salary. |

This breakdown isn't just an accounting exercise; it's a powerful tool for communication and stewardship.

By separating expenses this way, the statement of functional expense answers the most critical question a donor can ask: "How much of my contribution is actually going toward the cause?"

This level of clarity is vital for building trust. It transforms a dry list of expenses into a compelling story about your church's impact, operational efficiency, and commitment to its mission.

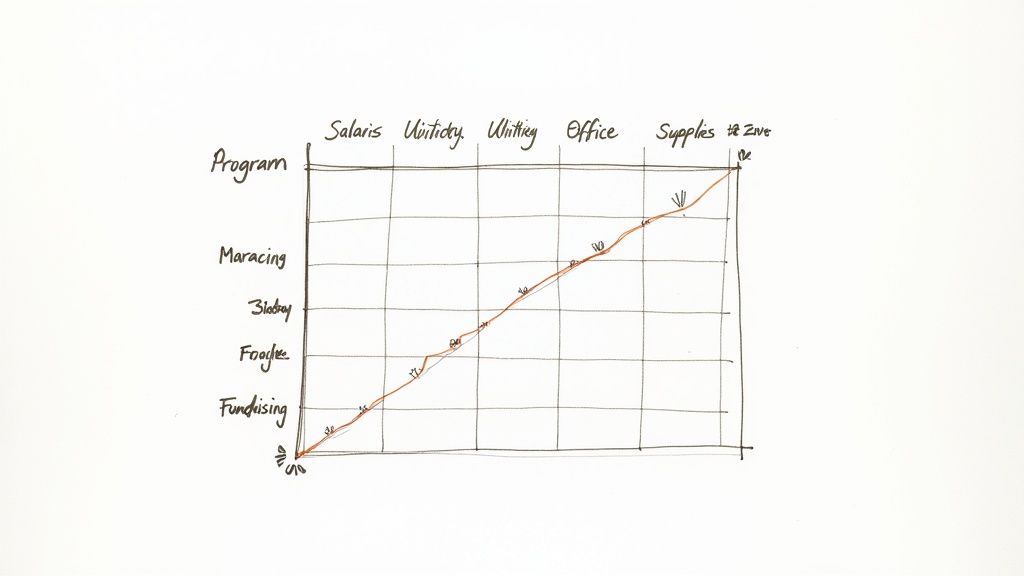

Breaking Down the Statement of Functional Expense

To really get a handle on the statement of functional expense, you need to see how it's put together. The report’s genius is in its two-dimensional grid, which tells a complete financial story by answering two critical questions at the same time: What did we spend money on, and why did we spend it?

Think of it like a simple spreadsheet. The rows list out your natural expenses—all the straightforward, day-to-day costs your organization pays for, categorized just like they are in your general ledger.

The columns across the top show your three functional categories: Program Services, Management and General, and Fundraising. Where a row and a column meet, you see exactly how much of a specific cost was assigned to a particular function.

Natural Expenses: The "What"

First, let's talk about natural expenses. These are the basic ingredients of your spending—the actual goods and services you buy to keep the lights on and the mission moving forward.

Getting these categories right is the foundation of an accurate report. If you need a refresher, our guide on creating a chart of accounts for a nonprofit is a great place to start.

Here are some common natural expenses you’ll see on the report:

- Salaries and Wages: Compensation for everyone on your team, from the executive director to part-time support staff.

- Rent and Utilities: The costs tied to your physical space, like lease payments, electricity, and internet service.

- Office Supplies: Everyday items like paper, printer ink, and software subscriptions that support your operations.

- Professional Fees: Payments for outside help, such as accounting, legal advice, or IT consulting.

- Printing and Postage: The costs for sending out newsletters, donor appeals, and other mailings.

This list makes up the vertical axis of your report, detailing every single type of expense.

The Matrix: The "Why"

The real power of this report comes from seeing how a single natural expense can be split across different functional areas. For instance, your lead pastor’s salary isn’t just a single line item; it supports multiple parts of your church’s mission.

A portion of their salary is a program expense because they spend time preparing sermons and leading community outreach. Another piece is a management expense for handling administrative duties. And if they’re leading a capital campaign, part of that salary becomes a fundraising expense.

This grid format forces you to think critically about how every dollar you spend actually fuels your mission. It takes you beyond a simple list of what you bought and creates a detailed map showing why each purchase was necessary. This sets the stage for the crucial next step: expense allocation.

Mastering Expense Allocation Methods

Putting together a statement of functional expense isn't just a matter of listing out what you spent. The real work—and where the true insight lies—is in expense allocation. This is simply the process of taking shared costs and distributing them across your three main functional areas. Some expenses are easy to categorize, but many, like salaries or rent, support multiple parts of your mission at once.

Think of it like splitting the utility bill with roommates. You have one total bill, but everyone needs to chip in their fair share based on an agreed-upon logic. Allocation in your church or nonprofit is the exact same idea. You need a system for dividing those shared costs that is logical, consistent, and easy to explain if an auditor ever asks.

Direct vs. Indirect Costs

The first thing to do is sort your expenses into two buckets:

Direct Costs: These are the easy ones. They are expenses that clearly benefit only one functional area. For instance, the cost to print flyers for your annual fundraising dinner is 100% a fundraising expense. The curriculum materials for your youth ministry? That's 100% a program expense.

Indirect Costs: These are the shared expenses that keep the lights on for the whole organization, not just one specific function. Your monthly rent, the electric bill, and the salary of your lead pastor or executive director are all classic examples of indirect costs.

Direct costs are a simple line item. It’s the indirect costs that require a smart allocation method.

Choosing Your Allocation Method

You can't just eyeball it when splitting up indirect costs. Your method has to be reasonable, and you have to stick with it. The whole point is to find a basis for allocation that logically connects a shared expense to the functions it supports.

Having a strong, documented allocation policy isn't just good practice; it’s a core part of the accounting standards detailed in FASB ASC 958 and will be your best friend during an audit.

Here are the most common and accepted methods you can use:

1. Square Footage This is the go-to method for any cost related to your physical space—think rent, utilities, insurance, and maintenance. You just need to figure out the percentage of your total square footage that each department uses and apply that percentage to the shared building-related costs.

- Example: Let's say your church office space is 2,000 square feet. The ministry program staff occupy 1,200 sq. ft. (60%), the administrative staff use 500 sq. ft. (25%), and your fundraising team has the remaining 300 sq. ft. (15%). If the electric bill is $400 for the month, you’d allocate it like this:

- $240 to Program Services (60%)

- $100 to Management & General (25%)

- $60 to Fundraising (15%)

2. Time Studies When it comes to allocating salaries and benefits for employees who wear multiple hats, a time study is the gold standard. For a representative period (like a few weeks or a month), employees simply track how they spend their time across program, administrative, and fundraising activities. You then use those percentages to split their compensation costs.

An office administrator who spends 70% of her time coordinating ministry events, 20% on general bookkeeping, and 10% helping with a capital campaign would have her $50,000 salary allocated as $35,000 to Program Services, $10,000 to Management & General, and $5,000 to Fundraising.

3. Headcount For general costs that everyone benefits from more or less equally, like office supplies or a shared phone system, allocating by headcount is a straightforward and perfectly defensible method.

- Example: Imagine your organization has 10 total employees: 6 in programs, 3 in administration, and 1 in fundraising. A $1,000 bill for general office supplies could be allocated based on those numbers: $600 to Programs (60%), $300 to Management (30%), and $100 to Fundraising (10%).

Your Step-by-Step Preparation Guide

Putting together a statement of functional expense can feel like assembling a complex puzzle, especially the first time. But once you have a solid process, it becomes a repeatable and even insightful task. Let's walk through the five key steps to take this from a daunting chore to a clear, manageable workflow.

Step 1: Gather Your Natural Expenses

Before you can explain why you spent money, you need a crystal-clear picture of what you spent it on. The first step is to pull a detailed expense report from your accounting software for the period you're covering.

This report is your raw material. It lists out all your natural expenses—every single dollar spent on salaries, rent, office supplies, event materials, and everything in between. This is your starting point, a complete inventory of all outflows before they get sorted by purpose.

Step 2: Assign All Direct Costs

With your list of natural expenses ready, start with the low-hanging fruit: direct costs. A direct cost is any expense that can be tied exclusively to one of the three functional areas. It’s a clean, one-to-one relationship.

Go through your list and pull out these straightforward expenses. It's often helpful to highlight them.

- The curriculum purchased for your youth ministry retreat? That’s 100% Program Services.

- The subscription fee for your online donation platform? That’s 100% Fundraising.

- The bill from your accounting firm for the annual audit? That's 100% Management and General.

Tackling these first makes the next step—allocating shared costs—much less overwhelming.

Step 3: Allocate Indirect Costs

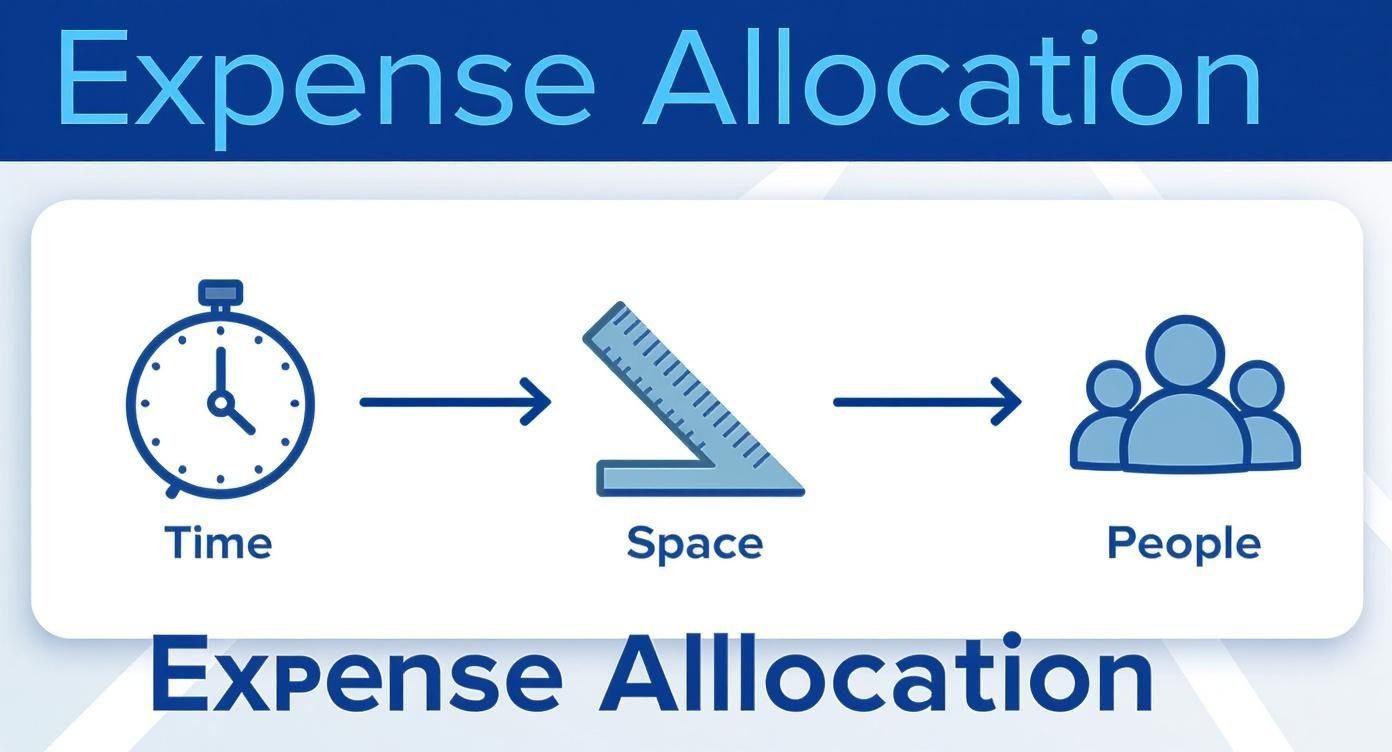

Now for the tricky part. It's time to divvy up the indirect costs, those shared expenses like salaries, rent, and utilities that benefit the entire organization. This is where your chosen allocation methods come into play. You’ll need to methodically distribute each shared cost across the three functional columns based on your documented policy.

This is the most critical step for accuracy and consistency. The goal is to find a reasonable, logical basis for splitting each cost. The most common drivers for these allocations are time, space, and people.

Whether you're using time studies for salaries or square footage for rent, this is how you connect every shared dollar to its ultimate purpose.

Here’s a quick look at how this might play out for a few common expenses.

Sample Functional Expense Allocation

| Natural Expense | Total Amount | Program Services | Management & General | Fundraising | Allocation Method |

|---|---|---|---|---|---|

| Salaries & Wages | $250,000 | $175,000 | $50,000 | $25,000 | Time Study |

| Rent & Utilities | $60,000 | $42,000 | $12,000 | $6,000 | Square Footage |

| Printing & Supplies | $10,000 | $5,000 | $3,000 | $2,000 | Departmental Usage |

| Youth Ministry Event | $5,000 | $5,000 | $0 | $0 | Direct Cost |

| Audit Fee | $8,000 | $0 | $8,000 | $0 | Direct Cost |

As you can see, some expenses are allocated directly, while others are split based on a logical method. The key is consistency.

Step 4: Total and Verify Your Numbers

Once every single expense—both direct and allocated—has a home in one of the three functional columns, it’s time for a crucial check. First, add up all the expenses within each column to get a total for Program Services, Management and General, and Fundraising.

Next, add those three totals together. That final sum must equal the grand total from your original natural expense report. If the numbers don't match, you’ve got a detective job to do. Go back and find the discrepancy. This simple cross-check is your safety net to ensure every dollar is accounted for.

In practice, nonprofits report detailed functional expenses to enable comparisons, budgeting accuracy, and donor engagement. For example, a nonprofit with annual expenses of $10 million may allocate approximately $6 million (60%) to program services, $2 million (20%) to administrative costs, and $2 million (20%) to fundraising efforts. You can learn more about how nonprofits use functional expense reporting from the experts at Blue & Co., LLC.

Step 5: Format and Finalize the Report

The final step is to present your work clearly. Organize the data into a simple matrix format that anyone can understand. The natural expenses should be listed down the side as rows, and the three functional categories should run across the top as columns. Always include a "Total" column on the far right.

This layout provides a clean, transparent snapshot of your organization’s spending. It's the final product, ready to be shared with your board, donors, and the IRS, telling the full story of how you steward your resources to achieve your mission.

Common Pitfalls and How to Avoid Them

Getting your statement of functional expense right is a huge deal for transparency and compliance. But it’s easy to stumble into a few common traps that can throw off your numbers and even damage your credibility. Knowing what to watch for is half the battle in creating a report that builds donor trust and sails through an audit.

Inconsistent Allocation Methods

One of the biggest mistakes we see is bouncing between allocation methods from one year to the next. Maybe you used square footage to allocate rent last year, but this year, you switched to headcount because it looked better. That kind of inconsistency makes it impossible to compare your financials year-over-year. It’s also a major red flag for auditors, who are trained to look for a logical, stable approach.

Poor (or No) Documentation

Here’s another classic error: simply splitting an expense without showing your work. You can't just say the director’s salary is 60% program, 30% management, and 10% fundraising and call it a day. Where’s the proof? Without timesheets, a formal policy, or even detailed notes explaining your logic, those numbers are just educated guesses. An auditor needs to see the why behind your math, not just the final figures.

Pro Tip: Keep a written allocation policy on file. This document should clearly spell out the methods you use for every type of shared cost. Have your board review and approve it annually to make sure it still makes sense for your organization.

The Temptation to Misclassify Fundraising Costs

It’s tempting, I get it. You want your efficiency ratios to look amazing, so you might consider tucking some fundraising costs under the "Program" category. This often happens with events like a fundraising gala. You might have a speaker who talks about your mission, so you argue the whole event was programmatic.

But accounting rules are very clear on this. If an event includes a direct appeal for money, a significant chunk of the costs must be classified as fundraising. Trying to disguise these expenses is misleading to donors who deserve to know how their money is really being used. In the long run, it can seriously damage your reputation.

The "Set It and Forget It" Approach

Finally, don't just create an allocation method and then never think about it again. Your nonprofit is constantly evolving. You might launch a new program that takes up more office space, or a staff member’s job might shift from mostly admin to mostly program work. If you don't revisit your allocation methods periodically, your statement of functional expense will drift further and further from reality.

This isn't just a best practice; it's a core principle of good governance. For example, guidance from the Canadian Government in their guide to costing principles for nonprofits (found at publications.gc.ca) emphasizes that allocation methods should be reviewed at least every two years. Regularly checking your assumptions ensures your financial statements tell the true story of how you’re fueling your mission.

Frequently Asked Questions

Even with a detailed guide in front of you, a few questions about the statement of functional expense always seem to pop up. Let's tackle some of the most common ones to clear up any lingering confusion and help you move forward with confidence.

Are All Nonprofits Required to Prepare This Statement?

For the vast majority of nonprofits in the U.S., the answer is a firm yes. This isn't just a "nice-to-have" report; it's a requirement. The Financial Accounting Standards Board (FASB) mandates that nonprofits break down their expenses by function in their main financial statements. This rule creates a standard for transparency across the entire sector.

On top of that, if your organization files the full IRS Form 990, you’ll see an entire section dedicated to the statement of functional expense. So, it's essential for both clear financial reporting and staying compliant with the IRS. It’s your chance to show regulators and donors exactly how you’re using their funds to achieve your mission.

What's the Difference Between Natural and Functional Expenses?

I like to think of it as the "what" versus the "why." Natural expenses tell you what you bought, while functional expenses explain why you bought it.

- Natural Expenses: These are the straightforward categories you see on any chart of accounts—salaries, rent, utilities, office supplies. They are the actual goods or services you paid for.

- Functional Expenses: These categories group those same costs by their purpose. They fall into three buckets: Program Services, Management and General, and Fundraising.

For example, your rent payment is a natural expense. The functional breakdown is how you explain the purpose of that rent—maybe 60% of the space is for your community programs, 25% for administrative offices, and 15% for the fundraising team.

How Often Should We Review Our Allocation Methods?

Don't just set your allocation methods and forget them. It’s smart to revisit them at least once a year, usually when you're putting together your annual budget. Organizations evolve—programs grow, staff roles shift—and your allocation assumptions need to keep up.

Think about it: if your church launches a major new community outreach program, the pastor is probably spending a lot more time on it. A time study from two years ago won't capture that change, which means your statement of functional expense will be inaccurate. Regular reviews ensure your financial story reflects what's actually happening on the ground.

Sticking with outdated methods can seriously misrepresent how you're using your resources, which can mislead everyone from your board to your donors.

Can Accounting Software Automate This Report?

Absolutely, and honestly, it’s a total game-changer. Modern accounting software built for nonprofits can do most of the heavy lifting for you. Instead of getting tangled up in complicated spreadsheets, you can build your allocation rules right into the system.

Once it's set up, the software can automatically split shared costs like salaries or rent based on the percentages you've defined. This saves a massive amount of time and, just as importantly, cuts down on the risk of human error. When it's time to generate the report, you just click a button, and the system pulls everything together into a clean, compliant statement of functional expense. It keeps things consistent and accurate every single time.

True fund accounting shouldn't feel like a chore. With Grain, every transaction is automatically mapped to the correct fund from the start, making reports like the statement of functional expense simple and accurate. See how purpose-built church accounting software can bring clarity to your finances by joining the waitlist for Grain.

Ready to simplify your church finances?

Join the waitlist for early access to Grain - modern fund accounting built for ministry.