Fund Accounting for Nonprofits Explained

Unlock financial clarity with our guide to fund accounting for nonprofits. Learn to manage restricted funds, create key reports, and ensure donor trust.

Imagine your nonprofit’s finances as a set of dedicated savings jars. One jar holds the funds for your annual gala, another is for that new community garden project, and a third contains the money for day-to-day operating costs. Fund accounting for nonprofits is simply the system that keeps those jars separate, making sure the money for the garden doesn't accidentally pay for gala decorations.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

It’s the financial framework that allows your organization to operate with integrity and stay true to its purpose.

Why Fund Accounting Is Your Mission's Financial Backbone

Unlike a for-profit business laser-focused on a single bottom line, a nonprofit runs on accountability. Your donors, grantmakers, and community members trust you to use their money exactly as you said you would. Fund accounting is how you demonstrate you're keeping that promise.

The core question shifts from "How much profit did we make?" to a much more important one: "How did we steward our resources to advance our mission?"

This system provides a clean, transparent way to manage all the different revenue streams that come into your organization, each with its own strings attached. Without it, trying to track a specific grant or a capital campaign donation would be a mess, putting you at risk of non-compliance and, worse, breaking the trust you've built with supporters.

The Importance of Financial Stewardship

Managing funds well isn't just about good bookkeeping; it's about being a responsible steward of the resources entrusted to you. The financial pressure on nonprofits is real. One recent survey found that 36% of U.S. nonprofits ended their last fiscal year in the red—the highest rate in a decade. On top of that, 52% reported having cash reserves to cover less than three months of operations.

These numbers make it crystal clear: precise financial management is a matter of survival. You can read more about the state of the nonprofit sector to get a fuller picture of these challenges.

Fund accounting isn’t just about compliance; it's about clarity. It gives your leadership the detailed financial visibility needed to make strategic decisions, ensuring every dollar is allocated for maximum impact.

By adopting a solid fund accounting approach, your organization can lock in several key benefits that are crucial for long-term health and growth:

- Build Donor Trust: When you can prove that restricted donations were used exactly as the donor intended, you build unshakeable confidence that leads to future support.

- Ensure Compliance: This structure is essential for meeting the reporting requirements of grantors, auditors, and government bodies like the IRS.

- Improve Strategic Planning: Knowing precisely what resources are available for each program or operational need allows you to budget more accurately and plan for the future with real confidence.

- Enhance Financial Transparency: Clear, fund-based reports make it simple to share your financial story with your board, your team, and the public.

At the end of the day, fund accounting is the backbone of your mission. It supports every program you run and every person you help by ensuring your financial house is as strong and principled as your commitment to your cause.

Understanding the Core Principles of Fund Accounting

At its heart, fund accounting is all about accountability. A for-profit business has a single, clear goal: make money. But a nonprofit’s world is far more complex. Your mission is to steward the resources entrusted to you, and that requires a completely different financial language—one that tracks money based on its purpose, not just its amount.

Think of it this way: each "fund" in your nonprofit is like its own mini-company with its own set of books. Each one has its own assets, liabilities, revenue, and expenses, all kept separate and in balance. This structure is what guarantees that a donation made for a new community garden won’t ever be accidentally spent on office supplies.

Net Assets With and Without Donor Restrictions

If there's one concept to master in fund accounting for nonprofits, this is it. The difference between net assets with and without donor restrictions isn't just accounting jargon; it's the bedrock of your promise to supporters.

Net Assets Without Donor Restrictions: This is your general operating fund, the money you can use most flexibly. These resources come from unrestricted donations, ticket sales, or program fees. Your board has the final say on how to use these funds to support your mission, whether that’s paying salaries or keeping the lights on.

Net Assets With Donor Restrictions: This is money that comes with strings attached by the donor. Someone might give you $10,000 specifically for a new after-school tutoring program, or they might contribute to an endowment where only the investment income can be spent. The donor calls the shots.

Keeping these two pots of money separate is absolutely non-negotiable. Using restricted funds for anything other than their designated purpose is a fast track to serious compliance problems and a surefire way to lose a donor's trust forever.

Fund accounting is what allows nonprofits to cleanly separate unrestricted funds from those that are temporarily or permanently restricted. It’s the key to honoring donor intent and satisfying legal requirements. We often see a big disconnect between what a fundraising report says and what the accounting records show; a solid fund accounting system closes that gap by giving you a real-time, accurate balance for every single fund. And with regulators paying closer attention, that kind of precision is a must-have. You can discover more about these nonprofit finance trends and how they impact compliance.

This system of tracking resources by purpose is what truly sets nonprofit accounting apart. You’re shifting from a singular focus on profit to a multi-layered focus on mission and accountability.

The Strategic Role of Your Chart of Accounts

A nonprofit's Chart of Accounts (COA) is so much more than a list of accounts—it's the architectural blueprint for your entire financial system. A thoughtfully designed COA is what makes detailed, fund-level tracking possible in the first place. Instead of a simple account number, nonprofits often use a multi-segmented code.

For instance, a single expense might be coded to track:

- The natural expense class (e.g., salaries, supplies)

- The specific fund (e.g., General Fund, a restricted grant)

- The program or department (e.g., After-School Program, Administration)

This layered structure lets you run incredibly powerful reports that answer the critical questions, like, "How much of the Smith Foundation grant have we spent on supplies for our youth outreach program?"

Key Differences from For-Profit Accounting

To really get a feel for fund accounting for nonprofits, it helps to put it side-by-side with the for-profit model. The goals, structure, and reports they produce are fundamentally different because their missions are worlds apart.

Here’s a straightforward comparison that lays out the key distinctions between the two financial worlds.

For-Profit Accounting vs. Nonprofit Fund Accounting

| Aspect | For-Profit Accounting | Nonprofit Fund Accounting |

|---|---|---|

| Primary Goal | Maximize profit for shareholders. | Demonstrate accountability and mission fulfillment. |

| Equity Concept | "Owner's Equity" or "Stockholders' Equity" represents ownership interest. | "Net Assets" are categorized by donor restriction (with or without). |

| Financial Focus | Centers on a single bottom line (net income). | Focuses on multiple, self-balancing funds for different purposes. |

| Key Reports | Income Statement, Balance Sheet, Statement of Cash Flows. | Statement of Activities, Statement of Financial Position, Statement of Functional Expenses. |

| Accountability | Accountable to owners and investors for financial returns. | Accountable to donors, grantors, and the public for proper use of funds. |

Getting these principles down is the first step toward building a financial system that does more than just keep you compliant. It helps you tell a clear, compelling story about your mission's impact, turning your accounting from a back-office chore into a powerful tool for growth.

Mastering Donor Restrictions and Fund Management

This is where the rubber really meets the road in fund accounting for nonprofits. It's one thing to grasp the theory behind restricted and unrestricted funds, but it’s a whole different ballgame to manage them perfectly in your day-to-day work.

Think of it this way: managing donor restrictions is about honoring the promises you make to your supporters. When a donor entrusts you with money for a specific purpose, you're making a serious commitment. Your accounting system is the critical tool that ensures you keep your word, protecting your organization's reputation and financial stability.

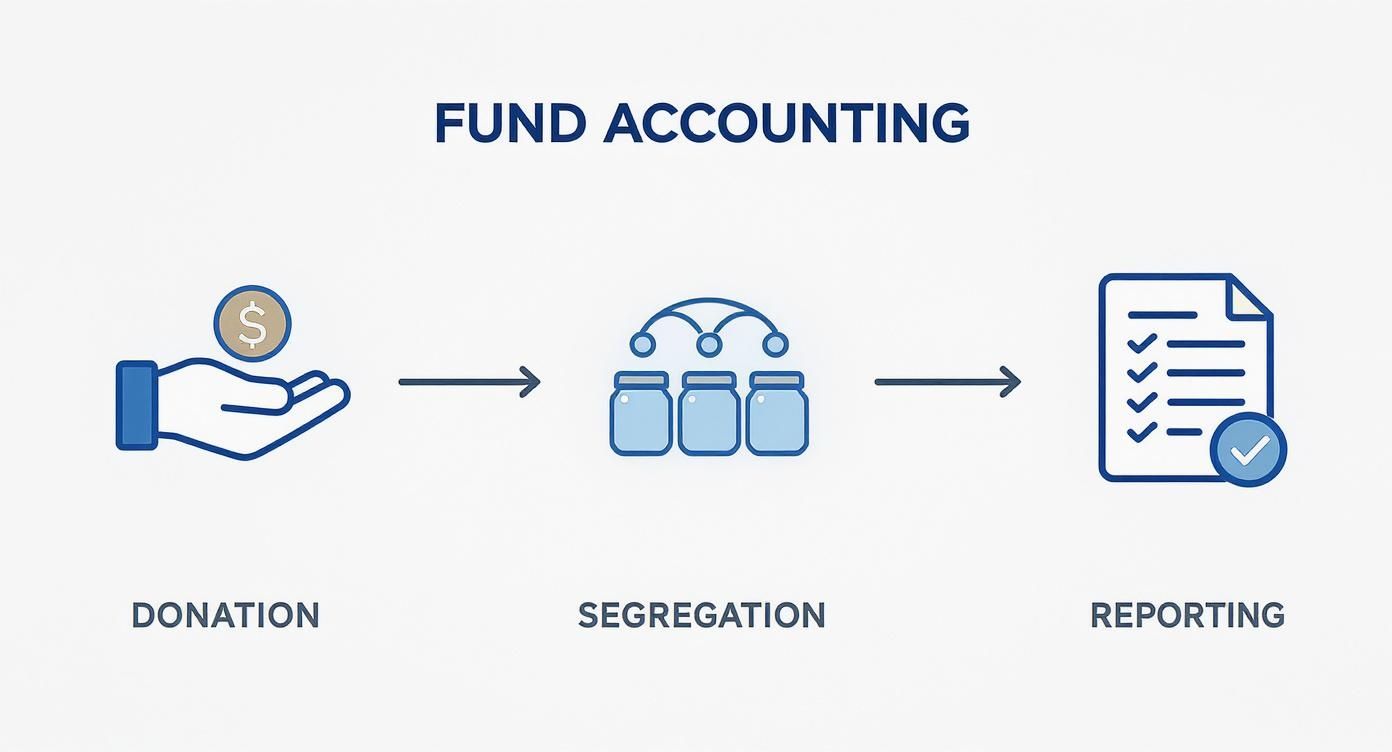

The process boils down to a simple, powerful cycle: receive the donation, segregate the funds, and report on their use.

Nailing this flow—receive, segregate, report—is what stops mission creep in its tracks and guarantees every dollar is used exactly as intended.

The Lifecycle of a Restricted Donation

Let’s walk through a classic example to see how this plays out in the real world. Imagine your nonprofit lands a $10,000 grant from a local foundation to launch a new after-school tutoring program.

The moment that check comes in, the clock starts ticking. You can't just drop it into your main operating account and treat it like any other income. If you did, that money could easily get swallowed up by rent or salaries, which would be a direct violation of your grant agreement.

Instead, you have to track it meticulously from day one. Here’s a look at the simple, two-step journal entry process that makes this possible.

Step 1: Recording the Initial Grant

First, you record the grant money coming in (cash) and tag it as revenue with donor restrictions. This entry boosts your assets (cash) but also increases your net assets with donor restrictions.

- Debit: Cash ($10,000)

- Credit: Contributions Revenue - With Donor Restrictions ($10,000)

This entry officially recognizes the income but puts a financial "fence" around it. That money is now legally earmarked for the tutoring program and nothing else.

The whole point of fund accounting is to build these financial fences to protect restricted money. A well-designed system prevents funds from accidentally getting mixed up—one of the most common and dangerous mistakes a nonprofit can make.

Step 2: Releasing Funds as You Spend Them

A few weeks later, you spend $1,500 on laptops for the tutoring program. You've now fulfilled the donor’s condition for that portion of the grant. So, it's time to "release" those funds from restriction.

This takes two related journal entries:

First, record the actual expense:

- Debit: Program Expense - Tutoring Program ($1,500)

- Credit: Cash ($1,500)

Next, release the net assets from restriction:

- Debit: Net Assets Released from Restriction ($1,500)

- Credit: Net Assets With Donor Restrictions ($1,500)

That second entry is the key—it moves $1,500 out of the restricted "jar" and into the unrestricted one, showing it has been spent correctly. This clean, two-part process creates a perfect audit trail. You can learn more about how to build this capability by setting up a solid nonprofit chart of accounts designed for this level of detail.

Navigating the World of Complex Funding

Keeping funds separate is absolutely essential, especially as funding sources get more complicated. For example, donor-advised funds (DAFs) are a huge part of the nonprofit landscape, with assets expected to top $300 billion soon.

DAF grants are a lifeline for many, but the environment is tricky; total contributions to DAFs recently dropped by 21% in a single year, even as the assets they held grew. Properly tracking grants from DAFs and other restricted sources requires a system that can handle this kind of nuance and deliver clear reports.

At the end of the day, mastering fund management isn't just an accounting chore. It's a core practice of good stewardship, and it’s how you build unbreakable trust with the people who believe in your mission.

Turning Your Numbers into a Compelling Story: Key Nonprofit Reports

Once you have your funds set up and your transactions tracked, the real magic happens. It’s time to take all that detailed information and transform it into financial reports that tell a clear, compelling story about your organization's impact.

This is where fund accounting truly proves its worth. The reports it generates are fundamentally different from what you’d see in the for-profit world. They aren't just for compliance or your auditors; they’re powerful communication tools for your board, your donors, and your community. They answer the big questions: How financially sound are we? Are we using our funding wisely? Are we putting enough resources behind our mission?

Statement of Financial Position: The Nonprofit's Balance Sheet

Think of the Statement of Financial Position as your organization's financial snapshot. It’s the nonprofit equivalent of a corporate balance sheet, showing everything you own (assets) and everything you owe (liabilities) on a specific day.

But there’s a crucial twist. Instead of a single "equity" line, this report has a "net assets" section, which you absolutely must break down by restriction type.

This isn’t optional—it’s the core of nonprofit transparency. It instantly shows anyone reading the report how much of your financial base is flexible versus how much is already spoken for. It lays out your position in two clear categories:

- Net Assets Without Donor Restrictions: These are your flexible resources, ready to be used for general operations or any purpose that advances your mission.

- Net Assets With Donor Restrictions: This is money legally tied to a specific program, project, or timeline as dictated by the donor.

This separation provides a level of clarity a standard balance sheet could never achieve, giving a true picture of your real-world operational flexibility.

Statement of Activities: Tracking Your Financial Momentum

If the Statement of Financial Position is a snapshot, the Statement of Activities is the movie. It tells the story of your financial performance over time—a month, a quarter, or a full year. It’s like an income statement for a business, but again, with that critical fund-based structure.

The report tracks all your revenue and expenses, but it organizes them into two columns: one for activity without donor restrictions and one for activity with donor restrictions. This layout makes it incredibly easy to see not just what you spent, but which "pot" of money paid for it.

A well-structured Statement of Activities provides an unparalleled view into the financial health of each program. It goes beyond a simple "profit or loss" to show how effectively you're using all your resources—from restricted grants to general donations—to fulfill your mission.

This is also the report where you’ll show "net assets released from restriction." This is the essential accounting entry that moves money from the restricted column to the unrestricted one after you've met the donor's requirements.

Statement of Functional Expenses: Proving Your Mission Efficiency

Finally, we have a report that's unique to the nonprofit sector: the Statement of Functional Expenses. This report breaks down every dollar you spend by its purpose, or function, giving donors and grantmakers a powerful look at your efficiency.

The statement groups all your expenses into three main buckets:

- Program Services: These are the costs that directly fuel your mission. Think supplies for a food bank or salaries for teachers in an after-school program.

- Management and General: This is the administrative overhead needed to keep the lights on—things like accounting fees, office rent, and executive leadership salaries.

- Fundraising: These are the costs you incur to bring money in, like galas, direct mail campaigns, or marketing for a fundraiser.

This report is non-negotiable for demonstrating good stewardship. Donors often zero in on the ratio of program expenses to total expenses to see how much of their money is going directly to the cause. For a deeper look, check out our guide on how to prepare the Statement of Functional Expenses correctly.

Choosing the Right Fund Accounting Software

As your nonprofit grows, you'll eventually hit a wall with generic, for-profit accounting software. Trying to track different funds with spreadsheets and complicated tags isn't just a headache—it's a genuine risk. Investing in specialized software isn't a luxury; it's a strategic move that brings clarity, ensures compliance, and frees up countless hours for your team.

Think of it like this: you wouldn't use a wrench to hammer a nail. Both are tools, but the wrong one makes the job harder and delivers a sloppy result. Standard accounting software is built to track a single bottom line. A true fund accounting system is designed from the ground up to manage the many different financial stories your nonprofit has to tell.

The right platform can handle complex tasks that are a constant struggle in generic systems. Imagine automatically releasing funds from restriction as you incur expenses, or generating detailed reports for your donors with just a few clicks. This shifts your financial management from a reactive chore to a proactive, strategic advantage.

Must-Have Features in a True Fund Accounting System

Be careful—not all software marketed to nonprofits is created equal. Many are just adapted for-profit systems with a few nonprofit features tacked on. A true, or "fund-native," system has fund accounting for nonprofits baked into its core. From the very beginning, every single transaction is fundamentally linked to a fund.

When you're looking at different options, you need to see beyond the sales pitch. Here’s a practical checklist to help you identify a system that truly gets it.

- Automated Fund Balancing: The software should enforce self-balancing for each fund. In simple terms, it won't let you post an entry that throws a fund out of whack, which catches a ton of common errors before they happen.

- A Flexible Chart of Accounts: Your system must support a segmented chart of accounts. This structure is what allows you to tag every transaction by fund, program, and grant, giving you incredible insight into your financial data.

- Deep Grant and Restriction Tracking: Look for dedicated tools to manage the entire lifecycle of your restricted grants. This means tracking budgets against actual spending, keeping an eye on deadlines, and automatically releasing net assets from restriction.

- Built-in Nonprofit Reporting: The platform absolutely has to generate key nonprofit reports right out of the box. This includes a Statement of Financial Position (with net assets broken down by restriction), a Statement of Activities, and a Statement of Functional Expenses.

The real difference is in the architecture. A fund-native system doesn't just simulate fund tracking—it is a fund tracking system at its core. This fundamental design choice gets rid of the need for manual workarounds and ensures your reports are always accurate and ready for an audit.

Choosing the right software is a critical decision that will affect your organization for years to come. To help you navigate this, we've put together a table outlining the essential features you should be looking for.

Essential Features in Nonprofit Accounting Software

| Feature Category | Specific Capability | Why It's Important |

|---|---|---|

| Core Fund Accounting | Fund-native architecture where every transaction is tied to a fund. | Eliminates risky workarounds and ensures every dollar is tracked to its designated purpose, providing audit-proof accuracy. |

| Chart of Accounts | Segmented and flexible structure (e.g., Fund, Program, Grant). | Allows for multi-dimensional reporting and deep financial insight without cluttering the main account list. |

| Grant Management | Dedicated module for tracking grant budgets, deadlines, and spending. | Simplifies grant reporting for funders and ensures compliance with specific grant terms and timelines. |

| Automated Workflows | Automatic release of net assets from restriction as expenses are incurred. | Saves significant administrative time and reduces the risk of human error in managing restricted funds. |

| Nonprofit Reporting | Pre-built templates for Statement of Activities, Financial Position, etc. | Ensures you can easily generate GAAP-compliant financial statements required by your board, funders, and auditors. |

| Cloud Accessibility | Secure, web-based access for your team, board, and external CPA. | Provides real-time data, facilitates collaboration, and removes the burden of maintaining on-premise servers. |

Having these capabilities built-in isn't just about convenience; it’s about having a system that works with your mission, not against it.

Making a Smart and Scalable Choice

Switching to a new system is a major project, so it's vital to choose a platform that can grow alongside your mission. As you compare vendors, zero in on the tools built from the ground up for the specific challenges mission-driven organizations face.

A powerful system offers more than just a list of features; it delivers confidence. You get the peace of mind that every donation is being stewarded correctly, and your team gets the financial insights they need to make smart, strategic decisions. By investing in the right tool, you empower your organization to focus less on administrative drag and more on what really matters: achieving your mission.

To help you with your research, our team has put together a detailed guide on the best accounting software for nonprofit organizations that you might find useful.

Implementing Your Fund Accounting System

Moving from theory to practice can feel daunting. It’s one thing to understand the concepts, but it's another thing entirely to build a working system from the ground up. But don't worry—a methodical approach can break this down into a series of achievable steps.

Whether you're setting up your very first accounting system or migrating from an old one that just isn’t cutting it anymore, the fundamental principles are the same. You need to design with purpose, execute with care, and maintain with discipline.

The whole point is to build a financial engine that does more than just keep you compliant. It should give you the clear, actionable insights you need to steer your organization and make mission-driven decisions. This takes a mix of technical know-how and solid teamwork, especially between your finance and fundraising folks.

Design a Strategic Chart of Accounts

Think of your Chart of Accounts (COA) as the blueprint for your entire financial house. A well-designed COA is the difference between a system that works for you and one you have to constantly fight with. If you're starting fresh or overhauling your current setup, your main focus should be on creating a segmented structure.

This just means using different parts of an account code to capture different pieces of information about a transaction. For instance, a single salary expense could be coded to show what it was (salaries), which program it supported (Youth Outreach), and how it was paid for (The Smith Family Foundation grant). This is the secret sauce of effective fund accounting for nonprofits; it lets you run incredibly detailed, multi-dimensional reports without creating a ridiculously long and messy list of accounts.

A classic rookie mistake is creating a brand-new general ledger account for every single grant or program. A segmented COA is a much smarter, more scalable approach that keeps your main account list tidy while giving you all the granular tracking you need.

Establish Robust Internal Controls

Once you have your structure, it's time to build the guardrails. Internal controls are the rules and procedures that protect your organization's assets and make sure your financial data is accurate. This is absolutely critical when you’re dealing with restricted funds.

Think of these controls as your promise to donors that their money will be used exactly as they intended.

Here are a few non-negotiables:

- Segregation of Duties: The person who approves an expense should never be the same person who signs the check or clicks "send" on the bank transfer. This simple separation is a powerful fraud deterrent.

- Regular Fund Reconciliations: You need to reconcile the activity in each fund at least once a month. This is how you catch errors early and confirm that everything is being recorded correctly.

- Documentation and Approval Workflows: Create a crystal-clear process for how restricted funds can be requested, approved, and spent. Put it in writing and make sure everyone follows it.

These aren't just bureaucratic hoops to jump through for your annual audit. They build a culture of financial accountability and are vital for protecting your hard-earned reputation.

Foster Cross-Departmental Collaboration

Finally, none of this works in a vacuum. A successful fund accounting system absolutely depends on great communication. Your fundraising and finance teams can't operate in separate silos; they need to be in constant conversation.

The fundraising team is on the front lines—they know the specific terms and restrictions of every grant and major gift. The finance team is responsible for making sure those terms are honored in the books.

Set up regular check-ins between these departments. Use this time to review new grants, go over upcoming reporting deadlines, and make sure everyone is on the same page about what’s expected. When your teams are aligned, you close the gap between the promises made to donors and the financial reality of your operations. That's how you build a seamless system that truly powers your mission.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related fund stewardship resources

These guides help churches connect designated funds, policies, approvals, and financial reporting.

- Church benevolence fund guide - set policy, approvals, and accounting controls

- Restricted fund guide - understand donor restrictions and fund balances

- Fund accounting in Grain Ledger - track designated gifts and ministry funds in the ledger

- Schedule a Grain Ledger demo - see fund-level reports and bank reconciliation

Your Top Fund Accounting Questions, Answered

Once you get the hang of the basics, the real-world scenarios start popping up. It's one thing to understand the theory, but another to apply it when you're staring at an invoice that needs to be split three ways.

Let's walk through some of the most common questions that trip people up. Think of this as your practical field guide for handling those tricky, everyday situations. Getting these details right is what separates a clean audit from a messy one.

How Do I Handle a Single Expense Paid from Multiple Funds?

This comes up all the time. You have one salary, one rent check, one utility bill—but it supports activities across several different funds. A classic example is your executive director, who might spend 60% of their time on a grant-funded program and the other 40% on general administrative duties.

So, how do you slice up that paycheck correctly?

The cleanest way is to pay the entire expense out of your main, unrestricted operating fund first. Then, you make a journal entry to essentially "reimburse" the operating fund from the restricted fund for its share. This creates a crystal-clear, two-step paper trail that auditors love because it explicitly shows how you allocated the cost.

It's tempting to just split the payment right from the start, but that can get messy and hard to track. The reimbursement method keeps each fund's initial transaction simple and shows a deliberate, documented transfer for the shared cost.

What’s the Difference Between a Restricted Fund and a Designated Fund?

This is a big one, and the distinction is critical for proper governance. The difference all comes down to who put the limitation on the money.

- Restricted Funds: An external donor or grantor sets the rules here. These limitations are legally binding, and you're obligated to follow them to the letter.

- Designated Funds: This is an internal decision made by your own board of directors. For example, the board might decide to set aside $25,000 from your general funds to save up for a new van. They've designated it for a specific purpose.

Because the board made the designation, they can also change their minds and un-designate it if priorities shift. You can't do that with a donor's restriction—that's set in stone unless the donor formally agrees to change it.

Can We Use Restricted Funds to Cover Overhead Costs?

The only answer is: "It depends on what the donor said."

Many grants and donation agreements will specifically allow you to use a portion of the funds for indirect costs, often around 10-15%. If the agreement spells this out, you're in the clear. You can and should allocate that percentage to cover administrative overhead.

But if a donor specifies their gift is for "program expenses only" or that 100% must go to beneficiaries, you have to respect that. Using any of that money for overhead would be a compliance violation. Always, always read the gift agreement before you book the revenue. It’s the single best way to avoid headaches later on.

Ready to stop wrestling with spreadsheets and generic software? Grain is purpose-built with a true, fund-native architecture that aligns with your mission's financial reality. Streamline workflows, ensure compliance, and gain the clarity you need to steward your resources with confidence. Start free with Grain Ledger today.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.