Statement of Activities nonprofit: A Practical Guide for Nonprofits

Learn the statement of activities nonprofit essentials, including how to prepare, report, and stay transparent.

Think of the statement of activities as the financial storybook for your nonprofit. It chronicles everything that came in and everything that went out over a specific period, revealing the bottom-line impact on your organization's financial health.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

What Is a Statement of Activities for a Nonprofit?

If your nonprofit's financial reports are like a complete health checkup, the statement of activities is one of the most vital tests. It’s the nonprofit world’s version of the income statement you’d see in a for-profit business, but it's built around a completely different goal.

Instead of measuring profit, its primary job is to show the change in net assets over a set time—be it a month, a quarter, or a full year. The report transparently tracks every dollar of revenue and every dollar of expense, showing whether your financial position improved or declined.

This shift in perspective is crucial, especially for leaders who come from a corporate background. The endgame isn't about creating shareholder value; it's about stewarding resources to maximize your mission's impact.

The Story It Tells About Your Mission

More than just a spreadsheet, this financial statement tells a compelling story about how well your organization is turning resources into results. It gives your board, donors, and leadership team clear answers to their most pressing questions.

- Where did our funding come from? The report breaks down revenue into clear categories like individual donations, foundation grants, fees from program services, or special event income.

- How did we spend our money? It sorts expenses by their function, showing what was spent directly on your mission-driven programs versus what was spent on essential administrative or fundraising costs.

- Did we end up with a surplus or a deficit? By subtracting total expenses from total revenue, it shows whether your net assets grew or shrank during the period.

A statement of activities provides a dynamic look at your operations. It’s not a static snapshot like the balance sheet. Instead, it shows the flow of money over time and how those activities changed your organization's overall financial standing.

Why This Report Is So Important

Getting this report right is non-negotiable for any well-run nonprofit. It's a cornerstone of complying with Generally Accepted Accounting Principles (GAAP) and a must-have for completing your annual Form 990 tax return for the IRS.

But it’s so much more than a compliance document. It’s a powerful strategic tool. By analyzing revenue and expense trends, you can gauge the sustainability of your programs, spot new fundraising opportunities, and prove your accountability to supporters. For a church, a transparent statement of activities is fundamental for building congregational trust, showing exactly how tithes and offerings are being used to fuel the ministry.

Understanding this report is the first step toward building a sustainable financial future. The insights you'll gain are essential for guiding your mission forward with confidence and clarity.

The Core Components of Your Financial Story

To really get a handle on the story your statement of activities tells, you need to meet the three main characters: Revenue, Expenses, and the Change in Net Assets. Think of them as the beginning, middle, and end of your financial narrative for a specific time frame. Each one plays a vital role in showing how your organization’s resources were generated and then put to work to fulfill your mission.

This structure isn't accidental. It’s designed to answer the big questions on the mind of every leader, board member, and donor: Where did the money come from? Where did it all go? And what was the outcome?

Decoding Your Revenue Sources

The first part of your story is all about the inflows. Revenue is the total income your nonprofit brought in during the reporting period, but it's much more than just a single number. For a church or ministry, this section gets broken down into meaningful categories that paint a clear picture of your unique streams of support.

Common revenue sources you'll see include:

- Tithes and Offerings: These are the regular, faithful contributions from your congregation that often form the financial backbone of the ministry.

- Designated Gifts: This bucket holds funds given for a specific purpose, like a missions trip, a building fund, or a special community outreach event.

- Grants: Support received from foundations or other organizations, usually tied to specific programs.

- Program Service Fees: Income you might generate from activities like a preschool, a summer camp, or a special conference.

This is also where we run into one of the most important concepts in nonprofit accounting: donor restrictions. All revenue has to be classified based on whether the donor specified how it must be used. We'll dig into this more later, but it's a critical piece for maintaining accountability and trust.

Classifying Your Ministry Expenses

Next up is the middle of the story, which details how your organization used its resources. Expenses are all the costs you incurred to run your ministry, and they aren't just thrown onto the page randomly. Generally Accepted Accounting Principles (GAAP) require them to be grouped into functional categories that explain their purpose.

A functional expense classification tells the "why" behind your spending. It connects every dollar spent back to a specific part of your mission, giving a crystal-clear view of your ministry's priorities and operational efficiency.

For most nonprofits and churches, expenses get sorted into three main buckets:

- Program Services: These are the costs directly tied to your mission-driven activities. This is the heart of what you do—think expenses for worship services, youth groups, community outreach, and mission trips.

- Management and General: Often called administrative or overhead costs, these are the essential operational expenses that keep the whole organization running. This includes things like staff salaries, office supplies, utilities, and accounting services.

- Fundraising: This category captures any costs associated with raising money. That could be the expense of running a capital campaign, putting on a special fundraising event, or creating appeal materials.

Getting the allocation right across these categories is a huge deal. For a deeper look at this process, you can learn more about creating a statement of functional expenses in our detailed guide. That report is what provides the detailed breakdown that feeds into your main statement of activities.

Calculating the Change in Net Assets

Finally, the end of the story reveals the bottom line. The Change in Net Assets is simply your total revenue minus your total expenses. This single figure is the most direct indicator of your financial performance for the period.

If your revenue is higher than your expenses, you have a positive change in net assets, often called a surplus. That's a great sign—it means your organization brought in more than it spent, strengthening its financial position.

On the flip side, if expenses outpace revenue, you have a negative change in net assets, or a deficit. This isn't always a cause for alarm, especially if it was planned for a major one-time project. But a recurring deficit is a clear signal that it's time to make some strategic adjustments, either by boosting revenue or managing costs more effectively. This one number ties the whole report together, giving you a powerful summary of your financial story for the year.

Understanding Donor-Restricted Funds

This is the one concept that truly sets nonprofit financial reporting apart from the business world. While a company has "equity," a nonprofit has net assets, which are split into two legally distinct categories. Getting this right is the key to a compliant statement of activities and, more importantly, to demonstrating you're a trustworthy steward of the funds you receive.

Think of it like managing your household budget with two separate bank accounts. One is your everyday checking account—it pays the mortgage, buys groceries, and covers utility bills. It's flexible. The other is a special savings account you’ve set aside strictly for your child's college education. You simply can't dip into that college fund to pay for a new car, no matter how much you need one.

That same principle governs your church's finances. Your net assets fall into two buckets:

- Net Assets Without Donor Restrictions: This is your "checking account." It’s where general tithes and offerings land, giving your leadership the flexibility to direct those funds to any ministry need, whether it's paying salaries or funding a pizza night for the youth group.

- Net Assets With Donor Restrictions: This is your legally-bound "college fund." These are gifts given for a specific purpose (like a building fund), a project (like a missions trip), or a particular timeframe (like an endowment).

Mastering the difference between these two types of net assets isn't just an accounting exercise—it's a legal and ethical requirement. It's the foundation of donor trust and ensures your ministry honors the heart behind every single gift.

How This Works in a Church Setting

Let's walk through a real-world example. Say your weekly offering brings in $5,000. This is classic revenue without donor restrictions. Your finance team can allocate it to the most pressing needs—staff salaries, curriculum, or community outreach.

Now, imagine the next week you hold a special offering for a summer missions trip and raise $10,000. This revenue comes with donor restrictions. Those funds are legally earmarked only for that missions trip. You can't use them to cover a shortfall in the general budget; doing so would be a serious breach of your fiduciary duty.

Releasing Funds from Restriction

A restriction isn't always permanent. Once you've fulfilled the donor's specific purpose, the net assets are "released" from their restriction. This is a critical entry on your statement of activities.

Using our example, once the missions trip is over, the $10,000 in expenses are paid from that restricted fund. On your statement, you’ll show a $10,000 transfer out of the "with donor restrictions" column and into the "without donor restrictions" column, where it's immediately offset by the trip's expenses. This transaction clearly shows the funds were spent exactly as intended.

Keeping a close eye on these flows is essential for financial stability. From 2015 to 2019, 58% of nonprofits saw donation growth, but that trend flipped dramatically in 2020 when 37% saw donations decline. A well-organized statement of activities helps leaders see the shifts between restricted and unrestricted funds, which is critical for building resilience. You can dig deeper into these nonprofit financial trends to see how they might impact your planning.

Managing these classifications correctly is a huge deal, especially for churches that juggle multiple designated giving campaigns. This is precisely why fund-based accounting systems like Grain Ledger are so helpful. They are built to track each fund automatically, ensuring donor intent is always honored and your reports are always accurate without the manual gymnastics.

Bringing the Statement of Activities to Life

Theory is one thing, but seeing how a statement of activities works in the real world is where it all clicks. Let's move past the definitions and walk through a practical example for a fictional church. This will transform the report from a page of numbers into a clear story about your ministry's financial health.

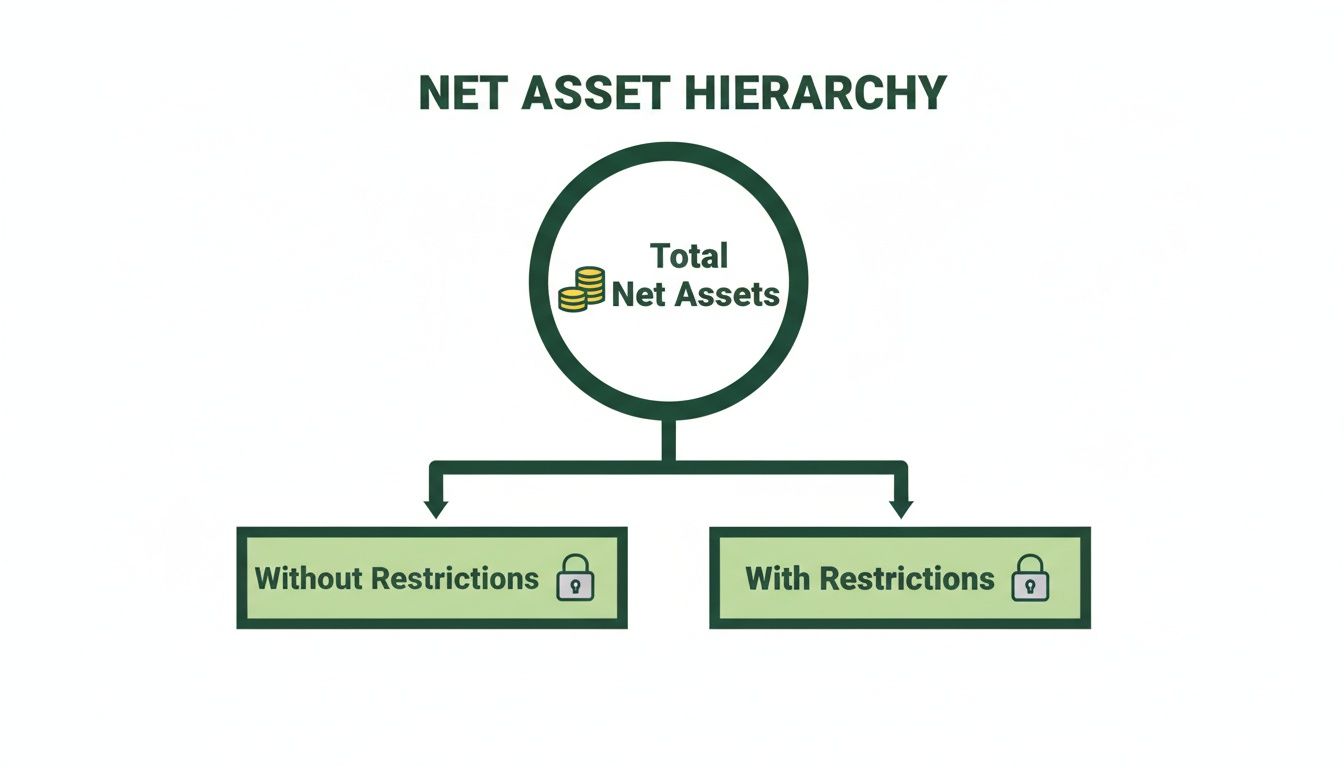

Imagine your church manages a General Fund for everyday operations and a separate, restricted Missions Fund. The statement of activities is designed to show you exactly how both of these funds performed over the year, side-by-side.

This diagram shows the fundamental split at the heart of the report: how your total net assets are divided into funds with and without donor restrictions.

This visual is crucial. It represents the financial firewall between flexible funds your church can use for anything and purpose-bound funds that are legally and ethically tied to a specific donor's intent.

A Step-by-Step Example

Let's break down a simplified statement line by line. We'll start with revenue, move to expenses, and see how they combine to show the change in your church's net assets.

1. The Revenue Section

The top of the report is all about income. It carefully organizes every dollar received into the correct category based on donor intent.

- Tithes & Offerings: Here we see $250,000 in general giving. Since these funds have no specific designation, they land squarely in the "Without Donor Restrictions" column. This is the money that fuels your primary budget.

- Missions Fund Donations: The church also received $50,000 specifically for missions. This amount goes directly into the "With Donor Restrictions" column because it’s earmarked for a single purpose.

- Net Assets Released from Restriction: This line is where the magic happens. It shows $40,000 moving out of the restricted column (as a negative number) and into the unrestricted column (as a positive one). Why? This entry signifies that $40,000 of the restricted mission funds were spent on their intended purpose during the year.

This "release" process is fundamental to nonprofit accounting. It’s how you prove you’ve honored a donor’s wishes, which then allows the funds to be officially used to cover the related expenses.

2. The Expenses Section

Next up are the expenses, all neatly categorized by function—like worship, outreach, or administration. Notice one critical detail: all expenses are recorded in the "Without Donor Restrictions" column. That’s because you can only pay bills with available, unrestricted cash, which now includes the money that was just released from the missions fund.

- Worship Ministry: Costs for services, music, and tech total $110,000.

- Outreach & Missions: This bucket, totaling $80,000, includes both local outreach and the mission trips funded by the released donations.

- Administration: General operating costs like salaries, utilities, and office supplies come to $90,000.

A key insight here is that expenses themselves are never "restricted." The net assets used to pay for them are. The report's structure brilliantly clarifies this distinction, showing exactly how restricted gifts fulfill their purpose by supporting specific ministry expenses.

Comparing Statement of Activities Presentation Formats

How you present this information can make all the difference between confusion and clarity. While a simple, consolidated report might be technically compliant, a columnar format that breaks down activity by fund is far more insightful, especially for a church.

The table below highlights why a fund-based view is the gold standard for ministry leadership.

| Reporting Element | Consolidated View (Single Column) | Fund-Based View (Columnar) |

|---|---|---|

| Revenue Clarity | Shows a single total revenue figure, obscuring the source and purpose of funds. | Clearly separates general tithes from designated missions gifts, showing the health of each fund. |

| Restriction Tracking | Makes it difficult to see if restricted funds were used properly without manual cross-referencing. | Visibly tracks the release of restricted funds, providing a clear audit trail of donor stewardship. |

| Decision-Making | Can lead to misinterpretations, like thinking a large total balance is entirely available for general use. | Empowers leaders to see exactly what's available for the general budget versus what is legally earmarked. |

For church leaders, the columnar, fund-based view isn’t just a nice-to-have; it's essential. It gives you the transparency to answer a member’s questions with confidence and allows your board to make strategic decisions based on a true understanding of available resources.

This is precisely the level of detail that specialized accounting platforms like Grain Ledger are built to produce automatically, ensuring your statement of activities is always accurate, insightful, and ready for review.

A Step-by-Step Guide to Preparing Your Statement

Putting together an accurate statement of activities can feel a bit like assembling a complex puzzle. But with a clear process, it becomes a manageable, even insightful, task. A systematic approach helps your finance team transform raw data into a compliant report that tells a trustworthy story of your ministry's financial stewardship.

Think of it like following a detailed recipe. You need to gather all the right ingredients, measure them carefully, and combine them in the correct order. These steps provide that recipe for a clean, clear financial statement.

Step 1: Consolidate Your Financial Records

The foundation of any financial report is having all your data in one place, and making sure it’s accurate. Before you can start classifying anything, you have to gather every single financial transaction from the reporting period—whether it’s a month, a quarter, or a full year.

This means pulling together:

- All income sources: Giving records, bank deposits, grant award letters, and event revenue.

- All expense records: Invoices, receipts, payroll reports, and credit card statements.

- Bank and investment statements: These are essential for reconciling your cash balances and ensuring nothing fell through the cracks.

For churches, a purpose-built accounting solution like Grain Ledger is designed to make this step much easier. By integrating with your giving platforms and bank accounts, it captures all transactions automatically, which helps prevent those pesky manual data entry errors from the get-go.

Step 2: Classify All Revenue by Restriction

With all your income data collected, the next crucial step is to sort every dollar into one of two buckets: revenue with donor restrictions or revenue without donor restrictions. This isn't just an accounting rule; it's a legal and ethical obligation you have to your donors.

General tithes and offerings are almost always unrestricted. But funds from a special collection for a new roof or a designated missions offering are restricted and absolutely must be tracked separately. Getting this right is non-negotiable for maintaining donor trust.

Step 3: Categorize Every Expense by Function

Now, let's shift focus to the money going out. Every expense must be categorized by its function—the "why" behind the spending. The three main functional categories are:

- Program Services: These are costs directly tied to your core mission, like worship services, youth ministry, or community outreach.

- Management and General: Think of these as the administrative costs that support the entire organization—things like the pastor's salary, office utilities, and accounting fees.

- Fundraising: These are any expenses you incurred specifically to generate contributions, such as the costs for a capital campaign event.

A well-organized chart of accounts is your best friend here. For a little help, you can check out our guide on building a nonprofit chart of accounts that makes this part of the process much more straightforward.

This process of functional allocation is where many nonprofits struggle, especially when an expense like a staff member's salary supports multiple functions. A clear allocation policy is essential for consistency and compliance.

Step 4: Record the Release of Restrictions

As you spend designated funds on their intended purpose, you have to record a "release from restriction." This is simply an accounting entry that moves net assets from the restricted column over to the unrestricted column on your statement. It’s how you show that you've fulfilled the donor's wishes.

For example, when you pay for that mission trip using the funds donated specifically for it, you’ll record the expense and, at the same time, show the release of those restricted funds. This creates a crystal-clear audit trail.

Step 5: Assemble the Final Report

Finally, you can pull all the classified data together into the formal statement of activities format. Add up your revenue categories, subtract your functional expense totals, and calculate the final "Change in Net Assets" for the period.

This report becomes a vital tool for analysis. While the nonprofit sector saw a modest 2% increase in online revenue recently, performance varied widely. Organizations at the 25th percentile actually saw a 7% decline, which really highlights how crucial a detailed statement of activities is for understanding your own specific financial trends. You can discover more insights about these fundraising trends and what they mean for nonprofits.

Go Beyond Spreadsheets with True Fund Accounting

Trying to piece together a statement of activities using generic software or spreadsheets feels like a high-wire act, doesn't it? Every month, you’re tangled in complex calculations, double-checking every cell, and just hoping you haven’t misplaced a decimal or misclassified a restricted donation. This manual grind isn't just frustrating; it's a real risk to your organization's financial integrity.

When you're tracking different funds in separate spreadsheet columns, you're practically inviting human error to the party. One simple copy-paste mistake can throw everything off, leading to reports that don't paint an honest picture of your financial health. This leaves your leadership in a tough spot, forced to make mission-critical decisions with shaky data.

The Power of Automated Fund Tracking

This is where a true fund accounting system makes all the difference. Unlike basic bookkeeping tools that have been tweaked for nonprofit use, specialized software is designed specifically for the unique world of fund management. From the moment it’s entered, every single transaction—whether it's a designated gift for the youth group or a grant payment for a new outreach program—is tied directly to its specific fund.

This fundamental difference offers some serious advantages:

- Built-in Compliance: The system automatically enforces donor restrictions. You literally can't spend designated funds on general operating costs by accident.

- Error Reduction: When you get rid of manual data entry and tangled formulas, you drastically cut down the risk of costly accounting errors.

- Real-time Clarity: Your leadership team can pull an accurate, up-to-the-minute statement of activities with a single click, instead of waiting weeks for someone to reconcile everything by hand.

Why Churches Need Purpose-Built Tools

For a church juggling a general fund, designated missions, a building campaign, and more, this kind of automated clarity isn't a luxury—it's essential. It’s why a solution like Grain Ledger can have such an impact. It connects directly to your giving platforms and bank accounts, making sure every dollar flows into the correct fund automatically. You can dive deeper into how this works by exploring the core principles of fund accounting for nonprofits in our comprehensive guide.

Moving to a true fund accounting system isn't just an operational upgrade; it's a strategic shift. It frees up countless hours, eliminates critical compliance risks, and equips your ministry with the financial clarity needed to steward resources faithfully and effectively.

The nonprofit world keeps growing, and with that growth comes a need for better financial tools. Between 2007 and 2017, the number of 501(c)(3) organizations in the U.S. shot up by 28.9%, far outpacing the growth of for-profit businesses. This trend highlights why solid reporting, made simple through technology, is more important than ever—especially for small to medium-sized churches. You can read more about these national trends in nonprofit growth and employment to see why financial clarity is so crucial.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

Common Questions About Nonprofit Financials

When you're leading a ministry, diving into the financial reports can bring up a lot of questions. That’s perfectly normal. Getting straight answers is the first step toward confident stewardship and making smart decisions for your church's future. Let's tackle a few of the most common questions we hear from church leaders about the statement of activities.

Answering these helps connect the dots between accounting rules and the day-to-day reality of running a church. It all comes back to solid planning, clear accountability, and earning your donors' trust.

How Is a Statement of Activities Different from a Budget?

This is a classic question. It's easy to get the two confused, but they serve very different purposes. The easiest way to remember it is that one looks forward, and the other looks back.

- A budget is your financial roadmap for the future. It's your plan, outlining what you expect to bring in and spend over the next year to achieve your ministry goals.

- A statement of activities is a report card on the past. It shows what actually happened over a specific period, detailing the real income and expenses.

Think of it like a road trip. Your budget is the map you plan out before you start the car. The statement of activities is the GPS log after the trip is over—it shows the exact route you took, how much gas you really used, and where you ended up.

How Often Should We Prepare This Statement?

For compliance and annual member meetings, you'll need an official statement of activities once a year. But waiting 12 months to get a clear picture of your financial health is like driving with your eyes closed.

The best practice is to prepare and review a statement of activities at least quarterly. This gives your board or finance team a regular rhythm for spotting trends, catching potential budget shortfalls early, and making adjustments before small issues become big problems.

The good news is that modern accounting software makes this easy. For churches using a specialized fund accounting system like Grain Ledger, you can pull an up-to-the-minute statement of activities in just a few clicks. You get real-time insight whenever you need it.

Can We Use General Fund Tithes for a Building Project?

This question goes right to the heart of donor intent—one of the most important ethical and legal principles in nonprofit finance. The answer hinges entirely on how the funds were given.

Tithes and offerings given to the general fund are typically considered unrestricted net assets. This means donors gave them without specifying a purpose, trusting your leadership to use them for any aspect of the ministry, which could include a building project.

However, if you ran a capital campaign for a "Building Fund," every dollar given to that specific campaign is a restricted net asset. That money can only be used for the building project. Dipping into those funds to cover a general budget shortfall would break the trust you have with those donors and violate your legal responsibility. Keeping this distinction crystal clear is the cornerstone of good stewardship.

Ready to simplify your church's financial reporting and ensure every dollar is accounted for correctly? With Grain Ledger, you can automate fund tracking and generate an accurate statement of activities in minutes. Learn more and Schedule a Demo today at grainledger.com.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.