What Is an Encumbrance in Accounting?

What is an encumbrance in accounting? Learn how it works with clear examples, and see why it's a vital tool for non-profit and church budget control.

Let's get straight to it: an encumbrance in accounting is a reservation of funds for a future expense.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Think of it like putting an item on hold at a store. You haven't paid for it yet, but you've mentally (and in this case, officially) set aside the money. That cash is now spoken for, so you can't go spend it on something else.

What Encumbrance Accounting Really Means

While standard accounting is mostly a look in the rearview mirror—tracking what you've already spent—encumbrance accounting adds a windshield. It tracks not just your expenses but your commitments. This proactive approach is the secret to preventing overspending and getting a true handle on your available budget.

An encumbrance is created the moment your organization makes a formal promise to spend money. The most common trigger is issuing a purchase order for new Bibles or signing a contract for a new HVAC system. At that exact moment, even before an invoice arrives or a single dollar leaves your bank account, a portion of the budget is officially earmarked.

Understanding the Financial Impact

This practice isn't just "nice to have"—it's essential for any organization that lives by a budget. This is especially true for churches and nonprofits, where every dollar is tied to donor trust and mission-critical goals. By recording these commitments as they happen, you get a real-time, honest view of your financial position. Without it, your budget reports are always telling an incomplete story.

An encumbrance acts as a placeholder against your budget. It reduces your "available balance" immediately, ensuring that funds promised for one purpose aren't accidentally spent on another.

This forward-looking perspective is a game-changer for managing restricted funds. Imagine your church has a designated building fund. When you sign a $50,000 contract with a builder, encumbering that amount gives you an immediate and accurate picture of the actual remaining capital. Proper financial stewardship under FASB ASC 958 guidelines for nonprofits absolutely depends on controls like this to honor donor intent.

Encumbrance vs Expense At a Glance

To make this crystal clear, it helps to see these two concepts side-by-side. An encumbrance is a promise to spend, while an expense is the record of that spending after it has happened.

| Attribute | Encumbrance | Expense |

|---|---|---|

| What It Is | A commitment or obligation to spend money | An actual cost incurred for goods or services received |

| Timing | Recorded when a purchase order or contract is issued | Recorded when an invoice is received and approved for payment |

| Financial Impact | Reduces the available budget balance | Reduces both the budget balance and cash/accounts payable |

| Purpose | To prevent overspending and control the budget | To accurately report historical financial performance |

In short, the encumbrance holds the spot in the budget, and the expense eventually fills it once the transaction is complete.

How It Works in Practice

Also known as commitment accounting, this method is a cornerstone of financial management in government, schools, and savvy nonprofits. By recording commitments like purchase orders as encumbrances, you reserve those funds at the moment the obligation is made, not weeks or months later when the payment is due.

Ultimately, it provides the answer to the most critical question every ministry leader asks: How much do we truly have left to spend? By subtracting both your actual expenses and your committed encumbrances from the budget, you finally arrive at your true, uncommitted available balance.

Protecting Your Mission with Encumbrances

For a church, a budget is so much more than a spreadsheet of numbers. It's a statement of faith, a roadmap for your mission, and a promise to your donors. This is exactly why encumbrance accounting isn't just a technical bookkeeping practice—it's a vital tool for safeguarding your church's commitments.

Think about a special fund you've set up, like one for a new building wing or a specific missions trip. These are restricted funds, meaning that money is ethically and often legally bound to a single purpose. Encumbrances are your best defense to protect those funds, making sure money set aside for a new roof doesn’t accidentally get spent on new sound equipment.

By setting aside the funds the moment a commitment is made, encumbrances act as a powerful, proactive control. It effectively stops overspending in its tracks, long before the invoice arrives.

Upholding Donor Trust and Accountability

When someone gives to a specific campaign, they're not just donating money; they're placing their trust in your stewardship. Encumbrance accounting gives you a practical way to honor that trust. It creates a clear, transparent trail showing how you’re managing their gifts responsibly, from the moment a decision is made to the final check being cut.

This isn't just about good bookkeeping; it's about maintaining financial integrity. It shifts your financial reporting from being a backward-looking history of what happened to a forward-looking guide for what’s possible. That kind of clarity is priceless for pastors, board members, and finance committees who need to make smart decisions with real-time, accurate data.

Encumbrances transform your budget from a static document into a dynamic management tool. They ensure that every financial decision aligns with your strategic priorities and honors the intent behind every donation.

A Standard for Financial Integrity

This proactive approach to budgeting isn't some niche practice. In fact, it's a cornerstone of financial management in the public sector, used by government agencies and universities that manage trillions of dollars every year. Departments rely on encumbrance reports to track their commitments against their budgets, a critical internal control when those pending obligations can represent 10-20% or more of their total spending. You can learn more about how fiscal officers use encumbrances at uci.edu to prevent budget overruns.

Bringing this standard into your church offers some immediate, powerful benefits:

- Prevents Overspending: It makes it practically impossible to spend the same dollar twice, protecting your overall financial stability.

- Improves Budget Accuracy: Your budget reports start to reflect reality by showing the true available balance, not just what's left in the bank account.

- Strengthens Internal Controls: It naturally creates a stronger approval process, as commitments have to be recorded before they can turn into actual expenses.

- Builds Donor Confidence: It showcases a high level of financial discipline and accountability, which encourages people to continue supporting your mission.

So, what is an encumbrance in church accounting? At its heart, it’s a promise keeper. It's the system that ensures your financial actions always line up with your mission’s purpose.

Recording Encumbrance Journal Entries Step by Step

Knowing what an encumbrance is in theory is great, but seeing it work in your books is where it all clicks. Let's walk through the actual bookkeeping, turning this financial concept into a straightforward, repeatable process. The entire lifecycle of an encumbered transaction really just boils down to three key stages.

This visual helps show how the process acts as a safeguard, protecting your mission funds from the moment a budget is set to the final, secure outcome.

Think of each step as a checkpoint, locking down committed funds to make sure they're used exactly as intended and not accidentally spent elsewhere.

Stage 1: Creating the Encumbrance

This first step happens the moment your church makes a formal commitment. Let's say you decide to buy new curriculum for the youth group and issue a purchase order (PO) to a supplier for $2,500. Right then and there, you create a journal entry to "encumber," or set aside, those funds.

To do this, you’ll debit the Encumbrances account and credit a corresponding equity account, which is usually called Reserve for Encumbrances.

- Debit: Encumbrances $2,500

- Credit: Reserve for Encumbrances $2,500

This entry doesn't touch your cash or your actual expense lines. It's simply a budgetary placeholder. Its only job is to reduce your available budget balance, preventing that $2,500 from being promised to another ministry.

Stage 2: Reversing the Encumbrance

A few weeks go by, and the curriculum finally arrives with an invoice. The commitment is no longer a future promise—it has become a real, tangible liability. So, the very first thing you need to do is get rid of the placeholder you created in Stage 1.

You just reverse the original entry. This clears out the encumbrance accounts for this specific transaction, getting them ready for the next one.

- Debit: Reserve for Encumbrances $2,500

- Credit: Encumbrances $2,500

This step zeroes out the encumbrance and makes way for the actual expense to be recorded. It's a critical bit of housekeeping that keeps your budget reports clean and accurate.

Think of it like taking an item off "hold" at a store. The item is now in your shopping cart (an invoice has arrived), so the hold isn't needed anymore. You're now ready to go to the register and record the real purchase.

Stage 3: Recording the Final Expense

With the placeholder gone, you can finally record the actual expense just as you would any other bill. Assuming the final invoice was exactly $2,500, you now book the real transaction. This is what will impact your expense accounts and your liabilities (Accounts Payable).

The entry is probably one you're very familiar with:

- Debit: Youth Curriculum Expense $2,500

- Credit: Accounts Payable $2,500

This is the entry that officially hits your budget and shows up on your statement of activities or income statement.

But what if the invoice amount is different? Say the invoice came in at $2,450. You would still reverse the full original encumbrance of $2,500. Then, you record the actual expense of $2,450. That $50 difference? It’s automatically released back into your available budget.

To make this flow even clearer, here’s a table breaking down the journal entries at each stage of a typical encumbered purchase.

Encumbrance Accounting Workflow

| Stage | Action | Debit Entry | Credit Entry |

|---|---|---|---|

| 1. Purchase Order Issued | A $2,500 PO is sent to the curriculum vendor. The funds are now committed. | Encumbrances $2,500 | Reserve for Encumbrances $2,500 |

| 2. Invoice Received | The curriculum arrives with an invoice. The placeholder entry is now reversed. | Reserve for Encumbrances $2,500 | Encumbrances $2,500 |

| 3. Expense Recorded | The actual expense is booked as a payable, reflecting the true cost. | Youth Curriculum Expense $2,500 | Accounts Payable $2,500 |

| 4. Payment Made | The church pays the invoice, reducing cash and clearing the liability. | Accounts Payable $2,500 | Cash $2,500 |

Following these distinct steps ensures your budget reports remain accurate from the moment a spending decision is made until the final check is cut. It’s a complete cycle that maintains financial integrity from start to finish.

Encumbrances in Action: Real-World Scenarios

Alright, let's move past the theory. The best way to really wrap your head around encumbrances is to see them play out in situations your church or nonprofit handles every day. We’ll walk through two common examples.

First, we’ll look at a simple, everyday purchase paid for from the general operating budget. Then, we’ll tackle a much bigger project—one funded by a special, restricted fund. In both cases, we'll follow the money from the initial promise to the final payment, showing exactly how encumbrances give you that critical financial foresight.

Scenario 1: An Everyday Purchase from the General Budget

Let's say your education department needs new Sunday school curriculum. They get a quote and issue a purchase order for $1,500.

That purchase order is the trigger. It’s a formal commitment to the vendor.

This is the moment the encumbrance is born. Instead of waiting for the invoice to arrive, your bookkeeper immediately encumbers $1,500 against the education budget. Right away, the department's "available balance" shrinks by that amount, even though a single dollar hasn't left the bank.

This simple step is a powerful safeguard. It prevents the department from accidentally double-spending that money on something else, keeping them firmly within their annual budget.

A few weeks later, the curriculum shows up, along with an invoice for the expected $1,500. At this point, the bookkeeper does two things:

- Reverses the $1,500 encumbrance entry (its job is done).

- Records the actual $1,500 expense, now that the bill is in hand.

The financial story is now complete, accurate at every stage from promise to payment.

Scenario 2: A Major Project with Restricted Funds

Now for a more complex example. Your church has a dedicated $250,000 building fund, which was generously donated for a sanctuary renovation. After getting bids, you sign a contract with a construction company for $220,000.

That contract represents a huge commitment. The moment it’s signed, your bookkeeper should encumber the full $220,000 against the restricted building fund.

This immediately shows leadership that while $250,000 is technically in the fund, only $30,000 is actually left for any surprises or add-ons. That kind of real-time clarity is absolutely essential for stewarding major donor-restricted projects responsibly.

This practice isn't new; encumbrance accounting became a standard in the mid-20th century as a way to manage the sprawling budgets of public sector and nonprofit organizations. It provided a much-needed tool for fiscal discipline, and you can discover more insights about its history on fiveable.me.

As the renovation moves forward, the contractor submits monthly invoices. With each invoice—say, for $50,000—your bookkeeper reverses a portion of the total encumbrance and records the actual expense. This process gives everyone a clear, running total of what’s left in the project budget, helping you avoid catastrophic overspending and demonstrate incredible accountability to your congregation.

Reporting and Managing Encumbered Funds

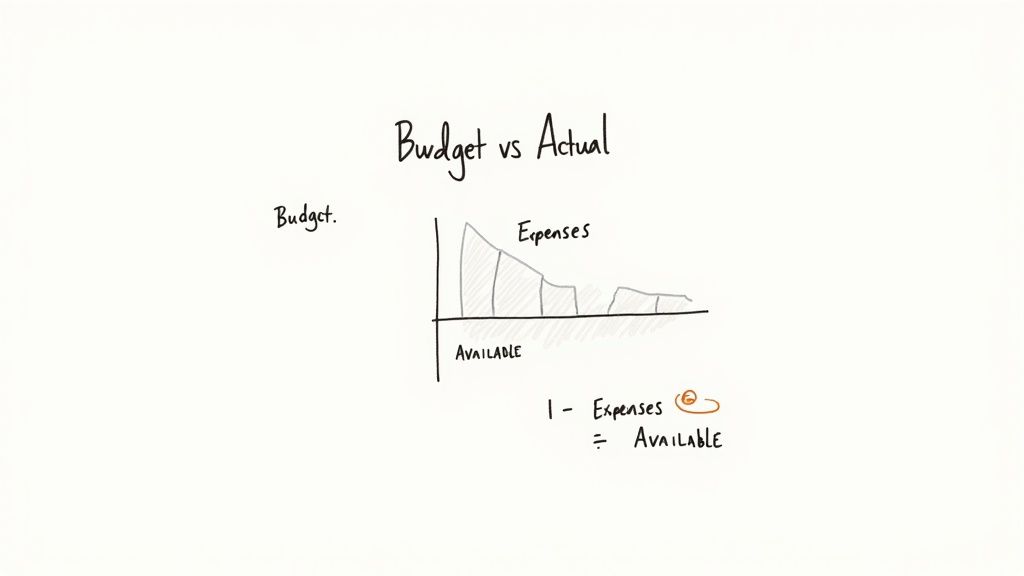

Just recording encumbrances is only half the battle. The real magic happens when you can clearly see their impact on your budget, and that's where your financial control truly sharpens. Standard financial reports often give you a rearview mirror perspective—they show what you’ve already spent but leave you blind to the commitments you’ve already made. This is where a slightly modified report becomes your most powerful tool.

The go-to report for any budget manager is the Budget vs. Actual report. By itself, it’s useful. But to make it truly effective, you need to add a third, crucial column: Encumbrances. This one addition transforms the report from a simple historical record into a forward-looking guide that prevents overspending before it happens.

The Formula for Financial Clarity

With this enhanced report, you can finally calculate your true spending power. The formula is simple but incredibly insightful, revealing exactly what’s left for new initiatives or unexpected needs.

Budget - Encumbrances - Actual Expenses = True Available Balance

This calculation gets to the heart of what encumbrance accounting provides: an honest, real-time picture of your financial position. It stops you from making the classic mistake of thinking that cash in the bank equals cash available to spend.

This kind of clarity is essential for building a transparent financial system. A well-organized chart of accounts for your nonprofit creates the right foundation, and robust encumbrance reporting brings that structure to life with data you can actually use.

Best Practices for Managing Encumbrances

To keep your financial data trustworthy, ongoing management is just as important as making the initial journal entries. A few solid habits will ensure your reports stay clean, accurate, and reliable.

- Regularly Review Open Purchase Orders: Make it a monthly habit to review all outstanding POs. Are those commitments still valid? Has a project been canceled or put on hold? Closing out old, irrelevant encumbrances is an easy way to free up budgeted funds that were otherwise tied up.

- Establish a Clear Year-End Process: Decide ahead of time how you'll handle open encumbrances when the fiscal year ends. Most organizations either let them lapse (requiring new POs in the new year) or formally carry them over by re-appropriating the funds in the next budget.

- Automate Where Possible: Let's be honest, manually tracking encumbrances is tedious and a recipe for human error. Using accounting software that automatically creates encumbrances from purchase orders—and reverses them when invoices are paid—is the most reliable way to maintain accuracy.

Following these practices ensures your financial reports aren't just an exercise in record-keeping but a dynamic tool for proactive stewardship.

Using Software to Automate Encumbrance Tracking

https://www.youtube.com/embed/ZAr8RL82Qq4

Trying to keep track of encumbrances manually, maybe in a separate spreadsheet, is a massive headache. It's not just tedious work; it's practically an open invitation for human error, which can lead to some costly mistakes down the line.

The good news is that modern accounting software can completely flip the script. It turns this manual chore into an automated, powerful financial control, saving you a ton of time while making your numbers far more reliable.

Instead of hand-keying journal entries for every single financial promise you make, the right software handles it all behind the scenes. The moment you create a purchase order, for instance, the system can automatically set aside—or encumber—those funds. It then instantly checks that amount against your budget. This simple, automated step is your best defense against overspending, stopping it before it even happens.

Gaining Real-Time Financial Visibility

This kind of automation gives ministry leaders a clear, trustworthy view of all financial commitments at any given moment. You can finally say goodbye to the guesswork and the nail-biting wait for month-end reports to figure out where you truly stand financially.

Here’s a look at how a system like Grain generates a purchase order, which is what kicks off the whole automated encumbrance process.

This simple, clean form captures all the key details—the vendor, what you're buying, and the costs. That's all the data the system needs to automatically reserve the funds from the correct budget line.

By linking purchase orders directly to the general ledger, the system ensures that your budget reports always reflect both what you've spent and what you've promised to spend.

This tight integration is a hallmark of true fund accounting software for churches. It lets you make strategic, confident decisions without getting bogged down in manual data entry. Ultimately, it transforms your budget from a static, once-a-year document into a dynamic, living tool for responsible stewardship.

Common Questions About Encumbrances

We've covered a lot of ground on what encumbrance accounting is and how it works. To finish up, let's tackle a few of the questions that almost always come up when leaders and bookkeepers first start using it.

Do We Really Have to Use Encumbrance Accounting?

While it’s not a strict GAAP rule for every single non-profit out there, it is absolutely a best practice for any organization serious about managing budgets and protecting restricted funds. For government entities, it's pretty much non-negotiable.

For a church, adopting this practice sends a powerful message. It shows your board, your donors, and your congregation that you are committed to the highest level of financial responsibility and transparency. It’s a tool for building trust.

What's the Real Difference Between an Encumbrance and Accounts Payable?

It's helpful to think of it as the difference between a plan and a bill.

An encumbrance is just a commitment—a reservation of budget funds for something you've ordered but haven't received yet. On the other hand, accounts payable is a real liability for goods or services you have already received and have an invoice for.

The encumbrance is like a temporary earmark. Once the invoice comes in and you officially owe the money, that earmark is removed, and it becomes a formal accounts payable entry. One looks forward to manage your budget; the other looks backward to record what you owe.

What if We Spend Less Than We Originally Encumbered?

That's a great outcome, and it happens all the time! Maybe you got a discount, or the final shipping cost was lower than the estimate. The accounting process is simple and clean.

When the actual bill arrives, you first reverse the entire original encumbrance amount. Then, you record the actual, lower expense from the invoice. The leftover amount—the difference between your original estimate and the final cost—is automatically freed up and returned to your available budget. It keeps your financial picture honest and up-to-the-minute.

Ready to stop wrestling with spreadsheets and gain real-time visibility into your church's finances? Grain is purpose-built with true fund accounting to automate encumbrance tracking, protect restricted funds, and provide the clarity you need for confident stewardship. Schedule a Demo today!

Ready to simplify your church finances?

Schedule a demo to see Grain Ledger in action, or sign up for product updates.