How to Read a Cash Flow Statement: A Simple Guide for Churches

Jun 26, 2023

When you first glance at a cash flow statement, it might seem like just another page of numbers. But it’s actually telling a story—the real, boots-on-the-ground story of how money is actually moving through your church. It answers the questions that keep ministry leaders up at night: "Do we have enough cash to make payroll?" or "Can we truly afford that new sound system?"

Why Your Cash Flow Statement Matters More Than You Think

Your income statement might show that you’re “profitable” on paper, but the cash flow statement reveals the hard truth about your liquidity. It tracks the actual dollars flowing in and out of your bank accounts, cutting through the accounting noise to show you what you can really afford right now.

Think of it this way: the income statement is the plan, but the cash flow statement is the reality.

The good news is, you don’t need to be a CPA to understand it. The statement is broken down into three distinct parts, each revealing a different chapter of your church’s financial journey.

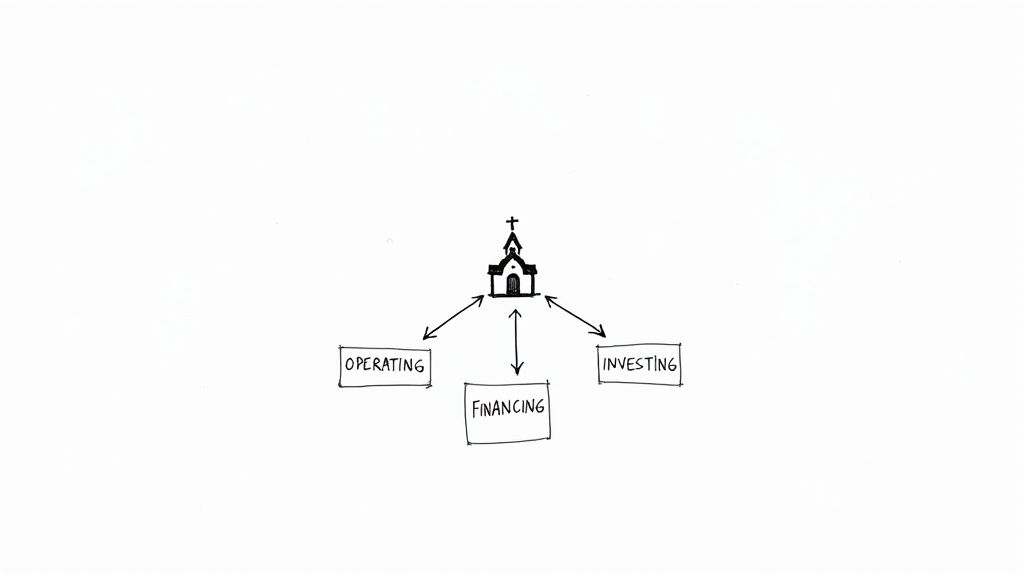

A Story in Three Parts

Every cash flow statement is built around three core activities. Each one answers a fundamental question about how your church is managing the resources God has provided.

Operating Activities: This is the lifeblood of your ministry. It reflects the cash coming in from tithes and offerings minus the cash going out for day-to-day expenses like salaries, rent, and utilities.

Investing Activities: This section covers the big-ticket items. It tracks cash spent on or received from long-term assets—think purchasing property, selling an old church van, or upgrading your worship equipment.

Financing Activities: This part tells the story of how you handle major capital and debt. It includes things like making mortgage payments, taking out a loan, or receiving a large, restricted gift for a new building project.

To put it simply, each section gives you a different piece of the puzzle. Here’s a quick way to think about what each one tells you.

The Three Stories Your Cash Flow Statement Tells

This table summarizes what each section reveals about your church's financial activities and overall health.

Section | What It Tells You | The Core Question It Answers |

|---|---|---|

Operating | Whether your core ministry operations are generating more cash than they consume. | "Is our day-to-day ministry financially self-sustaining?" |

Investing | How you are putting money to work for the future by buying or selling major assets. | "Are we investing in our long-term mission and growth?" |

Financing | How you are managing debt and funding large-scale projects. | "How are we handling our debts and major capital needs?" |

By looking at these three areas together, you get a clear, unfiltered picture of your church's financial reality.

It’s the critical difference between knowing you earned money on paper and knowing you actually have that money in the bank to spend on your mission.

This distinction is absolutely vital for effective stewardship. A church can easily look healthy on an income statement but be facing a cash crunch because of uncollected pledges or large, non-cash expenses. To see how this report fits in with others, check out our complete guide to church financial statements.

Ultimately, learning to read this statement empowers you to lead with confidence, ensuring every dollar is stewarded well and aligned with your ministry's calling.

Understanding Your Operational Cash Flow

The first, and arguably most important, section of your cash flow statement is Operating Activities. Think of this as the financial pulse of your day-to-day ministry. It shows the cash coming in from your core mission—tithes, offerings, program fees—and the cash going out to keep the lights on and the staff paid.

This is where the rubber meets the road, financially speaking.

Ultimately, this section answers a critical question: Is our daily ministry generating enough cash to sustain itself? A consistently positive number here is a fantastic sign. It tells you that your regular income is more than enough to cover regular expenses, without having to touch savings or take on debt.

Direct vs. Indirect Method

You'll see operating cash flow calculated in one of two ways: the direct method or the indirect method.

Direct Method: This one is exactly what it sounds like. It simply lists all the cash that came in (like offerings) and all the cash that went out (like salaries). It's easy to understand but can be a real headache to put together.

Indirect Method: This is the one you’ll see almost everywhere. It starts with the net income from your Statement of Activities and then makes a few clever adjustments for non-cash items.

Why do most churches use the indirect method? Because it brilliantly connects your income statement (which isn't purely about cash) to what's actually in your bank account. It shows you the difference between what you earned on paper and the cash you have on hand.

Depreciation is the classic example. Your income statement lists it as an expense, which lowers your net income. But no cash actually left the building for depreciation. The indirect method adds that amount back, giving you a much clearer picture of your real cash position. Keeping this straight requires a clean ledger, which all starts with a solid plan. For a deeper dive, check out our guide on how to build a chart of accounts for nonprofits.

A Real-World VBS Scenario

Let's ground this in something familiar. Imagine your church just wrapped up a successful Vacation Bible School (VBS).

You brought in $5,000 in registration fees from families—a direct cash inflow. Over the month, you also spent $3,000 on VBS supplies, snacks, and curriculum, all paid with cash.

On your cash flow statement, these transactions would show up in the Operating Activities section as a $2,000 net increase in cash. Seeing that direct link between a ministry event and your church's financial health is incredibly empowering. It proves that your programs don't just serve the community; they contribute to your financial stability. This is exactly the kind of clarity that tools like Grain Ledger are built to provide, tracking these ministry-specific cash flows automatically.

Looking Beyond Day-to-Day Operations: Investing and Financing

Your operating activities give you a snapshot of your church’s day-to-day financial pulse, but the next two sections reveal the bigger picture—your long-term vision. This is where you see the strategic moves your church is making to build for the future.

When you learn to read this part of the cash flow statement, you start to understand the story behind your church’s growth, its approach to debt, and how it handles major capital projects.

Investing in the Future of Your Ministry

The Cash Flow from Investing Activities section tracks how your church puts its money to work by buying or selling long-term assets. This isn’t about the weekly curriculum or coffee supplies; it’s about the big-ticket items that will support your mission for years.

Think of things like:

Purchasing new equipment: This could be that new sound system for the worship center, a van for outreach events, or even just new computers for the office staff.

Property and building transactions: Buying or selling land, or spending on a major facility renovation, will show up here as a cash outflow.

Selling off old assets: If you finally sell that old church bus, the cash you get for it appears as a cash inflow right here.

It might seem counterintuitive, but a negative number in this section is often a great sign for a church. It means you're actively investing in your mission, turning cash into tangible assets that will serve your congregation and community.

A big cash outflow here could mean you're renovating the children's ministry wing or buying the property next door for that expansion you've been dreaming about. These are the footprints of a forward-thinking ministry, as long as these investments are planned and financially sustainable.

How Your Church Handles Debt and Major Funding

Next, the Cash Flow from Financing Activities section tells the story of how your church manages its debt and handles large-scale funding. This part of the statement provides crucial accountability for how you handle borrowed money and significant designated gifts.

This section typically includes:

Loan activity: You'll see cash coming in from taking out a new loan or cash going out as you make principal payments on an existing mortgage.

Capital campaign funds: When your church receives a large, designated gift for something like a building fund, it's recorded here as a cash inflow.

For example, let's say your church secures a $200,000 loan for a new roof. That $200,000 shows up as a positive cash flow from financing. Then, each mortgage payment you make is split—the interest portion hits your operating activities, but the principal portion shows up here as a cash outflow.

Managing these transactions, especially when they involve restricted funds, requires incredible attention to detail. You have to ensure that money designated for a capital project is tracked separately and used only for its intended purpose. If you want to dive deeper into this, our guide on fund accounting for churches is a must-read; it’s a foundational concept for good stewardship.

This is exactly where tools like Grain Ledger become indispensable. Because it's a true fund accounting system, a donation to the "Building Fund" automatically flows into the correct restricted fund. It then generates clear reports showing exactly how those funds were received and spent, removing the headache of manual tracking and giving your congregation the transparency it deserves.

Tying It All Together: Your Church's Financial Story

A cash flow statement is so much more than a list of ins and outs. It's a story. When you learn to connect the dots between the operating, investing, and financing sections, you can see the whole picture of your church's financial health and direction.

Think about it this way: a big purchase in the investing section, like new sound equipment for the worship team, is often directly linked to a new loan showing up in the financing section. Spotting these connections is the difference between just reading numbers and becoming a truly savvy ministry strategist.

This is the cycle of growth in action—strategic investments, made possible by thoughtful financing, that ultimately expand your ministry's reach.

The One Number That Shows Your True Ministry Potential

If you really want to gauge your church's capacity for growth, there's one metric you absolutely need to know: Free Cash Flow (FCF). It’s a game-changer.

FCF tells you the exact amount of cash your church has left after covering both day-to-day operations and investing in long-term assets. This is the money you're free to use for new ministry initiatives, paying down debt ahead of schedule, or building up a rainy-day fund. It’s one of the clearest indicators of your financial strength and flexibility.

The formula is refreshingly simple:

Free Cash Flow = Cash Flow from Operations - Capital Expenditures

Capital Expenditures (often called CapEx) are just the funds you spend on physical assets like buildings, vehicles, or major equipment. You'll find this number under the Investing Activities section. A healthy, positive FCF shows that your core operations are generating more than enough cash to handle your present needs and fund your future vision.

What Free Cash Flow Looks Like in Real Life

Let’s make this practical. Say your cash flow statement shows these figures:

Cash Flow from Operations: $75,000

Purchase of New Van (CapEx): -$15,000

Your Free Cash Flow is $60,000. That $60,000 is what you have to work with. It's the real, unrestricted cash available to launch that community food bank you've been dreaming about or to finally hire a dedicated youth pastor—all without taking on new debt.

This isn't just a church thing; it's a critical measure for any healthy organization. The global cash flow management market was valued at US$736.33 million in 2023, and it's growing because leaders understand that cash flow is the key to strategic decision-making. Investors live and die by FCF when they're evaluating a company's ability to grow. We can bring that same level of financial discipline to our stewardship, ensuring we’re always ready for the next step in our mission. If you're interested, you can read more on these market trends to see the bigger picture.

This is precisely where specialized accounting software becomes invaluable. A tool like Grain Ledger, for example, is designed for the nuances of church finance. It automatically categorizes your transactions by fund, which makes it simple to pull your operational cash flow and capital spending figures. Instead of wrestling with spreadsheets, you can calculate your FCF in moments and make financial decisions that are both confident and mission-aligned.

Putting Your Financial Insights Into Action

Knowing how to read a cash flow statement is a fantastic start, but the real magic happens when you turn those numbers into action. This report isn't just a historical document to file away. Think of it as a playbook for your ministry, giving you the clarity and confidence to move your mission forward.

When you translate your church's financial story into a strategic plan, you shift from simply managing money to truly stewarding it for maximum impact. This involves building a solid rhythm of review and using the right tools to make the whole process as insightful as possible.

Set Up a Monthly Financial Review

The best way to act on what you’re learning is to get a monthly financial review meeting on the calendar. This isn't just about crunching numbers; it's about asking smart questions and making mission-focused decisions together.

The idea is to build a proactive financial culture, not a reactive one. Meeting regularly helps your team spot trends early, handle potential shortfalls before they become emergencies, and make sure every dollar is aligned with your budget and ministry goals.

So, who needs a seat at this table?

The Pastor or Senior Leader: They bring the "why"—the ministry context behind the numbers.

The Church Treasurer or Finance Admin: They bring the "what"—presenting the statements and explaining the details.

The Elder Board or Finance Committee Chair: They bring the "how"—providing oversight and strategic wisdom.

This core group can work together to analyze the cash flow statement, celebrate the ministry wins reflected in the financials, and make adjustments when needed.

Your cash flow statement is a feedback loop. It tells you what's working, what's not, and where your financial energy is truly going. A monthly review ensures you're actively listening to that feedback.

Give Your Team the Right Tools

Let's be honest: creating cash flow statements by hand, especially for a church juggling designated funds, can be a real headache. It’s slow, tedious, and easy to make mistakes.

Every hour spent fighting with spreadsheets is an hour you can't spend on ministry. This is where accounting software designed for churches really shines.

A tool like Grain Ledger is built from the ground up to handle the specific needs of fund accounting. It takes the manual labor off your plate by automatically generating accurate cash flow statements. Since it connects directly to your bank and giving platforms, every donation and expense gets categorized into the right fund without you lifting a finger.

This means when your leadership team sits down for that monthly review, they aren't second-guessing the data. They can dive right into discussing what the numbers mean for the mission. With clear dashboards and fund-specific reports, Grain Ledger helps pastors and board members—even those who aren't "numbers people"—make smart, informed decisions.

The bottom line? You spend far less time on administrative busywork and far more time focused on what actually matters: serving your people and your community. It turns financial management from a necessary evil into a powerful tool for stewardship and growth.

Common Questions About Church Cash Flow Statements

Even after breaking down the different sections of the statement, some practical questions always seem to pop up. When you're learning how to read a cash flow statement for a church, these are the details that separate theory from confident stewardship. Let's tackle a few of the most common ones I hear.

Getting clear, straightforward answers here can really demystify the process for your entire leadership team.

What’s The Difference Between A Cash Flow Statement And An Income Statement?

The big difference here comes down to timing and focus. Your income statement, which you might know as a Statement of Activities, is usually based on accrual accounting. It records income when it's pledged and expenses when they're incurred—not necessarily when the money actually moves.

This means your income statement could show a "profit" for the month, making it look like you're in a great financial position, even while your actual cash in the bank is dwindling. The cash flow statement, on the other hand, is pure reality. It tracks the actual cash coming in and going out of your accounts. It's the truest picture of your church's ability to operate right now.

Why Can Negative Cash Flow From Investing Be A Good Thing?

I know, the word "negative" always sets off alarm bells. But in the investing section, it often signals strategic growth. A negative number here simply means your church is putting its cash to work by purchasing long-term assets that will further your mission.

Think about it in these terms:

You finally bought that piece of land for a future expansion.

The children's ministry wing got a much-needed renovation.

You upgraded the worship center's ancient sound system.

These are all investments in the future. As long as these big purchases are planned and you have healthy cash flow from operations or financing to support them, a negative number here is a great sign.

A negative investing cash flow isn't a red flag; it's often a footprint of a forward-thinking ministry. It shows you're turning cash into tangible assets that will serve your congregation for years to come.

How Are Designated Gifts And Restricted Funds Handled?

This is a huge one for churches, and it’s where a lot of confusion can happen. When someone gives a designated gift—say, for the building fund—the cash coming in is typically recorded under Financing Activities.

Then, when you actually spend that money on the project (like paying the construction contractor), that cash going out is recorded under Investing Activities. Keeping these separate and tracking them properly is absolutely essential for good stewardship and transparency. This complexity is exactly why a specialized tool like Grain Ledger is so helpful; it's built to handle these fund-based transactions automatically, which keeps your reporting accurate.

How Often Should We Review The Cash Flow Statement?

For proactive financial leadership, your finance team or church board should be looking at the cash flow statement monthly. This rhythm allows you to spot trends early, see potential cash shortages before they become a crisis, and make sure your spending is actually lining up with the budget.

Now, if you're in the middle of a big capital campaign or a building project, you might even want to bump that up to a bi-weekly review. The goal is to turn this report into a living document that informs your decisions today, not just a historical record you glance at once a quarter.

Ready to stop wrestling with spreadsheets and get instant clarity on your church’s finances? Grain Ledger is true fund accounting software built for ministries. It automates your reporting, tracks every restricted dollar, and gives you the confidence to lead well.