The Definition Operating Budget A Practical Guide for Financial Planning

Jun 26, 2023

At its core, an operating budget is the financial game plan your organization lives by day in and day out. It's a detailed forecast of your expected income and all the expenses needed to keep the lights on and the mission moving forward over a set period, typically a fiscal year.

Think of it as the roadmap for your routine operations—covering everything from payroll and rent to office supplies and software subscriptions. It's the most essential tool you have for managing the daily financial pulse of your organization.

What Is an Operating Budget and Why Does It Matter?

Let's use a simple analogy. If your organization was a household, the operating budget would be your monthly plan for covering all the regular bills and spending. It’s not for huge, one-off projects like building an addition to the house—that’s what a capital budget is for. Instead, your operating budget makes sure you have enough cash for the mortgage, groceries, electricity, and all the other recurring costs that keep the household running smoothly.

This budget is, by nature, a forward-looking document. It forces you to get realistic about your anticipated revenue and then carefully map out every expense required to keep things on track. It’s the backbone of your daily financial management.

The Strategic Value of an Operating Budget

A well-built operating budget is much more than a simple accounting exercise; it’s a powerful strategic tool. It gives you a clear benchmark to measure your actual financial performance against what you planned. This comparison, often called variance analysis, is where the magic happens. It helps you quickly spot what’s going well and where you might need to course-correct.

For instance, if you see marketing expenses are running higher than budgeted but are bringing in even more revenue than projected, you know you've made a smart investment. On the flip side, if utility costs are unexpectedly soaring, it might be the trigger to look into more energy-efficient solutions. This ongoing process delivers some major benefits:

Financial Control: It’s your best defense against overspending and helps ensure your limited resources are directed toward what matters most.

Performance Measurement: It provides a clear, objective yardstick to evaluate how efficiently different departments or programs are operating.

Informed Decision-Making: It gives leaders the hard data needed to make strategic pivots, reallocate funds, and plan for sustainable growth.

To give you a clearer picture, here’s a breakdown of the typical line items you'll find in an operating budget.

Key Components of a Standard Operating Budget

Component | Description | Typical Example |

|---|---|---|

Revenue/Income | All sources of incoming funds that support daily operations. | Donations, grants, sales of goods/services, membership fees. |

Personnel Costs | Expenses related to paying your staff. | Salaries, wages, payroll taxes, health insurance, retirement contributions. |

Administrative Costs | General overhead expenses required to run the organization. | Office rent, utilities (electric, water, internet), insurance, bank fees. |

Program/Service Costs | Expenses directly tied to delivering your core services or programs. | Program supplies, event costs, marketing materials, software subscriptions. |

Contingency Fund | A small portion set aside for unexpected expenses or emergencies. | Unforeseen repairs, sudden increase in supply costs. |

This structure ensures all the moving parts of your organization's finances are accounted for, from the money coming in to every dollar going out.

A strong operating budget moves your financial plan from a reactive document to a proactive guide. It transforms financial data into an actionable roadmap, empowering leaders to steer the organization with clarity and confidence toward its long-term mission.

Ultimately, this budget gets your entire team on the same page, all working toward shared financial goals. It's not just about planning; it’s about building a resilient and adaptable organization. In fact, businesses that consistently tracked their operating budgets against actuals saw a 12% better recovery rate in profitability by 2021. You can explore more about these insights on financial resilience.

Breaking Down the Core Components of Your Budget

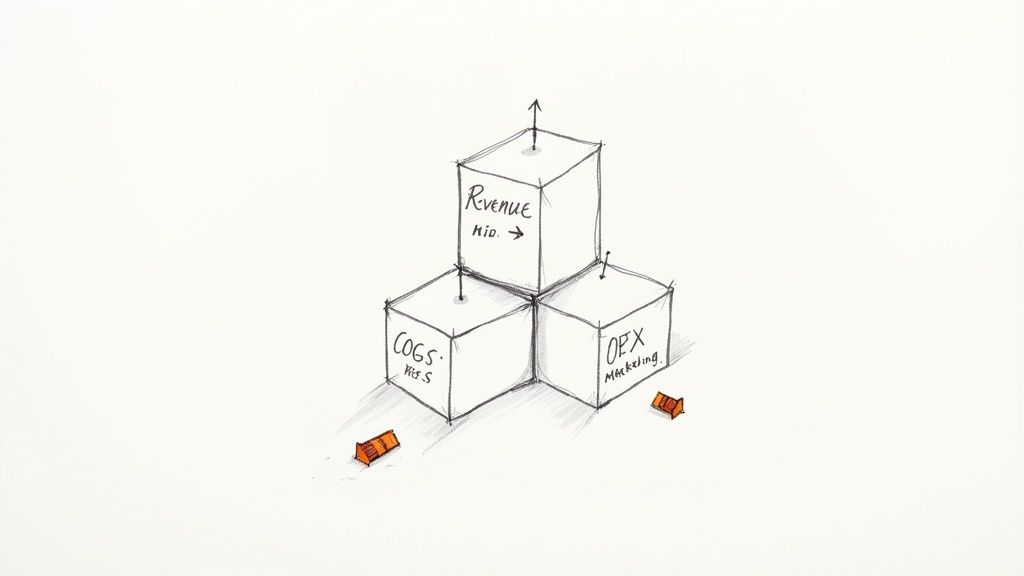

To really get what an operating budget is, you have to look under the hood at its fundamental parts. It helps to think of it as a simple formula for your organization’s financial engine: Revenue - COGS - Operating Expenses = Profit/Surplus. Each of these pieces tells a crucial part of your operational story.

Revenue is simply all the money coming in from your primary activities. For a retail shop, that’s income from selling products. For a church, it’s mostly tithes and offerings. A tech company might see revenue from software subscription fees. This is the top line of your budget—it’s the fuel for everything else.

The Cost of Doing Business

Next up is the Cost of Goods Sold (COGS). This bucket holds all the direct costs tied to making or buying the goods you sell. If you run a coffee shop, your COGS would be the price of coffee beans, milk, and cups. If your organization doesn't sell a physical product, this category might be pretty small or even non-existent.

After COGS, you have your Operating Expenses (OPEX). These are the everyday costs required to keep the doors open and the lights on, but they aren't directly tied to creating a specific product. This is where most of your day-to-day spending lives.

Operating expenses usually fall into a few key categories:

Personnel Costs: For most organizations, this is the biggest line item. It covers salaries, wages, payroll taxes, and benefits for your entire team.

Administrative Expenses: Think of these as your core "keep the lights on" costs. This includes rent or a mortgage for your building, utilities, office supplies, and insurance.

Marketing and Sales Costs: This covers everything you spend to promote your organization and bring in revenue, like advertising, website maintenance, and promotional materials.

These line items need to be tracked and categorized with care. For nonprofits and churches especially, organizing these accounts properly is absolutely critical for transparency. You can learn more about how to structure these categories in our guide to building a chart of accounts for nonprofits.

Putting the Pieces Together

It's the relationship between these components that paints the full financial picture. The numbers show an intricate web of projections. For instance, the Cost of Goods Sold can eat up 60-70% of revenues in certain industries, while operating expenses often see the largest slice go to salaries. In 2024, HR budgets within operating plans averaged $5.2 million globally for every 1,000 employees. One detailed analysis even found that organizations with precise operating budgets see 22% higher long-term value creation.

An operating budget isn't just a list of numbers; it's a dynamic model of your organization's financial life. It shows how every dollar earned is put to work, covering everything from the cost of your core mission to the salaries of the people who make it happen.

When you truly understand each piece, you can see exactly where your money is going and start making smarter decisions. Whether you're running a service business where payroll is the main event or a retail store focused on keeping COGS in check, mastering these components is the first step toward real financial control and strategic planning.

Operating Budgets vs. Capital Budgets Unpacked

One of the best ways to get a firm grip on what an operating budget really is, is to see how it stacks up against a capital budget. They’re both vital financial plans, but they play completely different roles for your organization and work on different schedules. Nailing this distinction is one of the first steps toward solid financial management.

Here's a simple way to think about it: your operating budget is for the "fuel and oil changes" that keep your organization running day in and day out. It covers all the short-term, predictable expenses like salaries, rent, utilities, and supplies.

Your capital budget, on the other hand, is for "buying a new van"—it’s a major, long-term investment that you don't make every year.

Different Purposes, Different Timelines

The real split between these two budgets comes down to their purpose and their timeline.

An operating budget is all about the here and now. It maps out your finances for a single fiscal period, which is typically one year. The whole point is to make sure you can cover the daily costs of carrying out your mission. Think of it as your guide to immediate operational health.

A capital budget has a much longer-term view, often looking out over several years. It's built specifically for buying or upgrading major assets—things that will deliver value for a long, long time. These are the big, often one-time, purchases that fall well outside of your normal operational spending.

An operating budget answers the question, "How will we fund our daily mission this year?" A capital budget answers, "How will we invest in major assets to sustain our mission for years to come?"

Keeping these budgets separate is crucial. It stops a single, massive purchase from completely skewing your view of routine financial health. For churches and nonprofits, this separation is fundamental to accountability. When a donor gives a large gift for a new building, that money needs to go into the capital budget, not get mixed in with tithes meant for ministry programs.

This is exactly where a dedicated accounting solution like Grain Ledger is so valuable. It’s built from the ground up to manage these separate funds accurately, making sure restricted donations are always used exactly as intended.

Operating Budget vs. Capital Budget at a Glance

To lay it all out as clearly as possible, here’s a simple side-by-side comparison of how these two budgets work.

Attribute | Operating Budget | Capital Budget |

|---|---|---|

Purpose | Funds daily, recurring operations. | Funds major, long-term asset purchases or projects. |

Timeframe | Covers a single fiscal year. | Spans multiple years. |

Expense Type | Routine costs like salaries, rent, supplies, utilities. | Large investments like building renovations, new vehicles, major equipment. |

Financial Impact | Expenses are recorded on the income statement as they occur. | Assets are recorded on the balance sheet and depreciated over time. |

As you can see, each budget has a distinct job to do. Your operating budget keeps the lights on, while your capital budget builds for the future.

How to Build Your Operating Budget From Scratch

Creating an operating budget for the first time can feel like you're trying to map out a dense forest with no compass. But it's really just a logical process. Think of it like assembling a puzzle: you lay out all your corner and edge pieces first—your revenue and fixed costs—before tackling the more intricate, variable pieces in the middle.

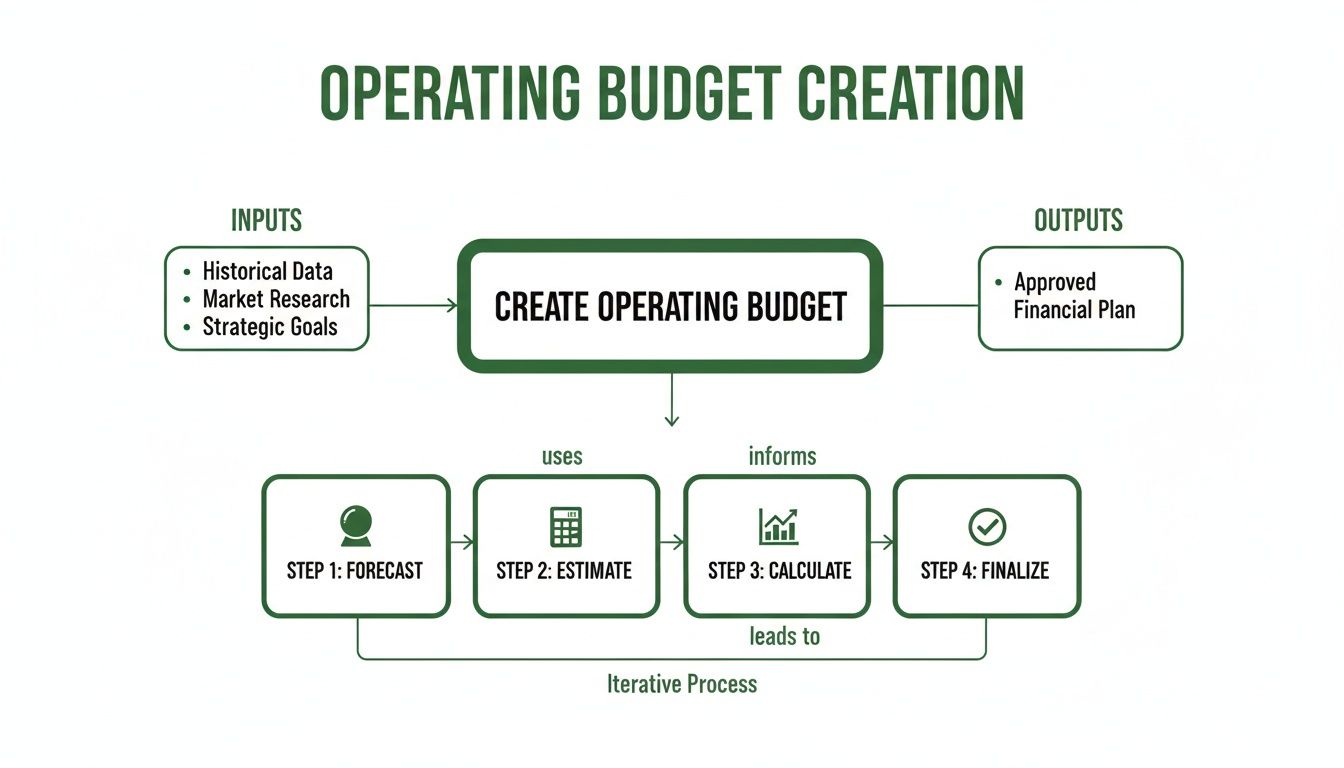

Following this framework breaks a big, daunting project into a series of smaller, more manageable steps. It boils down to four key stages: forecasting your income, estimating your expenses, seeing what's left over, and getting everyone on board with the final plan.

Step 1: Forecast Your Revenue

First things first, you need to project all the income your organization expects to bring in. This isn't just about pulling a number out of thin air; it’s about making an educated guess based on real-world data. Dig into your financial history from the last couple of years. What trends do you see? Are there seasonal patterns?

If you’re a church, for example, look at your giving trends. Is there always a big spike in donations at the end of the year? If you're running a business, what does your sales data tell you? Some months are just naturally slower than others. Answering these kinds of questions is how you build a realistic, month-by-month forecast that anticipates the natural ups and downs.

Step 2: Estimate Your Expenses

Once you have a solid idea of what's coming in, it's time to map out what's going out. I always recommend starting with your fixed expenses. These are the easy ones—the predictable costs that stay the same month after month, like rent, insurance premiums, and full-time staff salaries. They form the bedrock of your budget.

Next up, tackle your variable expenses. These are the costs that move up and down based on how busy you are. Think utility bills, program supplies, or marketing costs for a big campaign. Again, your past data is your best friend here, but you also need to build in some wiggle room. If you’re planning to launch a new community outreach program, for instance, you'll need to account for those new costs.

A classic mistake I see all the time is underestimating variable costs. A great budget doesn't just predict what you plan to spend; it also creates a buffer for what you might need to spend. It prepares you for the unexpected.

Step 3: Calculate the Difference

This step is simple math, but it’s where the rubber meets the road. Just subtract your total estimated expenses from your total forecasted revenue. What you're left with is your projected net operating income—which could be a surplus or a deficit.

Got a surplus? Fantastic! Now you get to decide how to use those extra funds. Maybe you'll beef up your contingency fund, invest in a new initiative, or just build up savings.

Facing a deficit? Okay, time for some tough decisions. You either have to find realistic ways to increase your income or identify areas where you can trim expenses without hurting your mission.

This is the moment of truth that tells you if your initial plan is financially sustainable.

Step 4: Finalize and Approve the Plan

After tweaking your numbers, it's time to lock in the budget. This is a team sport. You need to work with your department heads or ministry leaders to make sure the numbers are grounded in reality and that they're on board with the plan. Their buy-in is absolutely crucial for both accuracy and execution. Once you have a consensus, the budget should be formally approved by your board or leadership team.

Don't underestimate the impact of this process. A PwC survey found that companies that beat their operating budget targets by 5% or more also delivered 15% higher shareholder returns. This shows a direct line between a solid budget and overall success.

For nonprofits and churches, presenting this information clearly is a cornerstone of transparency and trust. To make this easier, you can use our sample nonprofit budget template to organize your final numbers in a way that’s clear, professional, and easy for everyone to understand.

Budgeting for Churches and Nonprofits

When you're handling the finances for a church or nonprofit, budgeting takes on a whole new meaning. It’s not just about balancing the books; it’s an exercise in stewardship. While the fundamental idea of an operating budget—planning for your everyday income and expenses—is the same, the mission-driven nature of your work adds a crucial layer of responsibility. The biggest shift comes down to how you handle the money coming in.

Unlike a business earning revenue, a church receives tithes and donations, and many of those gifts come with strings attached. This is where fund accounting becomes the cornerstone of your financial management. A church’s operating budget needs to draw a hard line between unrestricted funds (general tithes meant for the day-to-day mission) and restricted funds (donations given for a specific purpose, like a building fund or a mission trip).

Navigating Fund Accounting in Your Budget

Keeping these funds separate isn't just good practice; it's essential for maintaining trust and transparency with your congregation and donors. Co-mingling funds is a surprisingly common mistake, but it's a serious one that can quickly erode an organization's credibility. Your operating budget should only account for unrestricted income and the general operational costs it's intended to cover.

So, what does that look like in practice? Here are some typical line items you’d find in a church operating budget:

Income: General tithes, weekly offerings, and any other gifts given without a specific designation.

Personnel Costs: Salaries for pastors and staff, health insurance, and payroll taxes.

Facility Expenses: The mortgage or rent payment, utilities, property insurance, and routine maintenance.

Ministry Program Costs: The funds needed for the youth group, community outreach, worship services, and other core activities that fulfill your mission.

The heart of nonprofit budgeting is accountability. It’s a promise to your donors and congregation that every dollar given for the general mission is being used wisely to fund the daily work of the organization, separate from any specially designated gifts.

The chart below shows a high-level view of the process for putting together a solid operating budget.

This four-step cycle—forecasting income, estimating expenses, reviewing the numbers, and finalizing the plan—gives you a reliable framework for building a responsible budget. If you want to dive deeper into structuring these finances, take a look at these budget examples for churches to see how other ministries lay everything out.

The Right Tools for Financial Stewardship

Trying to manage fund accounting with spreadsheets or generic software can quickly become a tangled mess, opening the door to costly errors. This is exactly why specialized tools are so important for churches. An accounting solution like Grain Ledger is built to handle fund accounting intuitively, helping you track every designated gift and simplify budget management. It gives church leaders the clarity they need to ensure every dollar is stewarded with integrity.

Common Questions About Operating Budgets

As you move from theory to practice, you're bound to run into some real-world questions about your operating budget. Let's tackle a few of the most common ones that come up, so you can handle the nuances of financial planning with more confidence.

How Often Should I Review My Operating Budget?

Think of your operating budget as a living document, not a "set it and forget it" file you create once a year. To get any real value out of it, you need to check in on it regularly. The best practice is a monthly review, but a quarterly check-in should be your absolute minimum.

This regular review is where the magic happens. It’s when you compare what you actually spent and earned against what you planned to—a process called variance analysis. Honestly, it's the single best way to spot trends, catch overspending before it spirals out of control, and make smart adjustments to stay on track.

What Is the Difference Between a Static and a Flexible Budget?

This is a great question, and the answer really gets to the heart of how you measure performance. A static budget is exactly what it sounds like: it's fixed. It’s built on a single prediction of activity (like selling 1,000 widgets) and doesn't change, no matter what really happens.

A flexible budget, on the other hand, is dynamic. It adapts. If you only ended up selling 800 widgets, a flexible budget automatically adjusts your variable cost projections to match that actual level of activity. This gives you a much more accurate, apples-to-apples comparison, making it a far more powerful tool for figuring out how well you're truly managing your costs.

Can a Startup Without Past Financial Data Create a Budget?

Absolutely. It’s a common misconception that you need years of history to build a budget. While startups don't have historical data to lean on, they can still build a solid operating budget by doing their homework and making some well-reasoned assumptions. This usually involves:

Market Analysis: Digging into the industry and what competitors are doing to come up with realistic revenue goals.

Vendor Quotes: Getting actual price quotes for the big stuff—rent, software, insurance, you name it.

Industry Benchmarks: Looking up data on what's "normal" for expenses like salaries or marketing in your specific field.

For a startup, that first budget is your best guess. The key is to treat it as a draft and be ready to review and update it constantly as real financial data starts rolling in.

Why Is Net Operating Income So Important?

Net Operating Income (NOI) is one of the most important vital signs for your organization's core health. You find it right in your operating budget: just take your total operating revenue and subtract your total operating expenses.

NOI is so critical because it shows you the pure profitability of your main activities. It strips away the noise from things like interest and taxes, giving leaders an unfiltered look at how efficiently the team is managing day-to-day operations.

A healthy and growing NOI is a clear sign of operational strength and long-term sustainability. That's why it's a metric that leaders, investors, and analysts pay very close attention to.

Managing finances, especially with the complexities of fund accounting, requires a tool built for the job. Grain Ledger provides churches with a true, fund-based accounting system that simplifies budgeting, tracks every restricted dollar, and delivers the financial clarity needed for confident stewardship. Learn more at https://www.grainledger.com.