8 Practical Budget Examples for Churches in 2026

Explore 8 detailed budget examples for churches. Get actionable templates & strategic breakdowns for operational, program, and capital campaign planning.

Creating a church budget that honors God, inspires generosity, and fuels ministry can feel overwhelming. Where do you even begin? A well-structured budget is more than just numbers on a spreadsheet; it is a theological document that outlines your ministry's priorities and vision. It serves as a fundamental tool for stewardship, transparency, and strategic planning, ensuring every dollar is aligned with your mission.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Get Your Personalized Template

Enter your church's budget, attendance, and payroll to generate a custom Excel template with industry-standard percentages and formulas.

This guide moves beyond theory to provide tangible, practical help. To assist you in this critical task, we have compiled a comprehensive list of eight distinct budget examples for churches. This collection is designed for church treasurers, pastors, finance committees, and administrators who need clear, actionable frameworks for financial management. We will explore a variety of models suitable for different contexts and needs.

Inside, you will find detailed breakdowns and templates for:

- The Percentage-Based Allocation Model

- Zero-Based Budgeting (ZBB) for Churches

- The Stewardship/Tithing-Based Budget Model

- The Ministry-Based Functional Budget

- The Multi-Year Capital Planning Budget

- The Activity-Based Costing (ABC) Budget Model

- The Flexible/Rolling Budget Template

- The Donor-Restricted and Unrestricted Fund Budget Model

Each example includes line-item analysis, strategic insights, and practical steps you can implement immediately. From simple percentage-based models ideal for smaller congregations to sophisticated fund accounting frameworks for growing ministries, these examples provide the tools you need to build a budget that truly serves your mission. Let's explore the models that can bring financial clarity and confidence to your leadership.

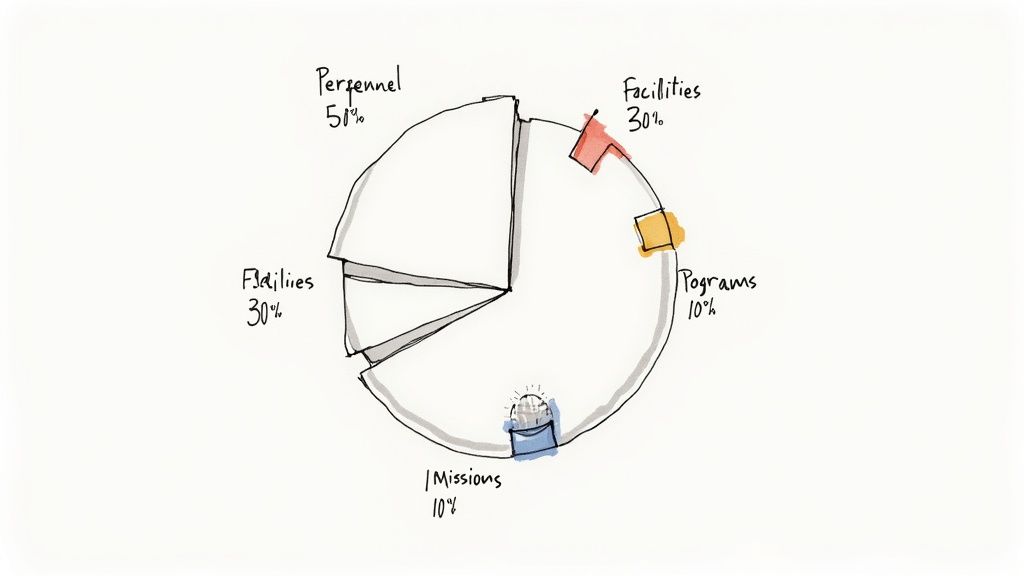

1. The Percentage-Based Allocation Model

The Percentage-Based Allocation Model is a foundational and highly popular approach among churches for structuring their annual budget. Instead of building a budget from zero-based line items, this method allocates total anticipated revenue into broad categories based on predetermined percentages. It provides a simple, high-level framework that aligns spending with the church's core priorities, making it an excellent starting point for many congregations.

This model, often championed by organizations like the Christian Leadership Alliance and leaders like Rick Warren, offers a clear snapshot of financial strategy. It ensures that essential areas like staffing and facilities are adequately funded while dedicating specific portions to ministry and outreach, reflecting a balanced approach to stewardship.

Strategic Breakdown and Typical Allocations

The strength of this model lies in its simplicity and strategic clarity. The typical percentage breakdown provides a tested guideline that can be adapted to a church's specific context.

- Personnel (45-55%): This is the largest category, covering salaries, benefits, and payroll taxes for all staff. A healthy church invests in its people, and this allocation ensures the team is well-supported to carry out the ministry's vision.

- Facilities & Operations (25-35%): This includes mortgage or rent, utilities, insurance, maintenance, and administrative costs. It covers the essential expenses required to keep the church doors open and operating smoothly.

- Ministry Programs (10-15%): This bucket funds the core activities of the church, such as children's and youth ministry, small groups, worship services, and discipleship resources.

- Missions & Outreach (5-15%): This allocation is dedicated to local and global missions, evangelism efforts, and community service projects, ensuring the church remains outwardly focused.

Key Insight: This budgeting method forces a conversation about priorities. If your missions allocation is only 5%, the budget transparently reflects that decision. Adjusting the percentages becomes a powerful tool for shifting the church's strategic focus over time.

Actionable Takeaways for Implementation

To effectively use this model, consider the following tactical steps:

- Establish Your Baseline: Analyze your last two years of spending to determine your church's current, de facto percentages. This provides a realistic starting point for discussion.

- Incorporate a Contingency: Within your operations or a separate category, set aside 3-5% as a contingency fund. This prevents unexpected facility repairs or shortfalls from derailing ministry program budgets.

- Review and Adjust Annually: Percentages should not be static. Before each budget cycle, leadership should review these allocations to ensure they align with the upcoming year's vision and strategic initiatives.

- Communicate Clearly: Share the high-level percentage breakdown with the congregation. This transparency builds trust and helps members understand how their tithes and offerings are stewarding the church's mission.

2. Zero-Based Budgeting (ZBB) for Churches

Zero-Based Budgeting (ZBB) is a meticulous and highly intentional methodology where every expense must be justified for each new budget period. Unlike traditional budgeting that adjusts the previous year's numbers, ZBB starts from a "zero base," forcing every ministry department to build its budget from the ground up and defend the necessity of every dollar requested.

This rigorous approach promotes exceptional stewardship and eliminates legacy spending that may no longer align with the church's current vision. Championed by management thinkers and adopted by accountability-focused organizations like the ECFA, ZBB ensures that all financial resources are actively and strategically allocated to the most impactful ministry efforts for the coming year.

Strategic Breakdown and Typical Allocations

The power of ZBB lies in its detailed justification process rather than fixed percentages. Each ministry area must present a compelling case for its proposed expenses, connecting them directly to strategic goals.

- Ministry Justification Packets: Each department (e.g., Children's Ministry, Outreach, Worship Arts) submits a detailed proposal. This packet outlines their goals for the year and the specific line-item expenses required to achieve them, such as curriculum costs, event supplies, or volunteer appreciation.

- Ranking and Prioritization: Leadership reviews all requests and ranks them based on alignment with the church's overall mission, potential impact, and resource availability. A youth retreat might be ranked higher than new lobby furniture if the church's priority is discipleship.

- Resource Allocation: Funds are allocated to the highest-ranked initiatives until the anticipated revenue is fully budgeted. This forces difficult but necessary conversations about what is truly essential versus what is merely "nice to have."

- Scrutiny and Accountability: This process inherently scrutinizes every subscription, contract, and program, preventing budgetary bloat and ensuring funds are used efficiently.

Key Insight: ZBB shifts the conversation from "What did we spend last year?" to "What is the most effective way to use God's resources to achieve our mission this year?" It transforms the budget from a static financial document into an active ministry plan.

Actionable Takeaways for Implementation

Adopting ZBB requires a significant commitment but yields powerful results. Consider these tactical steps:

- Pilot in One Department: Instead of a full, church-wide rollout, test the ZBB process with one or two ministry areas first. This helps refine your process and demonstrates its value on a smaller scale.

- Establish Clear Criteria: Provide all ministry leaders with a clear rubric for what constitutes a strong justification. Criteria should include alignment with church vision, expected ROI (Return on Investment, in terms of ministry impact), and detailed cost breakdowns.

- Schedule Ample Time: The ZBB process is more time-intensive than traditional budgeting. Begin the process at least 3-4 months before the start of your new fiscal year to allow for thorough review and discussion.

- Document All Decisions: Maintain a clear record of why certain requests were approved and others were denied. This transparency is crucial for maintaining trust with ministry leaders and the congregation. To build a robust framework, consider exploring a sample nonprofit budget template that aligns with ZBB principles.

3. The Stewardship/Tithing-Based Budget Model

The Stewardship/Tithing-Based Budget Model is a biblically grounded approach that frames financial planning as an act of worship and spiritual responsibility. Instead of viewing the budget as a simple spreadsheet of income and expenses, this model begins with the theological conviction that all resources belong to God. It builds the budget conservatively based on historical tithes and offerings, emphasizing faithful management over aggressive financial forecasting.

This approach, popularized by organizations like Crown Financial Ministries and Dave Ramsey's Financial Peace University, shifts the focus from "what can we afford" to "how can we best steward what God has provided." It integrates faith-based financial teaching with prudent management, creating a culture where giving is celebrated as a core part of discipleship. It is one of the most common budget examples for churches rooted in evangelical traditions.

Strategic Breakdown and Typical Allocations

The strength of this model lies in its ability to connect financial decisions directly to spiritual principles. The budget becomes a testament to the church's faith and trust in God's provision, rather than just a financial tool.

- Conservative Income Projections: Income is typically projected based on the previous year's actual giving, often with a slight, conservative increase of 1-3%. This prevents the church from overspending based on optimistic but unrealized growth.

- Emphasis on Tithing: A core component is teaching the biblical principle of the tithe (giving 10%). The church budget itself often models this by allocating the first 10% of its income to missions and outreach before any other expenses are paid.

- Debt Avoidance: This model strongly discourages debt, aligning with teachings on financial freedom. Capital projects are funded through savings and specific giving campaigns rather than loans.

- Generosity as a Priority: After missions, ministry programs are funded, followed by operational and personnel costs. This order intentionally prioritizes the outward-focused work of the church.

Key Insight: This model transforms the budget from an administrative task into a discipleship tool. When the congregation sees the church tithing its own income to missions first, it powerfully reinforces the very stewardship principles being taught from the pulpit.

Actionable Takeaways for Implementation

To effectively use this model, consider the following tactical steps:

- Establish Giving Baselines: Analyze giving data from the last 3-5 years to create a realistic and conservative income projection. Avoid basing the budget on aspirational giving goals.

- Build an Emergency Reserve: A crucial element of good stewardship is preparation. Systematically build an operating reserve of 6-12 months of expenses to ensure stability during leaner giving seasons.

- Teach Stewardship Regularly: Don't limit financial teaching to an annual sermon. Integrate principles of stewardship, tithing, and generosity into small groups, new member classes, and regular worship services.

- Share Giving Testimonies: Create opportunities for members to share stories of how giving has impacted their faith. This personalizes the act of stewardship and encourages others far more effectively than simple reminders to give.

4. The Ministry-Based Functional Budget

The Ministry-Based Functional Budget organizes finances around specific ministry functions rather than traditional line-item expense categories. This structure shifts the focus from "what are we spending on?" to "what are we funding?" by allocating resources directly to areas like children's ministry, worship, youth group, and missions. It provides unparalleled clarity on the true cost and resource allocation for each arm of the church's spiritual mission.

This approach is championed by church management software providers like Ministry Brands and consultants from organizations like Leadership Network. It's designed to align financial reporting directly with strategic ministry outcomes, making it a powerful tool for leaders who want to measure the impact of their spending.

Strategic Breakdown and Typical Allocations

The power of this model is its ability to create "mini-budgets" for each ministry department, fostering ownership and accountability among ministry leaders. This is one of the most effective budget examples for churches looking to empower their teams.

- Worship Ministry: Includes salaries for worship staff, volunteer appreciation, AVL (audio/visual/lighting) equipment maintenance and upgrades, music licensing fees, and special event production costs.

- Children's & Youth Ministry: Covers curriculum purchases, background checks, volunteer supplies, event expenses (like VBS or youth camp), and age-specific equipment.

- Missions & Outreach: Funds support for missionaries, local outreach partnerships, evangelism event costs, and community service project supplies.

- Administration & Operations: This functional category acts as an internal service provider, encompassing costs that support all other ministries, such as facility expenses, general office supplies, insurance, and administrative staff salaries. A key step is allocating a portion of these costs back to the ministries they serve.

Key Insight: This method transforms budget conversations from being about cutting costs to investing in effectiveness. When the youth pastor can show that their $20,000 budget led to 50 new students and 10 baptisms, the discussion shifts to strategic ROI, not just expenses.

Actionable Takeaways for Implementation

To implement a functional budget effectively, your church needs clear processes:

- Define Each Ministry Area: Create a "charter" for each ministry budget that clearly defines what expenses belong to it. This prevents confusion and budget overlap between departments.

- Allocate Shared Costs: Develop a consistent method for allocating shared operational costs (like utilities or facility usage) to the ministry areas. This could be based on square footage used, headcount, or percentage of the total budget.

- Empower Ministry Leaders: Give department heads direct ownership of their budgets. Hold monthly review meetings with them to track spending against goals and make adjustments as needed.

- Connect Budget to Metrics: For each ministry budget, identify 1-2 key performance indicators (KPIs) to track, such as attendance, new visitors, or small group participation. This links financial stewardship directly to ministry fruitfulness.

5. The Multi-Year Capital Planning Budget

The Multi-Year Capital Planning Budget is a long-term financial strategy that forecasts major expenditures beyond the typical 12-month operating cycle. Instead of reacting to facility failures or growth opportunities as they arise, this model proactively plans for significant investments over a three- to five-year horizon. It addresses major facility improvements, large equipment replacements, and strategic campus expansions.

This forward-looking approach is a hallmark of strong financial stewardship, championed by organizations like the Evangelical Council for Financial Accountability (ECFA) and various church facility consultants. It enables churches to anticipate and save for big-ticket items, manage debt responsibly, and execute long-term vision without derailing day-to-day ministry operations.

Strategic Breakdown and Typical Allocations

The power of this model is its ability to separate long-term, large-scale projects from the annual operational budget, providing clarity and stability. It involves forecasting needs and setting aside funds systematically.

- Capital Reserve/Replacement Fund: This is a designated fund for the eventual replacement of high-cost assets like HVAC systems, roofing, or major audiovisual equipment. Churches often allocate 1-3% of their annual budget or a fixed amount based on a facility audit.

- Expansion or Renovation Projects: This category outlines phased funding for future growth, such as a new children's wing, sanctuary renovation, or parking lot expansion. The plan details project costs, timelines, and funding sources (e.g., capital campaign, designated giving, loans).

- Debt Reduction: For churches carrying a mortgage or other loans, the capital plan includes a strategic schedule for accelerated debt repayment, freeing up future cash flow for ministry.

- Major Technology Upgrades: This covers significant investments in church management software, network infrastructure, or production gear that fall outside the scope of the annual operating budget.

Key Insight: A multi-year capital plan transforms the conversation from "Can we afford this emergency repair?" to "How are we strategically investing in the long-term future of our ministry?" It aligns facilities and major assets directly with the church's discipleship and outreach mission.

Actionable Takeaways for Implementation

To effectively build and use this strategic budget, consider these steps:

- Conduct a Facility Audit: Hire a professional or use a skilled volunteer team to assess the condition and expected lifespan of your building's key components. This audit forms the data-driven foundation for your replacement fund projections.

- Establish a Designated Fund: Formally create a board-restricted capital reserve fund. Consistently allocate money to this fund from the general budget or through designated giving to build up reserves over time.

- Develop Scenario Plans: Create conservative, moderate, and optimistic growth scenarios for your 3-5 year plan. This allows you to adjust your capital projects based on actual giving and attendance trends.

- Communicate the Vision, Not Just the Cost: When presenting the plan, focus on how these capital investments will facilitate ministry. Frame a new roof as "protecting our space for worship and community" and a building expansion as "making room for more families to hear the gospel."

6. The Activity-Based Costing (ABC) Budget Model

The Activity-Based Costing (ABC) Budget Model is an advanced and granular approach that provides unparalleled clarity on the true cost of each ministry activity. Instead of allocating overhead costs using broad percentages, ABC traces expenses directly to the specific programs and services that consume them, such as a youth retreat or a community food drive. This method reveals exactly what resources, from staff time to facility usage, each activity requires.

Pioneered in the corporate world and championed by management accounting experts and CPA firms serving non-profits, this model offers a sophisticated view of financial stewardship. For large churches or complex organizations, it moves beyond general fund allocation to answer the question: "What is the real cost and financial impact of this specific ministry?"

Strategic Breakdown and Typical Allocations

The power of the ABC model is in its precision. It connects indirect costs (like administration salaries and utilities) to direct activities based on actual consumption, providing a far more accurate financial picture.

- Cost Pools: First, indirect costs are grouped into logical categories, such as "Facility Maintenance," "Administrative Support," or "IT Services."

- Cost Drivers: Next, a "driver" is identified for each pool, a unit of activity that causes the cost. For facilities, this might be square footage used or hours of occupation. For administrative support, it could be the number of transactions processed or staff hours dedicated to a program.

- Activity Allocation: Costs are then allocated to specific ministry programs based on their usage of these drivers. For example, the annual youth camp would be assigned a portion of the facility and administrative costs based on how many hours it used the building and how much staff time it required.

- True Program Cost: The final result is the total direct cost of the program plus its accurately allocated share of indirect overhead, revealing its true cost to the church.

Key Insight: This model transforms financial conversations. Instead of saying "the youth budget is $20,000," leadership can say, "our summer camp costs a total of $15,000 to run when accounting for staff time and facility use, serving 50 students at a true cost of $300 per student."

Actionable Takeaways for Implementation

Implementing ABC requires a strategic and focused approach. It is best suited for larger churches or for analyzing specific, high-impact programs.

- Start Small: Do not attempt a church-wide ABC rollout at once. Select two or three key ministry programs to analyze first, such as a large annual conference or the VBS program.

- Track Staff Time: Staff salaries are often the largest indirect cost. Use simple time-tracking tools or spreadsheets for a set period (e.g., one month) to understand how much time staff members dedicate to various ministry activities.

- Define Cost Drivers Clearly: Work with ministry leaders to identify logical and easy-to-measure drivers for your main cost pools. Keep it simple to ensure the system is sustainable.

- Use Data for Strategy, Not Punishment: The goal of ABC is to inform strategic decisions about resource allocation, not to penalize ministries that appear "expensive." Use the data to identify opportunities for efficiency, collaboration, or strategic investment.

7. The Flexible/Rolling Budget Template

The Flexible/Rolling Budget Template is an adaptive, dynamic approach that moves away from the traditional static annual budget. Instead of setting a rigid plan for 12 months, a rolling budget continuously forecasts for a set period, like the next 12 months, and is updated monthly or quarterly. This model is ideal for churches experiencing unpredictable income, rapid growth, or economic uncertainty, allowing for real-time adjustments.

This modern financial management method allows a church to be more agile and responsive. For example, a new church plant seeing faster-than-expected growth can adjust its budget quarterly to hire staff or expand ministries, rather than waiting for the next annual cycle. It provides a more accurate and relevant financial picture at any given point in the year.

Strategic Breakdown and Typical Allocations

The core strength of a rolling budget is its responsiveness, not a fixed percentage allocation. The strategy lies in its structure and the process for updating it, which empowers leadership to make informed, timely decisions.

- Continuous Forecasting: The budget always looks ahead a full 12 months. At the end of Q1, a new forecast for Q1 of the following year is added. This prevents the "end-of-year" spending rush or paralysis.

- Variable Expense Management: Expenses are tied directly to actual income. If giving exceeds projections for two consecutive months, the budget for outreach or children's ministry might be increased in the next forecast. Conversely, a dip in giving triggers a planned, non-panicked spending reduction.

- Mission-Critical Protection: Core expenses like salaries and essential facility costs are designated as "protected," ensuring they are the last to be cut during a downturn. Discretionary spending in areas like events or new equipment is the first to be adjusted.

- Regular Review Cadence: The finance team or leadership board meets monthly or quarterly to review performance against the forecast and make necessary adjustments for the upcoming periods.

Key Insight: A rolling budget transforms the budget from a static historical document into a living, strategic tool. It forces leaders to constantly evaluate financial realities and align spending with current ministry opportunities and challenges, rather than a plan made ten months prior.

Actionable Takeaways for Implementation

To effectively use this model, consider the following tactical steps:

- Establish Clear Triggers: Define what conditions will trigger a budget review and potential adjustment. For instance, a +/- 10% variance in monthly income from the forecast could be a standard trigger.

- Maintain a Strong Reserve: This model requires a safety net. Aim to maintain a minimum of three months' operating expenses in a reserve fund to provide stability during periods of lower-than-expected income.

- Use Appropriate Tools: A rolling budget is difficult to manage on paper. Implementing a robust system, such as a well-designed church budget template for Excel, is crucial for managing the continuous updates.

- Document and Communicate: Every adjustment to the rolling forecast must be documented and approved by leadership. Transparent communication with ministry leaders about changes is essential to maintain alignment and trust.

8. The Donor-Restricted and Unrestricted Fund Budget Model

The Donor-Restricted and Unrestricted Fund Budget Model is a sophisticated approach essential for churches managing designated giving. It moves beyond a single operational budget by separating funds based on donor intent. Unrestricted funds are available for general operating expenses, while restricted funds are legally bound to be used for specific purposes designated by the donor, such as a building campaign, missions trip, or benevolence ministry.

This method, strongly advocated by accountability groups like the ECFA, ensures legal and ethical compliance while providing unparalleled financial transparency. It forces a church to honor the specific intentions of its givers, building trust and often encouraging more significant, targeted donations. This is one of the most critical budget examples for churches that want to maintain donor confidence and financial integrity.

Strategic Breakdown and Typical Allocations

The strength of this model is its clarity and integrity. Instead of percentages, it segregates income and expenses into distinct, non-interchangeable funds, reflecting the church's various financial commitments.

- Unrestricted Fund (General Fund): This is the church's main operational account. It includes all tithes and offerings not designated for a specific purpose and covers day-to-day expenses like staff salaries, facility costs, and general ministry programs.

- Temporarily Restricted Funds: These are funds donated for a specific purpose that will be fulfilled in the future. Examples include a youth camp fund, a specific missions project, or a capital campaign for a new building. Once the condition is met (the camp happens or the building is complete), the funds are released from restriction.

- Permanently Restricted Funds (Endowments): This is money or property donated with the stipulation that the principal must remain intact permanently. The church can typically only spend the investment income generated from the principal, often for a specified purpose like scholarships or facility maintenance.

Key Insight: This model isn't just an accounting practice; it's a donor relations strategy. By clearly tracking and reporting on restricted funds, you demonstrate faithful stewardship of every designated dollar, which can inspire greater confidence and generosity from major donors.

Actionable Takeaways for Implementation

To effectively use this model, consider the following tactical steps:

- Use Fund Accounting Software: Standard business software is insufficient. Use systems like Aplos or QuickBooks Online Plus that are designed for fund accounting to properly track separate fund balances.

- Establish a Gift Acceptance Policy: Create a clear, written policy that defines what types of restricted gifts the church can accept and under what conditions. This prevents accepting gifts with restrictions the church cannot realistically fulfill.

- Produce Regular Fund Reports: Provide the finance committee and board with quarterly reports detailing the balance, income, and expenses for each major restricted fund. This maintains high-level oversight and accountability.

- Train Staff on Proper Coding: Ensure anyone handling finances is trained to correctly code income and expenses to the appropriate fund. A single miscategorized donation can lead to compliance issues and reporting errors. For a deeper understanding of expense allocation, churches can learn more about the statement of functional expenses for nonprofits.

8 Church Budget Models Compared

| Model | 🔄 Implementation complexity | ⚡ Resource requirements | 📊 Expected outcomes | 💡 Ideal use cases | ⭐ Key advantages |

|---|---|---|---|---|---|

| The Percentage-Based Allocation Model | Low — straightforward percentages and rules | Low — basic accounting, minimal training | Stable priority funding; predictable allocations | Small–medium churches seeking simplicity | Transparent, easy to communicate, adaptable |

| Zero-Based Budgeting (ZBB) for Churches | Very high — requires full justification each cycle | Very high — staff time, training, review processes | Eliminates redundant spend; strong strategic alignment | Large churches with admin capacity or undergoing review | Forces discipline; exposes waste; aligns budget to goals |

| The Stewardship/Tithing-Based Budget Model | Moderate — depends on giving forecasts and teaching | Moderate — giving tracking and stewardship programs | Strengthened stewardship culture; revenue-sensitive | Congregations emphasizing theology and generosity | Aligns finances with spiritual values; builds donor discipleship |

| The Ministry-Based Functional Budget | High — overhead allocation and outcome metrics | High — tracking systems, staff training | Clear ministry cost visibility; improved allocation decisions | Multi-ministry or multi-site churches wanting ROI views | Shows true ministry costs; supports strategic planning |

| The Multi-Year Capital Planning Budget | High — rolling forecasts and board oversight | Moderate–High — financial forecasting, consultants | Better project readiness; fewer facility crises | Churches planning expansions, renovations, major projects | Enables phased funding and responsible debt planning |

| The Activity-Based Costing (ABC) Budget Model | Very high — detailed activity-level tracking | Very high — software, time-tracking, analytics | Precise cost-per-program; data-driven resource shifts | Large organizations, mega-churches, universities | Reveals hidden costs; enables fair program comparisons |

| The Flexible/Rolling Budget Template | Moderate — requires regular revisions and discipline | Moderate — frequent reviews, forecasting tools | Highly responsive to revenue changes; fewer shocks | Growing churches, startups, economically volatile areas | Adaptive forecasting; accommodates seasonal giving |

| Donor-Restricted & Unrestricted Fund Budget Model | High — dual-fund accounting and compliance | High — fund accounting software, reporting controls | Enhanced donor trust; targeted giving but restricted use | Churches with endowments or major donor programs | Honors donor intent; improves transparency and stewardship |

Choosing Your Best Path to Financial Faithfulness

The journey through these diverse budget examples for churches reveals a foundational truth: your church’s budget is far more than a spreadsheet of numbers. It is a theological document, a strategic roadmap, and a powerful tool for stewardship that reflects your core values and ministry priorities. Moving beyond a simple income-versus-expense report to a dynamic, mission-focused financial plan is the key to unlocking greater impact and fostering a culture of generosity and trust.

We explored a spectrum of models, from the straightforward Percentage-Based Allocation to the highly detailed Activity-Based Costing. Each serves a unique purpose and is tailored to different church sizes, complexities, and missional goals. The choice is not about finding a perfect, one-size-fits-all template but about selecting and adapting the framework that best empowers your specific vision.

Key Insights and Strategic Takeaways

As you reflect on the models presented, remember these critical takeaways:

- Clarity Precedes Control: The most effective budgets begin with a clear understanding of your mission. Models like the Zero-Based Budget and the Ministry-Based Functional Budget force you to ask "why" behind every dollar spent, ensuring that resources are directly tied to missional outcomes.

- Flexibility Builds Resilience: A static, annual budget can quickly become obsolete in a dynamic ministry environment. Embracing a Flexible/Rolling Budget allows you to adapt to changing attendance, giving patterns, and unforeseen opportunities, making your church more agile and responsive.

- Transparency Inspires Trust: Donors are partners in ministry, and transparent financial practices honor that partnership. The Donor-Restricted and Unrestricted Fund Budget Model is essential for demonstrating accountability, particularly when managing designated gifts, building funds, or capital campaigns. It proves you are stewarding their specific contributions faithfully.

Strategic Point: The ultimate goal of any church budget is to align every financial decision with the Great Commission. Your chosen model should not just track funds; it should actively propel your ministry forward, empowering leaders and equipping the saints for the work of service.

Your Actionable Next Steps

Feeling equipped is different from taking action. To translate these concepts into tangible progress for your church, consider these immediate steps:

- Assemble a Diverse Budget Team: Move beyond just the treasurer or a single elder. Involve a ministry leader, a long-time member, and perhaps a new member to bring varied perspectives to the table. This collaborative approach builds buy-in and produces a more holistic plan.

- Conduct a Financial Self-Audit: Before adopting a new model, review your past year's financials. Where did you overspend? Where did you underspend? What does this spending say about your actual priorities versus your stated ones?

- Pilot a New Model: You don't need to overhaul your entire system overnight. Select one ministry department, like youth or outreach, and apply a new model (like Zero-Based Budgeting) to its specific budget for one quarter. This pilot program can reveal the benefits and challenges before a church-wide implementation.

- Prioritize Fund Accounting: Regardless of the model you choose, committing to true fund accounting is non-negotiable for long-term financial health and integrity. This practice ensures restricted donations are handled with impeccable care, protecting your church legally and ethically.

Mastering these budgeting concepts elevates your church’s financial stewardship from a necessary administrative task to a vital act of worship. A well-crafted budget frees your pastor to focus on pastoral care, empowers your ministry leaders to dream bigger, and gives your congregation confidence that their offerings are making an eternal impact. By thoughtfully selecting and implementing the right framework, you build a sustainable foundation that honors God and supports the flourishing of His church for years to come.

Ready to transform your financial stewardship with a tool built for the unique needs of churches? Grain provides true fund accounting, making it simple to manage restricted donations, create ministry-based budgets, and generate transparent reports. Explore how Grain can bring clarity and confidence to your financial management.

Ready to simplify your church finances?

Schedule a demo to see Grain Ledger in action, or sign up for product updates.