treasurer duties non profit: A Guide to Nonprofit Finances

Discover treasurer duties non profit, including financial oversight, reporting, and governance tips to keep your nonprofit compliant and thriving.

More than just a bookkeeper, a nonprofit treasurer is the financial guardian of the organization's mission. They stand at the helm, ensuring every dollar is accounted for and put to work effectively, which is essential for building trust with donors and the community you serve.

Their job is to oversee the financial assets, make sure the board gets timely and accurate reports, and keep the organization in good standing with all legal requirements.

The Financial Navigator of Your Nonprofit

Think of your treasurer as the navigator on a ship. The captain—your Executive Director or CEO—sets the destination. But it's the navigator who charts the course, watches the weather, and makes sure the ship has enough fuel and supplies to get there safely. This is the heart of the treasurer duties non profit organizations depend on to survive and grow.

A great treasurer does more than just count the money; they tell the organization's story through its finances. They translate the mission into a financial reality, looking beyond simple transactions to see the long-term impact of today's decisions.

To give you a clearer picture, here's a quick breakdown of their key responsibilities.

Nonprofit Treasurer Responsibilities at a Glance

| Responsibility Area | Core Functions |

|---|---|

| Financial Stewardship & Management | Safeguard assets, manage bank accounts, oversee cash flow, and implement internal controls. |

| Budgeting & Strategic Planning | Lead the annual budget process, monitor performance against the budget, and provide financial insights for strategic decisions. |

| Financial Reporting | Prepare and present clear financial statements (e.g., Statement of Financial Position, Statement of Activities) to the board and other stakeholders. |

| Compliance & Legal Duties | Ensure timely filing of government forms (like the IRS Form 990), manage payroll taxes, and maintain records for audit purposes. |

This table provides a high-level view, but each area involves a detailed set of tasks that are crucial for the organization's health and integrity.

The 4 Pillars of a Treasurer's Role

The treasurer’s responsibilities really come down to four fundamental pillars. Getting these right is the foundation of effective financial leadership.

- Financial Stewardship: This is all about protecting the organization's assets. It means creating smart policies, strong internal controls, and managing risk. You're the guardian of the resources entrusted to you by your community.

- Accurate Reporting: It's the treasurer’s job to prepare, present, and clearly explain financial reports to the board. This gives leadership the clear view they need to make good, informed decisions.

- Strategic Oversight: This involves more than just numbers; it's about insight. The treasurer is a key player in the budgeting process, analyzes financial trends, and helps answer the big questions like, "Can we really afford to launch this new program?"

- Legal and Tax Compliance: This is non-negotiable. The treasurer makes sure all required financial filings, especially the annual IRS Form 990, are done right and on time to protect the organization's tax-exempt status.

A great treasurer doesn't just manage the books; they champion the mission with financial integrity. They build confidence among donors, empower the board with clarity, and ensure the organization has the stability to make a lasting impact.

It's More Than Just Crunching Numbers

Ultimately, being a treasurer is a true leadership position. They often chair the finance committee and work hand-in-hand with senior staff to make sure the financial strategy lines up with the mission's goals.

By moving beyond simple bookkeeping, treasurers become invaluable strategic partners. They connect the dots between financial health and mission success, ensuring the organization isn't just surviving—it's thriving. This proactive, big-picture approach is exactly what a board should expect when defining the treasurer duties non profit success depends on.

Your Fiduciary and Legal Responsibilities as Treasurer

Beyond just balancing the books and crunching numbers, your most critical role as a nonprofit treasurer is your fiduciary responsibility. This isn't just corporate jargon; it's a profound legal and ethical promise to always act in the best interests of the organization.

Think of it as a sacred trust. Donors, your community, and the very people you serve have placed their confidence in you to protect the organization's resources and steer them toward the mission.

This duty is the foundation of everything you do. Getting it wrong, even by accident, can open up a Pandora's box of legal and financial trouble for both you and the organization. But when you get it right, every decision you make reinforces the integrity and transparency that great nonprofits are built on.

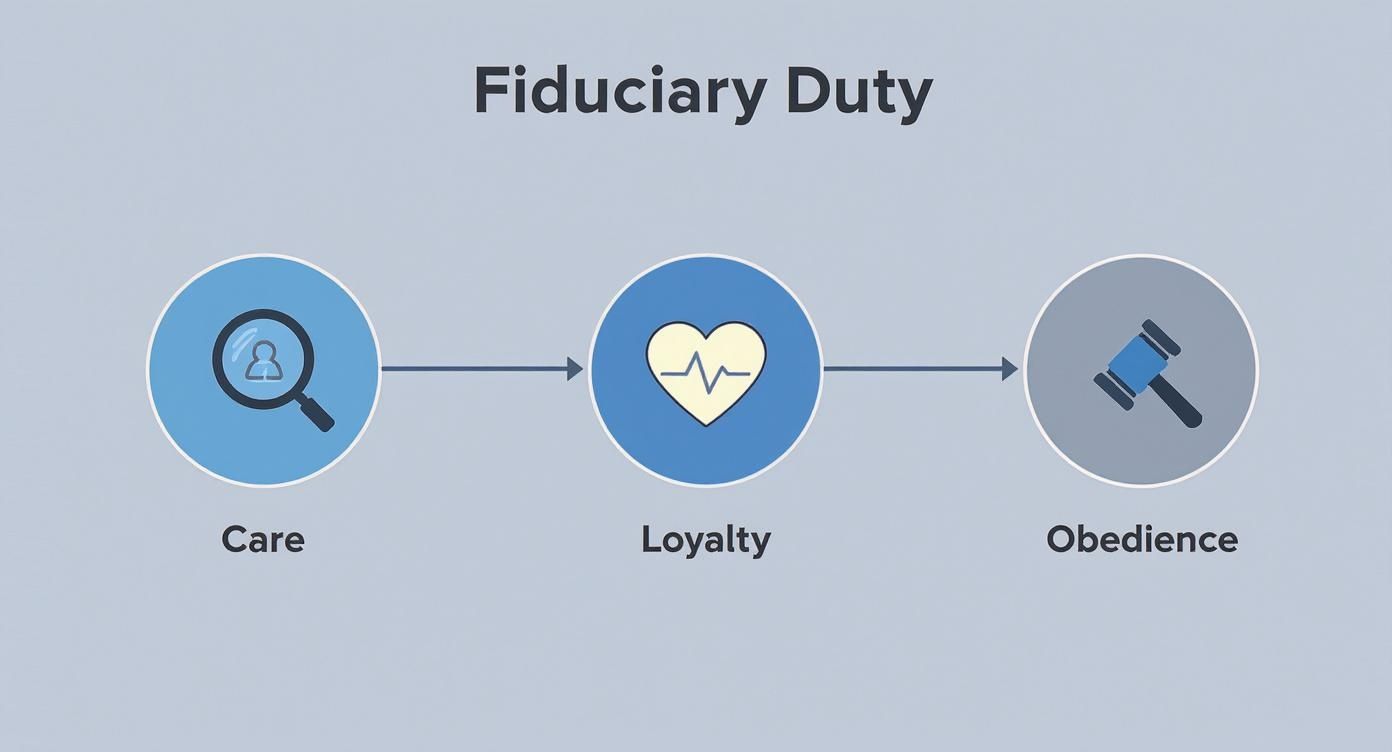

This core responsibility is best understood through three distinct, yet deeply connected, duties.

The Three Pillars of Fiduciary Duty

Grasping these three pillars gives you a practical roadmap for making sound financial decisions. They aren’t abstract legal ideas; they’re the guardrails that keep your financial leadership true.

The Duty of Care: This one is simple: pay attention. You're expected to show up informed, ask tough questions, and actively participate in financial discussions. It’s all about doing your homework. You don't have to be a CPA, but you do need to understand the financial reports in front of you and have the courage to speak up when something doesn't make sense. A perfect example is digging into the details of the annual budget before you vote to approve it, not just rubber-stamping it.

The Duty of Loyalty: This pillar is about putting the nonprofit first, always. Your personal interests—and those of your family or business—must take a backseat to the organization's well-being. This means being vigilant about avoiding any conflicts of interest. For example, if your brother-in-law's company submits a bid for the annual fundraiser, you must disclose that relationship and step away from any vote on the matter. Your loyalty belongs to the mission, period.

The Duty of Obedience: This duty is about staying true to the mission and following the rules. It means making sure the nonprofit complies with all laws, follows its own bylaws, and honors the specific intentions of its donors. If a family gives a large gift specifically for the new youth center, the Duty of Obedience means you can't "borrow" from that fund to patch a hole in the general operating budget.

"A fiduciary is someone who has undertaken to act for and on behalf of another in a particular matter in circumstances which give rise to a relationship of trust and confidence."

In the nonprofit world, that trust is everything. Your number one job is to protect it.

Staying on the Right Side of the Law

A huge part of your fiduciary duty is making sure the organization keeps up with its legal and tax filings. This is absolutely non-negotiable. It’s how you maintain public trust and, crucially, your nonprofit’s tax-exempt status.

Dropping the ball here can bring on serious penalties from the IRS and even threaten the organization's ability to operate. Your role is central to keeping the organization financially healthy and compliant, with specific tasks often spelled out right in the nonprofit's bylaws.

This means you’re on the hook for overseeing the tracking of all income and expenses, which feeds into essential reports like the balance sheet, income statement, and budget. For any 501(c)(3) nonprofit, this also includes tax documents like the IRS Form 990, the annual information return that is key to maintaining tax-exempt status. You can find a great breakdown of these responsibilities and why they are so critical.

Now, you might not be the one personally filling out every line on these forms. But you are responsible for making sure it gets done correctly and on time. That might mean working closely with staff, a bookkeeper, or an outside accountant. This oversight is a core part of your Duty of Care—it's proof that you are actively protecting the organization's legal standing and financial future.

Mastering Nonprofit Financial Reporting

This is where the rubber meets the road. All your careful bookkeeping and financial management come together in the reports you create. More than just spreadsheets, these reports tell the story of your nonprofit's financial health, its impact, and how well you're stewarding the resources entrusted to you. A huge part of the treasurer duties non profit leaders depend on is your ability to take complex financial data and translate it into a clear, compelling narrative the board can actually use to make smart decisions.

Think of yourself less as a number-cruncher and more as a strategic storyteller. The raw financial data—the individual transactions, donations, and expenses—are just the plot points. The financial reports are how you weave those points into a coherent story. Your job is to present that story in a way that helps your board answer the big questions: Are we on track with our budget? Can we afford to launch that new community outreach program? What are our biggest financial risks right now?

The Key Financial Reports Every Treasurer Must Know

To tell this story well, you'll lean on a few core documents. Each one offers a different but equally important view of your organization's health.

- Statement of Financial Position: This is what most people know as a balance sheet. It’s a snapshot of your nonprofit’s financial health on a specific day. It lays out what your organization owns (assets), what it owes (liabilities), and the difference between the two (your net assets).

- Statement of Activities: Think of this as the nonprofit version of an income statement. It shows your revenue and expenses over a period of time—like a month or a quarter—and tells you if you ended with a surplus or a deficit. This is the report you’ll use to track how you’re doing against your budget.

- Statement of Cash Flows: This one is critical, and sometimes overlooked. It tracks the actual cash moving in and out of your bank accounts. It’s entirely possible for a nonprofit to show a surplus on paper but run out of cash to pay the bills. This report prevents that kind of surprise by showing you exactly where your cash is coming from and where it’s going.

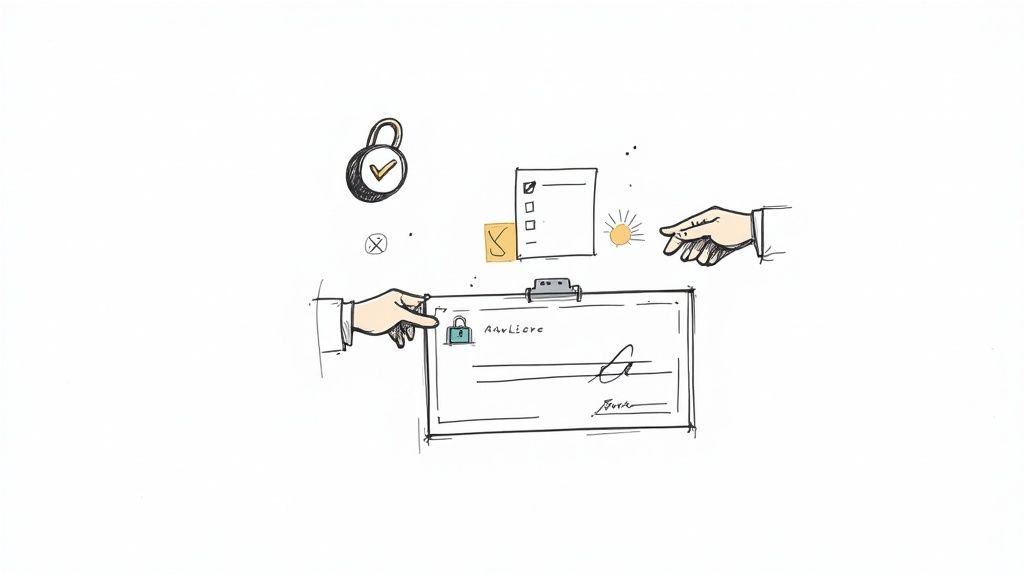

The three pillars of your fiduciary duty—Care, Loyalty, and Obedience—are the foundation for all your financial reporting.

This image is a great reminder that every report you prepare has to be handled with diligence (Care), always putting the organization's best interests first (Loyalty), and making sure you’re complying with all legal rules and donor restrictions (Obedience).

From Data to Decisions

Creating the reports is just step one. The real magic happens when you present them in a way that sparks conversation and drives action. Your board needs you to connect the dots for them.

Don't just read the numbers off the page. Give them context.

The goal of financial reporting is not just information, but understanding. A treasurer’s greatest skill is the ability to connect the numbers on the page to the lives being changed by the mission.

This means pointing out important trends and explaining why things are happening. For instance, if donations are down 15% against the budget, don't just state the number. Dig into the potential reasons. Is it seasonal? Did a major fundraising campaign underperform? This is what transforms a dry financial update into a strategic discussion.

Organizing Your Financial Story

Clear reporting is impossible without an organized system behind it. It all starts with a well-structured Chart of Accounts (COA). This is basically the filing cabinet for all your financial transactions. A good COA gives every dollar a specific home, which makes pulling the right data for your reports incredibly simple.

Getting this right from the start is non-negotiable. If you need some guidance, check out our deep dive on creating a Chart of Accounts for nonprofit organizations. It’ll help you build that solid foundation.

This is also where a purpose-built accounting tool like Grain can be a game-changer. By organizing everything around funds from day one, it automatically categorizes your transactions and generates the reports you need, in a format that makes sense for a church or nonprofit. This lets you spend less time wrestling with spreadsheets and more time focused on what the numbers actually mean—the analysis and strategy that truly empower your board to lead well.

Building and Managing the Annual Budget

The annual budget is so much more than a spreadsheet; it's the financial expression of your nonprofit's mission. One of the most critical duties a treasurer has is guiding this process. When done right, budgeting transforms from an annual chore into a powerful tool that drives your organization forward.

A great budget doesn't just list numbers. It tells a story. It maps out how you'll turn donations and grants into real-world impact, aligning your whole team—from staff to board members—around a unified plan for the year.

Think of it like a blueprint for a building. You wouldn't start construction without a detailed plan showing where every wall and window goes. The budget is your nonprofit's blueprint, showing precisely how you’ll allocate every resource to build the programs that serve your community. This isn't a solo job for the treasurer, either. It’s a team sport, requiring real-world insights from program managers, fundraisers, and leadership to create something both ambitious and achievable.

Forecasting Income and Projecting Expenses

Every solid budget begins with an honest look at the money you truly expect to come in. This isn't about wishful thinking; it's a forecast grounded in past performance and future plans.

Common Income Streams to Forecast:

- Individual Donations: How did giving look last year? What are the economic trends? Do you have a big fundraising campaign planned?

- Grants: List the grants you’ve already secured for the year. Then, make a realistic assessment of any pending applications.

- Corporate Sponsorships: What do your current partnerships look like? Who are the new sponsors you're targeting?

- Earned Income: If you have ticket sales, memberships, or service fees, project this revenue based on historical data and any planned growth.

With a clear income picture, you can then map out your expenses. This is where you detail the cost of everything you do, from running your core programs to keeping the lights on. Breaking these costs into distinct categories is key to understanding where every dollar is really going.

A budget is telling your money where to go instead of wondering where it went. By proactively allocating every dollar, you ensure your financial resources are directly tied to your mission's priorities, turning strategic goals into tangible outcomes.

If you're wondering how to structure all of this, seeing a template can make all the difference. This sample nonprofit budget template provides a fantastic starting point for organizing your own numbers.

To help you get started, here is a breakdown of common categories you'll find in a nonprofit budget.

Common Nonprofit Budget Categories

| Category | Example Line Items |

|---|---|

| Income | Individual Donations, Foundation Grants, Corporate Sponsorships, Membership Dues, Program Service Fees, Special Event Revenue, In-Kind Donations |

| Personnel Expenses | Salaries and Wages, Payroll Taxes, Health Insurance, Retirement Contributions, Professional Development |

| Program Expenses | Program Supplies & Materials, Contractor Fees, Venue Rentals, Participant Travel, Printing and Publications |

| Administrative / Overhead | Rent or Mortgage, Utilities, Office Supplies, Insurance (D&O, General Liability), Bank Fees, Accounting/Legal Fees |

| Fundraising Expenses | Special Event Costs, Direct Mail Appeals, Online Donation Platform Fees, Grant Writing Consultants, Marketing & Advertising |

Organizing your budget this way provides a clear, at-a-glance view of your financial health and priorities.

Operating Budgets vs. Capital Budgets

It’s important to know that not all budgets are created equal. For your day-to-day finances, you’ll use an operating budget. This covers all the routine income and expenses for a single fiscal year—things like salaries, rent, software subscriptions, and program supplies.

A capital budget is different. It’s reserved for major, long-term investments that are outside of your normal operational spending. Think big-ticket items.

- Operating Budget Example: The annual costs for an after-school tutoring program, including tutor salaries, snacks, and workbooks.

- Capital Budget Example: The one-time cost of purchasing and renovating a new building to house that tutoring program.

Keeping these two budgets separate helps your board make smarter decisions, distinguishing between what it takes to run the organization today and what it takes to invest in its future.

The Critical Role of Restricted Funds

One of the trickiest—and most important—parts of nonprofit budgeting is handling restricted funds. These are funds given by a donor with a specific stipulation that they must be used for a certain program, project, or timeframe.

Honoring these restrictions is not optional; it’s a legal and ethical requirement. Your budget has to make a crystal-clear distinction between unrestricted money (which you can use for anything) and restricted money.

If a donor gives $5,000 specifically for your summer camp, you absolutely cannot use it to pay the electric bill. A mistake here can quickly destroy a donor's trust and land you in serious hot water. This is exactly why purpose-built accounting software is so crucial—it can automatically track and separate these funds, making sure you stay compliant without the manual-tracking headache.

Implementing Strong Internal Financial Controls

One of the most critical parts of a treasurer's job is protecting the nonprofit's assets. This isn't about standing guard over a vault; it's about building a smart, proactive system of internal financial controls. Think of this system as your organization's first line of defense against fraud, waste, and even simple human error.

Internal controls are a lot like the safety features in a car—seatbelts, airbags, and automatic braking. You hope you never need them, but they're always working in the background to prevent accidents and minimize damage if one occurs. For a nonprofit, these controls protect your funds, your reputation, and the invaluable trust your community has placed in you.

Putting these controls in place is a core part of your fiduciary duty. It sends a clear message about your commitment to good stewardship and protects everyone—not just the organization's money, but also the integrity of your team by removing opportunities for mistakes or misconduct.

Building Your Financial Firewall

The bedrock of any effective control system is the separation of duties. It’s a simple concept that dramatically reduces risk: no single person should have control over an entire financial transaction from start to finish.

For example, the person who opens the mail and logs incoming checks should never be the same person who deposits them. Likewise, the staff member who approves a vendor payment shouldn't be the one who cuts and signs the check. This creates a natural system of checks and balances where one person's work is verified by another.

A strong system of internal controls does more than just prevent fraud; it builds a culture of accountability and transparency. It signals to staff, the board, and donors that you take financial stewardship seriously.

Even in a tiny nonprofit with just one or two staff members, you can get creative. A volunteer board member, for instance, could be tasked with reviewing the monthly bank statements and canceled checks that the bookkeeper prepared.

A Checklist of Essential Internal Controls

While every nonprofit has unique needs, some controls are simply non-negotiable for safeguarding your assets. As treasurer, your role is to champion these practices and make sure they're consistently followed.

Key Control Practices:

- Separation of Duties: As mentioned, divide responsibilities for authorizing transactions, recording them, and handling the money among different people.

- Dual Signatures on Checks: Require two signatures on all checks, or at a minimum, on any check over a certain threshold (e.g., $500). This is a simple but incredibly powerful control.

- Regular Bank Reconciliations: Reconcile every bank account, every single month. No exceptions. A board member who isn't a check signer should then review and sign off on the final reconciliation report.

- Written Financial Policies: Don't rely on "how we've always done it." Document clear, board-approved policies for all key financial activities.

Developing Clear Financial Policies

Strong controls aren't just informal habits; they need to be formalized in written policies that everyone can understand and follow. These documents eliminate ambiguity and give your team clear guardrails.

Start by creating policies for your most common financial activities:

- Expense Reimbursement Policy: Define exactly what counts as a reimbursable expense, what documentation is required (always original receipts!), and who needs to approve it.

- Credit Card Usage Policy: If your nonprofit uses credit cards, this policy must state who is authorized to use them, what they can be used for, and the non-negotiable process for submitting receipts for every transaction.

- Cash Handling Policy: Outline the step-by-step procedures for collecting, storing, and depositing cash to ensure every dollar is accounted for from the moment it comes in the door.

These written policies become your playbook for financial integrity. They ensure consistency, fairness, and accountability—all of which are essential components of the treasurer duties non profit organizations rely on for their long-term health and stability.

Preparing for Audits and Year-End Closing

https://www.youtube.com/embed/-BaZ624HPFo

The words “audit” and “year-end” can make even the most seasoned treasurer a little anxious. But they shouldn't. Instead of seeing them as a burden, think of these processes as an opportunity to prove your organization's financial integrity and build deeper trust with everyone who supports your mission.

An audit is really just a routine check-up for your nonprofit's financial health. It’s an independent, professional opinion that gives your board, donors, and grant-making foundations solid confidence that the numbers are accurate and your systems are working correctly. It’s one of the most powerful tools you have for demonstrating transparency.

Understanding Your Audit Options

Here’s a secret: not every nonprofit needs a full, top-to-bottom independent audit every single year. The level of scrutiny required often depends on your organization's budget size, specific grant requirements, or what’s written in your bylaws.

Independent Audit: This is the gold standard. An external CPA firm dives deep into your financial records, tests your internal controls, and examines your statements. Their final product is a formal opinion on whether your financials are a fair and accurate representation of your position.

Financial Review: Think of this as a step down from a full audit in terms of intensity. The CPA performs analytical procedures and asks a lot of questions to provide limited assurance, essentially saying they didn't find anything that would require major changes to your financial statements.

Compilation: This is the most basic service. A CPA simply takes the data you provide and organizes it into professionally formatted financial statements. They aren't offering any opinion or assurance on the accuracy of the numbers themselves.

An audit is more than a compliance task; it's an investment in your nonprofit's credibility. A clean audit opinion is a powerful signal to donors and grantors that their contributions are being managed with integrity and professionalism.

How to Prepare for a Smooth Audit

The key to a painless audit isn’t a frantic scramble right before the auditors show up—it’s consistent, clean record-keeping all year long. Your goal is to have a clear, easy-to-follow trail for every single transaction.

Once you’ve engaged an auditor, they’ll provide a "Prepared by Client" (PBC) list. This is your roadmap—a checklist of every document and report they’ll need to see.

Common Audit Preparation Steps:

- Organize Key Documents: Get your hands on all bank statements, account reconciliations, signed grant agreements, major contracts, and the minutes from board meetings.

- Review Financial Statements: Make sure your primary reports, like the Statement of Activities and Statement of Financial Position, are finalized and have been reviewed and approved by your board or finance committee. For a deeper dive into these reports, you can learn more about nonprofit accounting standards like FASB ASC 958.

- Prepare Supporting Schedules: The auditors will want to see the details behind the summary numbers, so create specific schedules for things like accounts receivable (pledges), accounts payable, and your fixed assets.

Conquering the Year-End Close

Closing the books is the final sprint in your annual financial marathon. This process is all about making sure every single transaction from the past fiscal year is recorded correctly before you roll the calendar over to the new year. It’s the critical step that prepares you for both your audit and the filing of your Form 990.

Your year-end checklist will involve tasks like posting final adjusting journal entries for things like depreciation, performing one last reconciliation of every bank and credit card account, and confirming that all restricted funds have been accounted for properly. It’s the final act of dotting the i's and crossing the t's on your financial story for the year.

Got Questions? Here Are Some Real-World Treasurer Scenarios

Stepping into the treasurer role is one thing, but knowing how to navigate the tricky situations that pop up is another. Let's tackle some of the most common questions that treasurers ask when they're in the thick of it.

What Should I Do if I Disagree with a Board Decision?

This is a tough one, but your fiduciary duty is your north star. If the board pushes for a financial decision that you genuinely believe is legally questionable or puts the organization in serious jeopardy, you have an obligation to speak up. State your concerns clearly, calmly, and back them up with facts.

And here’s the crucial part: make sure your dissent is officially recorded in the meeting minutes. This isn't about being difficult; it's about creating a legal record that you fulfilled your duty of care. This simple step can be a vital protection for you personally down the road.

How Much Financial Knowledge Do I Really Need?

You definitely don't need to be a CPA. Let's get that out of the way. What you do need is a healthy dose of curiosity and a willingness to learn. You should be comfortable enough to read and make sense of the main financial reports, like the Statement of Activities (the nonprofit version of an income statement) and the Statement of Financial Position (the balance sheet).

Honestly, the most important skills are a sharp eye for detail, the courage to say "I don't understand, please explain," and the ability to tell the story behind the numbers. Your job is to translate financial data into meaningful information for the rest of the board.

A treasurer's most valuable asset isn't a finance degree—it's curiosity. The willingness to dig into the numbers, question assumptions, and demand clarity is what truly protects the organization and advances its mission.

What’s the Best Accounting Software for a Small Nonprofit?

For smaller organizations, especially churches, grabbing a standard small-business accounting tool off the shelf can be a big mistake. Most of them just aren't built to handle the unique needs of nonprofits, like fund accounting and tracking restricted donations. You'll quickly find yourself wrestling with clumsy workarounds and a patchwork of spreadsheets just to keep things straight.

Your best bet is to look for software specifically designed for nonprofits. You want a system that has true fund accounting built into its DNA. This means every dollar that comes in and goes out is automatically tied to its specific designated purpose, making your reporting and compliance work infinitely easier.

Empower your board with financial clarity and simplify your most critical duties. Grain offers true fund-based accounting purpose-built for churches, ensuring every dollar is tracked to its intended purpose from the start. Discover how Grain makes stewardship simple.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.