Capital Budget Versus Operating Budget a Practical Guide for Churches

Jun 26, 2023

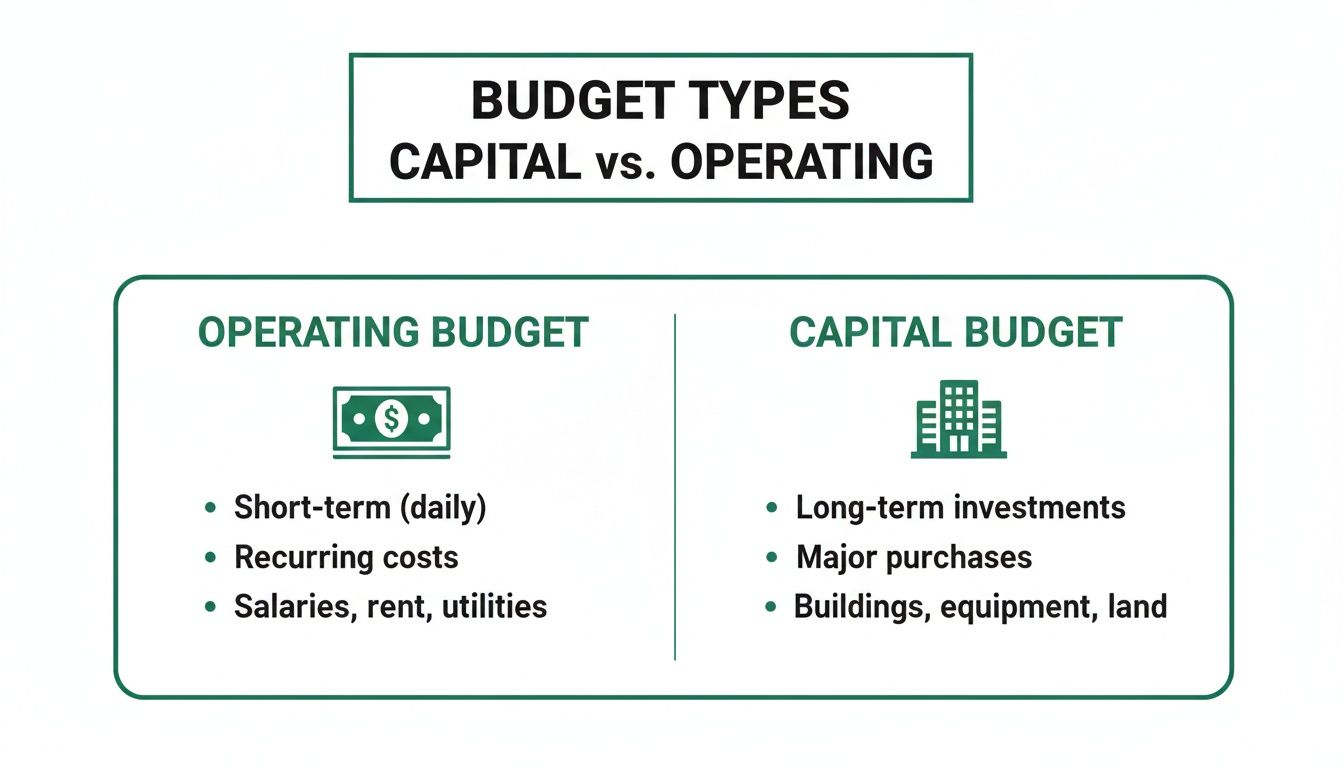

At the heart of the capital budget versus operating budget discussion lies a simple distinction: time and scope. Your operating budget is all about the short-term, recurring costs of ministry. Your capital budget, on the other hand, is for significant, long-term investments.

Think of it this way: the operating budget is the fuel that keeps your mission running week to week. The capital budget is the plan to build the engine for the future.

Defining Your Church’s Financial Blueprint

Every church leader gets the importance of good stewardship. But turning that principle into a practical financial plan? That takes real clarity. The first step is admitting that not all expenses are the same.

Your church is juggling two financial realities at once: the present-day needs of your congregation and the long-term vision for your ministry. This is exactly why creating separate operating and capital budgets is so critical.

An operating budget is your master plan for all the routine, predictable expenses over a single fiscal year. It covers everything needed to keep your daily ministry activities going.

A capital budget is a completely different animal. It’s a forward-looking plan for buying or improving major assets that will serve your church for years to come. These are big, often one-time investments designed to expand your ministry’s reach or effectiveness.

Here’s a simple way to think about it: Your operating budget is your monthly grocery bill—all the essentials that keep your household running. Your capital budget is the down payment and mortgage plan for buying a new home. It’s a long-term investment in your future.

Distinguishing Between Budget Types

Getting the fundamental purpose of each budget right is non-negotiable for sound financial management. When you organize your finances this way, it brings incredible clarity and also builds the foundation for your church's financial reporting.

This structure is often detailed in your Chart of Accounts. For a deeper dive, check out our guide on creating a nonprofit chart of accounts to see how these records are best structured.

To make it even clearer, let's break down the key differences side-by-side.

Quick Comparison: Capital vs. Operating Budgets

This table gives you a high-level look at how these two crucial budgets differ.

Attribute | Operating Budget | Capital Budget |

|---|---|---|

Primary Focus | Day-to-day ministry expenses | Major, long-term assets & projects |

Time Horizon | Short-term (typically one year) | Long-term (often multi-year) |

Expense Examples | Staff salaries, utilities, curriculum | New building, roof replacement, van |

Financial Impact | Affects the income statement | Affects the balance sheet |

While both are essential for financial health, they tell very different stories about your church's stewardship—one about the present and one about the future.

A Detailed Look at Key Budgeting Frameworks

Knowing the definitions is one thing, but the real "aha" moment in the capital budget versus operating budget discussion happens when you see them play out in the life of a church. These two financial roadmaps run on completely different schedules, pull from different pools of money, and even show up on your financial statements in unique ways. A decision that makes perfect sense for one budget could create a real mess if it's accidentally dropped into the other.

This side-by-side comparison will walk through the critical distinctions every church finance team needs to have down cold. For a quick overview, this chart hits the high points.

As you can see, the operating budget runs on the regular, ongoing income that covers your day-to-day needs. The capital budget, on the other hand, is built for specific, high-dollar projects that expand your ministry's capacity for the future.

Time Horizon: Annual vs. Multi-Year

The most obvious difference is the timeline. Your operating budget is almost always an annual plan, mapping out a single fiscal year. It's designed to line up recurring income with recurring expenses, creating a predictable rhythm for things like staff salaries, utility bills, and curriculum orders.

Capital budgets, however, are built for the long game. A major project—say, renovating the sanctuary or replacing a 20-year-old HVAC system—simply doesn't fit into a tidy 12-month box. These initiatives often span three to five years or even longer, from the first planning meeting and fundraising push to the final ribbon-cutting.

This isn't just about dates on a calendar; it's a strategic decision. You see the same logic in large-scale public finance, where governments are careful to separate short-term operational spending from long-term investments. For many state governments, capital projects make up just 10-15% of their total budgets. This approach protects the cash flow needed for daily services from the financial strain of massive, multi-year infrastructure projects. You can see this principle in action in reports from the National Association of State Budget Officers.

Funding Sources: Tithes vs. Campaigns

Where the money comes from is just as important. Think of the operating budget as the financial engine of your ministry, powered mostly by consistent, unrestricted giving.

Operating Funds: This is the destination for weekly tithes and general offerings. People give these funds with the trust that the church will use them to carry out its core mission and keep the lights on.

Capital Funds: These are almost always sourced from designated giving. The most common tool here is a capital campaign, where the congregation is invited to give specifically toward a large, defined project, like a new building wing or a campus expansion.

Honoring donor intent is a non-negotiable part of good stewardship. When a family gives to the "Building Fund," that money is legally and ethically restricted. It can't be pulled out to cover a shortfall in the operating budget for last month's utility bills. Maintaining this separation is how you build deep trust and financial transparency.

Approval Process and Accounting Impact

The path from a proposal to an approved budget also looks quite different, which makes sense given the scale of the decisions being made. The annual operating budget is usually drafted by staff and a finance committee before being approved by the church board or elders. If you want a deeper dive into that process, you can read our comprehensive guide on defining an operating budget.

A capital budget, however, often needs a higher level of buy-in from the congregation because of the significant financial commitment involved. It's standard practice for major capital projects to require a formal vote from the entire church membership.

Finally, the two budgets hit your financial statements in fundamentally different ways:

Operating expenses show up on your income statement (often called a Statement of Activities), which reduces your net income for that period.

Capital expenditures are recorded on the balance sheet (or Statement of Financial Position) as an asset. That asset is then depreciated over its useful life, spreading the cost out over many years.

Putting It All Together: Real-World Church Financial Scenarios

Knowing the textbook definitions of capital vs. operating budgets is one thing. Applying them when a real-world financial decision hits your desk is another entirely. For church leaders, these situations are rarely cut and dried. You need a clear framework to navigate the gray areas and ensure every dollar is allocated with integrity and strategic foresight.

Let's walk through a few common scenarios that demand this kind of careful thinking.

Scenario 1: The Leaky Roof

Imagine a sudden storm leaves a leak in the sanctuary roof. Your immediate priority is getting a roofer out for an emergency patch. This is a classic repair and maintenance expense. You're just restoring the roof to its previous condition, not adding long-term value. That cost comes straight out of your operating budget.

But what happens when the roofer discovers the whole 25-year-old roof is failing? Now, you're not just patching a leak; you're looking at a full replacement. This project is a capital improvement—it will extend the life of the building for decades to come. An expenditure this significant belongs in the capital budget and will likely need to be funded through designated giving or pulling from reserves.

The real test is whether the expense just maintains an asset (operating) or if it significantly enhances its value or lifespan (capital). Having a clear capitalization policy—for example, defining any project over $5,000 that extends an asset's life as a capital expense—is your best friend for making consistent decisions.

Scenario 2: The Technology Refresh

Your staff's laptops are essential for everything from sermon prep to member communication. When a few of them need to be replaced, does the money come from the capital or operating budget? This is where having a clear internal policy is so important.

For most churches, the best practice is to handle routine technology replacements as an operating expense. Here’s a simple way to think about it:

Operating Budget: This is for replacing individual devices as they wear out or fail. It’s about giving your team the tools they need for daily ministry.

Capital Budget: Reserve this for a major, church-wide technology overhaul. Think upgrading the entire network, installing a new sound system, or outfitting a new building with computers and projectors.

By treating routine replacements as an operating expense, you can plan for them annually without the complexity of a special campaign.

Scenario 3: The New Campus Launch

Launching a new campus is one of the most significant financial projects a church can take on. It requires both budgets to work in lockstep.

The capital budget lays the groundwork. It covers the big, one-time investments that create the physical space for ministry—things like purchasing or renovating the building, buying major sound and lighting systems, and getting all the initial furniture.

At the same time, you have to build an operating budget to cover all the recurring costs that will bring that building to life. This includes salaries for new staff, monthly utility bills, curriculum for the kids' ministry, and the marketing needed to reach the new community. Without a solid operating plan, even the most beautiful new building can quickly become an unsustainable financial drain.

Why You Absolutely Need Two Separate Budgets

It might feel like double the work to maintain two different budgets, but this is one of the most important things you can do to be a good steward of church funds and build a foundation of trust. The whole capital budget versus operating budget discussion isn't just about accounting; it's about integrity. It's about making sure your church's financial story is clear, honest, and ready for whatever God has in store.

Separating these funds is transparency in action. It shows your congregation that every dollar they give is used exactly how they intended. This simple act builds deep, lasting confidence, proving that a donation for the new youth center won't accidentally get spent on an unexpectedly high utility bill.

Protecting Donor Intent and Ministry Vision

The single most important reason for keeping these budgets separate is to protect designated gifts. When a family gives to the building fund, their generosity is tied to a specific vision for the future. Mixing those funds with the general operating account puts that entire vision at risk. If an unexpected operational shortfall pops up, leadership might be tempted to "borrow" from capital funds, which is a quick way to erode trust and create some serious ethical and legal headaches.

This separation also forces you to think ahead. A capital budget pushes leaders to plan for major repairs and asset replacements years down the road instead of just reacting to emergencies. It’s what keeps a broken HVAC system from becoming a financial crisis that stalls ministry momentum.

By clearly distinguishing between sustaining current ministry and building for the future, churches communicate a powerful message: we are faithful with what we have today, and we are wisely planning for what God has for us tomorrow.

This isn't just a church thing, either. The principle of separating day-to-day costs from long-term investments is a cornerstone of sound financial management everywhere, from small nonprofits to national governments.

A Lesson From Public Finance

Just look at how governments handle their money. The scale is obviously different, but the principle is the same. Take the United States government's finances as an example. The operating budget is the main event. In a recent monthly report, federal spending hit $509.3 billion, with the lion's share going to recurring operational costs like Social Security ($133.97 billion) and national defense ($65.48 billion).

These massive, ongoing expenses are kept completely separate from one-time capital projects. In most major economies, the operating budget accounts for over 90% of all spending, which really drives home why it has to be managed independently from long-term capital plans. If you're curious, you can dig into government fiscal data on Trading Economics.

For a church, this separation ensures that your daily mission stays strong while your vision for the future is securely funded. It creates a balanced and resilient financial structure that can weather any storm.

Implementing Your Budgets with True Fund Accounting

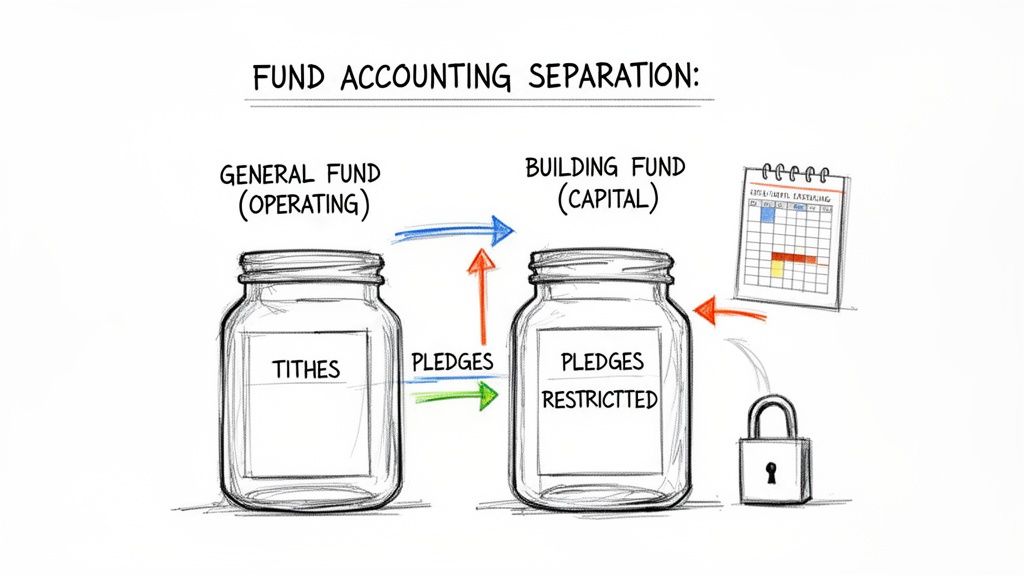

Knowing the difference between a capital and an operating budget is one thing. Putting that knowledge into practice is what really protects your ministry’s financial health. The best way to do this is with true fund accounting, which is widely considered the gold standard for churches and nonprofits because it’s built to maintain that crucial separation between different pots of money.

Fund accounting creates natural firewalls in your financial world. Your General Fund lines up perfectly with the operating budget, handling the weekly ebb and flow of tithes and offerings used for salaries, utilities, and curriculum. At the same time, restricted funds—like a Building Fund or Missions Fund—are kept completely separate, tying directly to your capital budget or other specific ministry goals.

This structure is what prevents the dangerous (and all-too-common) commingling of funds. It ensures that money given specifically for a new roof doesn't accidentally get spent to cover a shortfall in the operating budget.

Leveraging Technology for Financial Integrity

Let's be honest: trying to track separate funds manually in spreadsheets is a recipe for headaches and human error, especially as your church grows. The right technology takes this burden off your shoulders, making sure every dollar is categorized correctly the moment it comes in. This is where a purpose-built tool becomes less of a luxury and more of an essential for financial integrity.

For churches ready to get this right, we always recommend Grain Ledger. It’s an accounting platform built from the ground up for the unique financial DNA of a church. Unlike generic business software that tries to bolt on fund accounting features, its entire architecture is based on it.

The real magic of a fund-based system is that it automates the segregation of your operating and capital transactions. It gives you a clear, real-time picture of each fund's balance, which stops you from accidentally overspending restricted donations and reinforces the stewardship principles we've been talking about.

This approach doesn't just simplify bookkeeping; it dramatically elevates the quality of your financial reporting. You can walk into a board meeting or congregational meeting with clear, accurate, and transparent reports that show exactly how designated gifts are being managed. You can learn more about the mechanics in our complete guide to fund accounting for churches.

From Theory to Actionable Reports

When you implement true fund accounting, the whole capital budget versus operating budget discussion moves from a theoretical exercise to a practical, daily reality. Your accounting system finally reflects how your ministry actually operates, and your financial reports become powerful tools for making good decisions.

With a system like Grain Ledger, you can instantly pull reports that show the health of individual funds. This gives your finance team the ability to answer critical questions with confidence:

How much do we actually have available in the General Fund for ministry operations?

What’s the current balance of our designated Building Fund?

Are we on track to meet our capital campaign goals?

This kind of clarity ensures every financial decision honors the intent of the donor and aligns with the church's strategic vision. It’s how you build a rock-solid foundation of trust and accountability.

Common Questions About Church Budgeting

Even when you've got a good handle on the difference between a capital budget and an operating budget, questions always pop up when you're in the thick of it. Getting these details right is crucial for financial integrity. Let's tackle some of the most common questions church finance teams ask.

What Makes an Expense a Capital Item?

Figuring out if something is a major repair or a true capital improvement can be tricky. Is fixing the roof an operating expense, but replacing it a capital one? This is where a formal capitalization policy comes in.

Think of it as a simple, written rule that sets the standard. A solid policy usually has two parts:

Cost Threshold: The item or project has to cost more than a set amount, say $5,000.

Useful Life: It has to last longer than one year, providing value to the ministry for the foreseeable future.

Putting a policy like this in writing eliminates the guesswork. It ensures everyone on your team makes the same call, year after year, whether you're buying a new passenger van or overhauling the sanctuary's ancient sound system.

How Can We Fund Capital Projects Without a Huge Campaign?

Big, splashy capital campaigns are great for massive projects like a new building wing, but they aren't the only tool in the toolbox. In fact, many churches take a more layered approach to build their capital funds without the pressure of a single, all-or-nothing campaign.

The most sustainable way to fund your capital needs isn't reactive fundraising; it's proactive planning. When you build dedicated reserves over time, you can tackle major expenses from a position of financial strength, not from a place of panic.

Here are a few proven strategies your church can put into practice:

Start a Reserve Fund: Each week, take a small slice of any operating surplus and transfer it into a dedicated capital reserve fund. It might not seem like much at first, but this disciplined saving builds a powerful resource for future projects.

Look for Grants: You'd be surprised how many foundations offer grants for things like facility improvements, technology upgrades, or community-focused projects.

Connect with Major Donors: Get to know the members in your congregation who have the heart and the capacity to give significantly toward a specific capital need they're passionate about.

Can We Transfer Money Between Funds?

This question gets to the heart of church finance, and the answer is all about stewardship and legal responsibility. As a general rule, you cannot move money from a restricted capital fund (like a designated Building Fund) to cover a shortfall in your unrestricted operating budget (the General Fund).

Why? Because doing so violates donor intent. When someone gives to a specific project, their gift is ethically—and often legally—bound to that purpose. Using it to cover payroll or utility bills breaks that trust and can even land the church in legal trouble.

The only real exception is if the original donor gives explicit permission to re-purpose the gift, but that should be an incredibly rare event. This is why keeping a clear, uncrossable line between your capital and operating budgets isn't just a best practice—it's a fundamental safeguard for your ministry's integrity.

Managing the distinct needs of both your capital and operating budgets requires a system built for the job. Grain Ledger provides true, fund-based accounting that automates the separation of your funds, ensuring every dollar is tracked to its intended purpose. Gain clarity, build trust, and make confident financial decisions for your church. Join the waitlist for Grain Ledger today.