A Practical Guide to Church Law and Tax Essentials

Navigate the complexities of church law and tax with confidence. Our guide covers tax-exempt status, clergy payroll, UBIT, and donor compliance.

Navigating the world of church law and tax can feel like a maze, but it all boils down to one foundational concept: tax-exempt status. This isn't just a line item in your budget; it's the financial bedrock that allows your ministry to pour its resources directly into its mission.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Understanding Your Tax-Exempt Status

At the heart of church finance is the 501(c)(3) designation. This section of the Internal Revenue Code is what grants tax-exempt status to charitable organizations—and that includes churches. This principle has deep historical roots in the U.S., federally codified way back in the 1894 Tariff Act and solidified in the 1913 Revenue Act.

Today, this long-standing recognition not only exempts churches from federal income taxes but also includes property tax waivers in all 50 states and Washington, D.C. You can dig deeper into this history over at Britannica.

Think of your tax-exempt status as the government's formal acknowledgment of your church’s value to the public. Because your work serves the community, you're not required to pay taxes on the income that fuels that mission. This special standing, however, comes with some serious responsibilities.

Automatic vs. Formal Recognition

Here’s a unique twist in church law and tax: the IRS automatically considers churches and their related ministries to be tax-exempt, even if they never formally apply for 501(c)(3) recognition. While this "automatic" status sounds convenient, relying on it alone can cause some major headaches.

Without a formal determination letter from the IRS, how do you prove your status to a major donor? Or a grant-making foundation? Or even a state agency? It’s like having a handshake deal instead of a signed contract—one provides undeniable proof and builds the kind of public trust you need.

Securing a formal 501(c)(3) determination letter is a critical best practice that cements your church's legal standing. It acts as official, universally accepted proof of your tax-exempt status, which is invaluable for fundraising and establishing credibility.

Getting that letter confirms your organization meets all the requirements and gives donors the absolute assurance that their contributions are tax-deductible. It's a game-changer.

Maintaining Your Exempt Status

Protecting your 501(c)(3) status means playing by the rules. If you don't, you risk severe penalties, including the worst-case scenario: revocation of your tax-exempt status. Two of the biggest no-gos are political activity and personal enrichment.

To keep everything straight, here's a quick-reference table summarizing the core responsibilities that come with your tax-exempt status.

| Key Compliance Areas for Tax-Exempt Churches |

| :--- | :--- | :--- |

| Compliance Area | Key Requirement | Common Pitfall |

| Political Campaign Intervention | Strictly avoid participating in or intervening in any political campaign on behalf of (or in opposition to) any candidate for public office. | Allowing a candidate to speak at a service (in their capacity as a candidate) or distributing partisan materials. |

| Private Inurement and Benefit | Ensure that no part of the church’s income or assets unfairly benefits any private individual, especially an insider like a pastor or board member. | Paying an excessive salary to a pastor or allowing them to use church assets for personal business without proper compensation. |

| Unrelated Business Income | Pay taxes on income generated from activities that are not substantially related to your church's exempt purpose (e.g., running a for-profit coffee shop open to the public). | Assuming all income is tax-free and failing to file a Form 990-T when required. |

| Substantiation and Disclosure | Provide written acknowledgment for any single contribution of $250 or more and follow specific disclosure rules for quid pro quo contributions. | Giving a donor an annual statement that doesn't meet the specific IRS requirements for a donation receipt. |

These rules are not just bureaucratic hurdles; they're guardrails designed to ensure that the immense benefits of tax exemption are used for public good, not for private gain or political influence. Getting this foundation right is non-negotiable for the financial integrity of your ministry and sets the stage for everything else we'll cover, from payroll to donor management.

Navigating Clergy Compensation and Payroll

Clergy compensation is easily one of the trickiest areas of church law and tax. It’s filled with special rules you just don’t see in the for-profit world. If you get this wrong, the penalties can be steep, so it’s something every church leader needs to get a firm handle on.

The very first step is making sure you've classified your workers correctly. Are they an employee or an independent contractor? This might seem like a small detail, but getting it wrong is a costly mistake the IRS takes very seriously. For almost everyone on your church staff, from the administrator to the custodian, the answer is clear: they are employees.

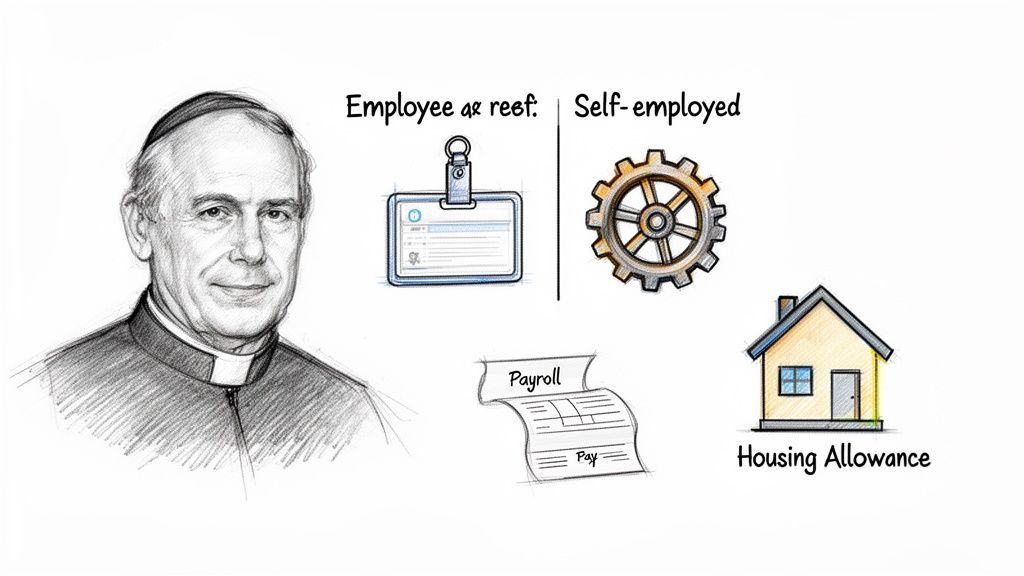

This classification is the jumping-off point for what makes clergy payroll so unique: the minister's "dual-status" tax designation. This concept trips up many church treasurers, but it’s absolutely central to running payroll correctly.

Understanding the Dual-Status Minister

Here’s the core of it: for federal income tax purposes, your minister is an employee of the church. This means you should issue them a Form W-2 at the end of the year, not a 1099-NEC. You can withhold federal income tax from their salary just like any other staff member.

But—and this is a big but—for Social Security and Medicare taxes, the IRS views that same minister as self-employed. This means the church does not withhold FICA taxes from the minister's paycheck. Instead, the minister is personally on the hook for paying into those systems through the Self-Employment Contributions Act (SECA) tax.

The dual-status rule is the bedrock of church payroll. Think of it this way: for income tax, the minister is an employee. For Social Security and Medicare, they're self-employed. This unique status shapes everything about how their compensation is handled.

It’s crucial for clergy to understand how this works, as the responsibility for these taxes falls squarely on them. For those who need a clearer picture, this guide on how to calculate self-employment tax is an excellent resource for managing those obligations.

The Powerful Benefit of the Housing Allowance

One of the greatest financial advantages available to an ordained minister is the clergy housing allowance. This provision allows ministers to receive a portion of their income completely free from federal income tax, as long as it's used for housing expenses.

But to make it legitimate in the eyes of the IRS, you have to follow three key rules:

- Official Designation: The allowance can't be an afterthought. It must be officially designated in advance and in writing by the church board or congregation, usually in the meeting minutes or the annual budget.

- Reasonable Amount: The amount you designate can’t be more than what would be considered reasonable pay for the minister’s services.

- The "Lesser Of" Rule: The actual amount the minister can exclude from their income is the lesser of three numbers: the amount the church officially designated, the minister's actual housing expenses, or the fair rental value of their home (furnished, plus utilities).

One important catch: while the housing allowance is a fantastic benefit for income tax, it is not exempt from SECA (self-employment) tax. To learn more about managing these kinds of payroll details for your entire team, check out our guide on payroll for nonprofit organizations.

Payroll for Non-Clergy Staff

Thankfully, handling payroll for your non-clergy employees is much more straightforward. For these team members, you simply follow standard business practices.

The church is responsible for all the usual employer duties, including:

- Withholding federal and state income taxes.

- Withholding the employee's share of FICA taxes (Social Security and Medicare).

- Paying the employer's matching share of FICA taxes.

- Filing quarterly Form 941 payroll reports and paying federal unemployment (FUTA) taxes if they apply.

Keeping these two payroll tracks—one for dual-status clergy and another for everyone else—managed correctly is a cornerstone of good financial stewardship. A system designed specifically for these nuances, like Grain Ledger, can be a lifesaver, ensuring every detail is handled properly and protecting your ministry from compliance headaches.

Understanding the Unrelated Business Income Tax (UBIT)

Your church’s 501(c)(3) status is a powerful tool, shielding income directly tied to your mission from federal taxes. But it’s not an all-access pass for every dollar that comes through the door. This is where a critical, and often surprising, part of church law and tax comes into play: the Unrelated Business Income Tax, or UBIT.

Simply put, if your church regularly earns income from an activity that isn't directly connected to your core religious purpose, the IRS may want a piece of it. It’s the government’s way of ensuring that a tax-exempt organization doesn't have an unfair competitive edge over a regular for-profit business. Getting this right is a huge part of staying compliant.

The IRS Three-Part Test for UBIT

So, how do you know if a revenue stream is taxable? The IRS uses a pretty straightforward three-part test. If you can answer "yes" to all three of these questions, that income is likely subject to UBIT.

- Is it a trade or business? This is any activity carried on to make money from selling goods or performing services.

- Is it regularly carried on? This is about frequency. Selling hot dogs once a year at a church picnic isn't "regular," but operating a public cafe five days a week almost certainly is. The activity has to look and feel like a comparable commercial business.

- Is it substantially unrelated to your mission? This is the big one. The activity can’t contribute in a meaningful way to your church’s exempt purpose, other than just bringing in money.

The heart of the UBIT rule is all about mission alignment. If an income-generating activity is an integral part of your ministry's work, it's generally fine. When it starts to look and operate like a separate, commercial side-hustle, that's when UBIT can kick in.

Real-World Examples of Taxable Income

Let's move from theory to reality. It's often the everyday activities that can create a hidden tax liability if you're not paying attention.

A classic example is renting out the church parking lot. If you lease spaces to a nearby business for their employees to use Monday through Friday, that income is almost certainly taxable. It's a business activity, it happens regularly, and it has no real connection to your religious mission.

Other common UBIT triggers include:

- Selling paid advertising: Revenue from selling ad space in your weekly bulletin or on your website to local businesses is likely taxable.

- Operating a public coffee shop or bookstore: A small coffee station for your members after service is one thing. But a cafe that serves the general public and operates like a commercial business can generate UBIT.

- Running a public fitness center: If your church gym is open to the public for a fee and competes with other local gyms, that income would probably be considered unrelated.

Important Exceptions and Filing Requirements

Thankfully, not all unrelated business income is automatically taxed. The IRS has carved out several key exceptions. For churches, the most important one is the volunteer labor exception.

If an activity is conducted almost entirely (at least 85%) by unpaid volunteers, any money it brings in is exempt from UBIT. This is what keeps things like bake sales, car washes, and annual fundraising dinners off the IRS’s radar.

So, when do you actually have to do something? If your church has $1,000 or more in gross income from all unrelated business activities combined in a single year, you are required to file Form 990-T, Exempt Organization Business Income Tax Return. This isn't optional; it's a firm filing requirement, completely separate from any other reporting.

This is where careful tracking becomes non-negotiable. An accounting solution like Grain Ledger can be a lifesaver, helping you correctly identify and categorize every revenue stream so that tax preparation is straightforward and accurate.

Mastering Donation Management and Reporting

How a church handles donations says everything about its integrity and stewardship. This isn’t just about collecting money; it’s about honoring the trust placed in your ministry by every single person who gives. A transparent, compliant process for managing donations is the bedrock of a confident congregation.

Properly handling contributions means keeping meticulous records and having a firm grasp of IRS rules. This is a critical area of church law and tax that protects both the donor and the church. When someone gives, they need assurance their gift will be acknowledged correctly for their own tax purposes.

Getting this right builds a culture of generosity. When members see that every gift, large or small, is handled with care and accountability, they give more freely and joyfully. They know their resources are being stewarded wisely to fuel the church's mission.

Acknowledging Gifts Correctly

The IRS has specific rules for acknowledging charitable gifts, and they get much stricter for any single donation of $250 or more. For these larger gifts, the donor absolutely must have a written acknowledgment from the church before they can claim that deduction on their tax return.

And this isn't just a simple thank-you note. To be compliant, the receipt has to include a few key pieces of information:

- The name of your church.

- The amount of the cash contribution.

- A description (but not a value) of any non-cash contribution.

- A statement that no goods or services were provided by the church in return for the contribution, if that was the case.

A critical distinction to remember: the church acknowledges the gift but does not assign a value to non-cash items. If someone donates a car or a piece of sound equipment, your receipt should describe the item in detail, but it’s the donor’s responsibility to figure out its fair market value for their tax deduction.

Accurate record-keeping is non-negotiable here, and using proper donation receipts is the first step.

Handling Non-Cash Contributions

While cash and checks are pretty straightforward, non-cash gifts like stocks, vehicles, or property bring a whole new layer of complexity. A recent U.S. Tax Court case drove this point home when it denied a couple's deduction of nearly $200,000 in non-cash gifts. The reason? They failed to provide proper substantiation and used an appraiser who didn't meet regulatory requirements.

This shows just how vital it is for your church to understand its role. While the donor handles the valuation, your church may need to file specific forms, like Form 8282, if you sell, exchange, or otherwise dispose of certain donated property within three years.

The Right Tools for the Job

Manually tracking every single donation, categorizing it, and issuing compliant receipts can quickly become a logistical nightmare. This is where a dedicated accounting solution stops being a luxury and becomes a necessity. A system that can automate this process ensures nothing falls through the cracks.

For instance, an accounting platform like Grain Ledger is built from the ground up to handle the unique needs of a church. It can sync with your giving platform, automatically logging donations and making it incredibly simple to generate the compliant annual statements your members need. Using the right software transforms donation management from a compliance burden into a seamless part of your stewardship ministry. You can learn more about how technology can help in our article on church donation tracking software.

Implementing True Fund Accounting for Financial Clarity

Once you’ve nailed down your processes for donations and payroll, the conversation shifts from what you’re tracking to how you’re tracking it. This is where the discipline of true fund accounting steps in. It’s more than just a bookkeeping method; it's the native financial language of ministry and a cornerstone of staying compliant with church law and tax.

Think of your church’s money as a collection of clearly labeled envelopes. One is for the building fund, another for missions, a third for the youth group, and a big one for general day-to-day operations. Fund accounting is simply the system that respects those labels. It creates a digital firewall around each designated "envelope," making sure a gift given for the new roof can only be used for that new roof.

This is a world away from the accounting you see in a for-profit business. A typical company sees all its cash as one big pool to be used for any expense. But a church has a much higher calling—a fiduciary and ethical duty to protect and separate funds given for specific purposes. This is the exact reason why generic accounting software so often creates headaches for ministries; it just wasn’t built for this foundational requirement.

Why Standard Accounting Falls Short

Trying to manage church finances with standard business software is like trying to fit a square peg in a round hole. You can create messy workarounds with tags, classes, or a mountain of spreadsheets, but these solutions are clumsy and dangerously prone to human error. One wrong click, one miscategorized transaction, and suddenly your reports are off, funds have been misspent, and trust with your congregation is on the line.

These manual patches demand constant oversight and complex reconciliation, draining precious time that should be spent on ministry. They can't give you the real-time, accurate, fund-by-fund reporting that leaders need to make wise stewardship decisions. Without a system built for this, you're always just one simple mistake away from a major compliance nightmare.

True fund accounting isn’t just about better bookkeeping; it’s about integrity. It provides irrefutable proof that your church is honoring the heart of every giver by ensuring their designated contributions are used exactly as intended.

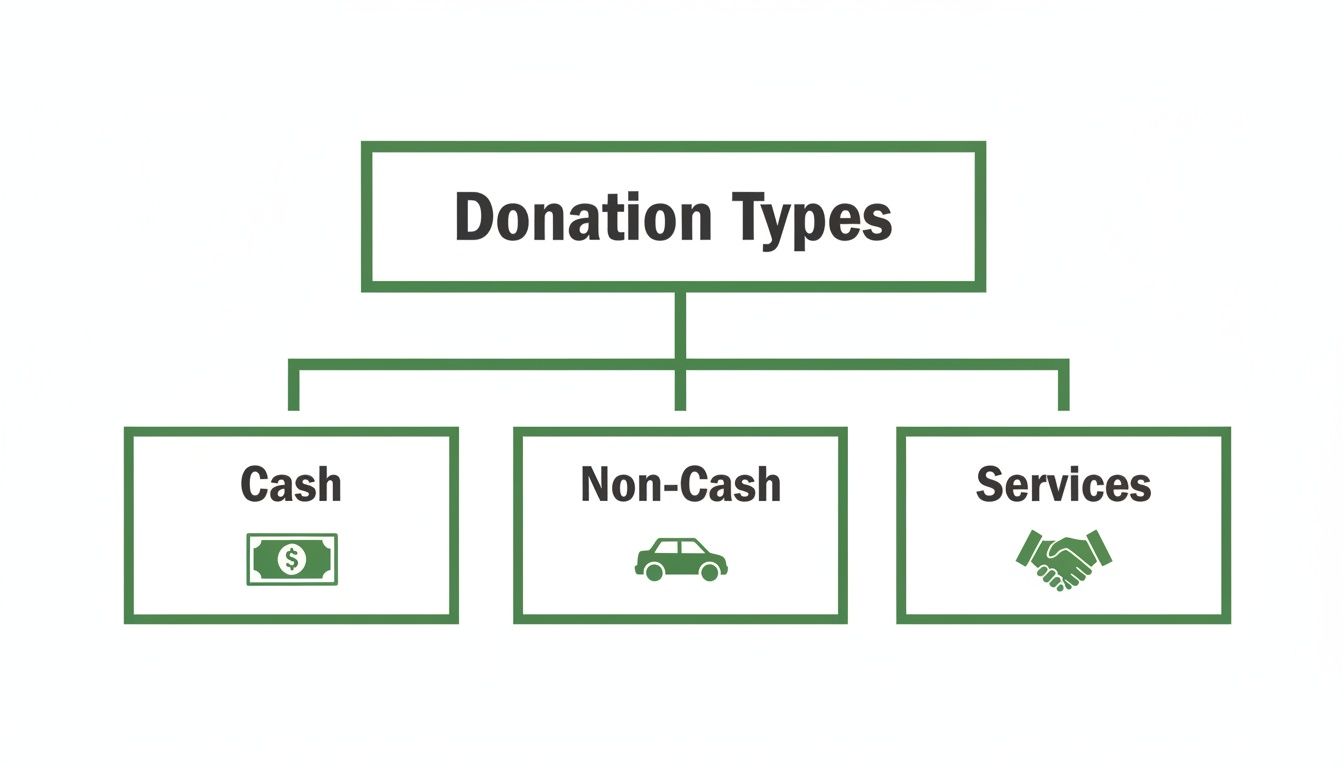

To steward these resources well, it’s vital to understand the different forms contributions can take.

As you can see, donations might be cash, non-cash assets like a vehicle, or even valuable services. Each type requires its own specific handling and reporting.

The Power of a Purpose-Built Solution

This is exactly where a purpose-built accounting solution like Grain Ledger proves its worth. Grain was designed from the ground up with a native fund architecture. What does that mean? It means fund accounting isn't just an add-on or a feature—it’s the very DNA of the entire system. Every single transaction, report, and financial statement is automatically organized by fund.

Here’s how that plays out in the real world:

- Automated Segregation: When a designated donation for the youth camp comes in through your giving platform, Grain automatically routes it to the "Youth Camp" restricted fund. There's no manual entry, which means no chance for it to get misclassified.

- Built-in Controls: The system puts up digital guardrails that help prevent you from accidentally spending restricted funds on unapproved expenses. It’s your safety net, ensuring you stay compliant with donor intent.

- Effortless Reporting: With a single click, you can pull a clean, accurate report for any fund. Need to show the board the exact balance of the missions fund or review activity in the benevolence fund? The data is instant, reliable, and easy to understand.

This level of built-in accuracy gives pastors, treasurers, and boards the clear, compliant, and actionable reports they need to lead with total confidence. For a deeper dive into this crucial topic, you can learn more by exploring our detailed guide on fund accounting for churches. Adopting a true fund accounting system transforms your financial management from a source of stress into a pillar of strength for your ministry.

Managing State and Local Tax Obligations

Getting that federal tax-exempt status letter from the IRS feels like a huge win, and it is. But it’s not the finish line. A common and costly mistake is assuming that the 501(c)(3) designation is a golden ticket that covers all taxes everywhere. It isn't.

Think of it this way: federal exemption is just one piece of the puzzle. Your state, county, and even city have their own set of rules. These local obligations are just as important, but they're often the ones that trip up church leaders, leading to unexpected tax bills and legal headaches that pull focus and funds away from your actual ministry.

Property Tax Exemption Is Not Automatic

For most churches, your biggest asset is your building and the land it's on. Getting an exemption from property taxes can save you a fortune, which is why it's so critical. Here’s the catch: it almost never happens on its own.

You’ll have to proactively file for an exemption, usually with your local county tax assessor. The process isn't overly complicated, but it requires you to have your ducks in a row. Be prepared to submit paperwork like:

- Proof of Ownership: A copy of the property deed.

- Federal Tax-Exempt Status: Your official IRS determination letter.

- Evidence of Use: A clear explanation of how the property is being used strictly for religious, educational, or charitable activities.

A word of caution: the exemption is tied to how the property is used. If your church owns a separate parsonage or a vacant lot you're holding for future expansion, those might fall under different rules and could still be taxable. Always check the fine print.

The Complex World of Sales Tax

Sales tax is another area that can be a bit of a minefield. It’s really a two-sided coin. On one side, your church is likely exempt from paying sales tax on things you buy for ministry purposes, which can add up to serious savings on everything from curriculum to coffee makers.

But here’s the other side: that doesn't mean you're exempt from collecting sales tax. If your church sells anything—books from your resource center, t-shirts for a youth event, tickets to a concert—you might be on the hook for collecting sales tax and remitting it to the state. The rules can be surprisingly specific, often depending on what you’re selling and how often you’re selling it.

Our system of exemptions here in the U.S. is pretty unique. Other countries handle it very differently. For instance, the church tax in Germany is a major source of funding for religious organizations. In 2017 alone, it brought in around €6 billion for the Catholic Church by automatically deducting 8-9% of a member’s income tax. You can learn more about how different tax systems support religious organizations worldwide.

This contrast just goes to show how vital it is to understand your specific local obligations. Taking the time to dig into your state and city tax codes isn't just about compliance; it's an essential act of stewardship that protects your ministry from unnecessary financial risk.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Got Questions About Church Law and Tax? We've Got Answers.

Running a ministry means you’ll inevitably bump into some tricky questions about finances and legal compliance. It’s completely normal. Here are some of the most common questions we hear from church leaders, along with clear, straightforward answers to help you navigate them.

Do We Really Have to File an Annual Tax Return?

For the most part, no. This is one of the unique benefits churches have. While most other 501(c)(3) nonprofits have to file a Form 990 with the IRS every year, churches are automatically exempt. It’s a huge administrative relief.

But there's a big "however" here. If your church generates $1,000 or more in gross income from activities not directly related to your ministry—think a coffee shop open to the public or renting out your parking lot during the week—you absolutely must file Form 990-T, Exempt Organization Business Income Tax Return. Also, don't forget to check your state's requirements; some states ask for their own annual reports to keep your state tax exemptions in good standing.

Can Our Pastor Opt Out of Social Security?

Yes, but it's a very narrow and serious path—not a financial strategy. A minister can apply for an exemption from self-employment taxes (the system that funds Social Security and Medicare) by filing IRS Form 4361.

This isn't a loophole to save money. The pastor must be conscientiously opposed to accepting public insurance for religious reasons. It has to be a deeply held belief, not a financial preference, and once the IRS approves it, the decision is permanent.

There’s a tight deadline, too. The application has to be filed by the tax return due date for the second year the minister earns at least $400 from ministerial work.

What's the Best Way to Keep Track of Restricted Funds?

Honestly, the only truly safe and reliable way is with a proper fund accounting system. Many churches try to make standard business software work using tags or classes, but these are just patches. They're clunky, prone to human error, and can put your church in a risky position if funds get mixed up.

A purpose-built system is always the better road. The accounting platform Grain Ledger is built on a foundation of true fund accounting. That means it’s designed to automatically separate funds the moment a designated donation comes in. It talks to your giving platform and produces financial reports that show exactly where every restricted dollar is. This approach isn't just about good bookkeeping; it's about integrity, preventing the accidental misuse of gifts, and maintaining the trust you've built with your givers.

Ready to bring clarity and integrity to your church's finances? Discover how Grain Ledger’s true fund accounting can simplify compliance and empower your stewardship. Learn more and Schedule a Demo.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.