A Guide to Accounting for Churches

Master accounting for churches with this practical guide. Learn fund accounting, internal controls, and reporting to ensure faithful financial stewardship.

At its heart, church accounting is a specialized world. It’s all about managing money with an intense focus on stewardship and transparency. The biggest piece of the puzzle is tracking donor-restricted funds separately from the money used for general operations.

Unlike a typical business chasing profit, a church's financial goal is accountability. Every donation needs to be tracked to ensure it’s used exactly as the donor intended. This builds the trust that is the lifeblood of any ministry.

Why Church Accounting Is Different

Let's get one thing straight: accounting for a church is fundamentally different from accounting for a business. A for-profit company lives and dies by its net income. A church, on the other hand, tracks its funds to prove it's being a faithful steward of the resources entrusted to it. The goal isn't to make money; it's to responsibly manage those resources for the congregation and the community it serves.

This isn't just a philosophical talking point—it changes everything about how the books are kept.

Think of it like managing a set of digital savings jars. You have one jar for general tithes and offerings that cover daily expenses like salaries and utility bills. Then you have another jar labeled "Building Fund" holding donations specifically for that new roof project. A third might be for "Missions Outreach." You simply can't dip into the building fund jar to pay the light bill, even if you’re running a little short. Each fund is its own separate financial entity.

Key Differences Between For-Profit and Church Accounting

To truly grasp the distinction, it helps to see the core differences side-by-side. While both use debits and credits, their language, goals, and the stories their reports tell are worlds apart.

| Aspect | For-Profit Business Accounting | Church Fund Accounting |

|---|---|---|

| Primary Goal | Maximize profit for shareholders. | Demonstrate stewardship and accountability to donors and the congregation. |

| Key Metric | Net Income / Profitability | Compliance with donor restrictions and mission fulfillment. |

| Terminology | Revenue, Expenses, Equity | Contributions, Expenses, Net Assets (often split by restriction). |

| Financial Statements | Income Statement, Balance Sheet, Statement of Cash Flows | Statement of Activities, Statement of Financial Position, Statement of Cash Flows. |

| Stakeholders | Investors, Lenders, Management | Donors, Congregation, Board/Elders, Granting Organizations. |

This table shows why you can't just apply standard business accounting principles to a church and expect it to work. The entire framework is built on a foundation of trust and purpose, not profit.

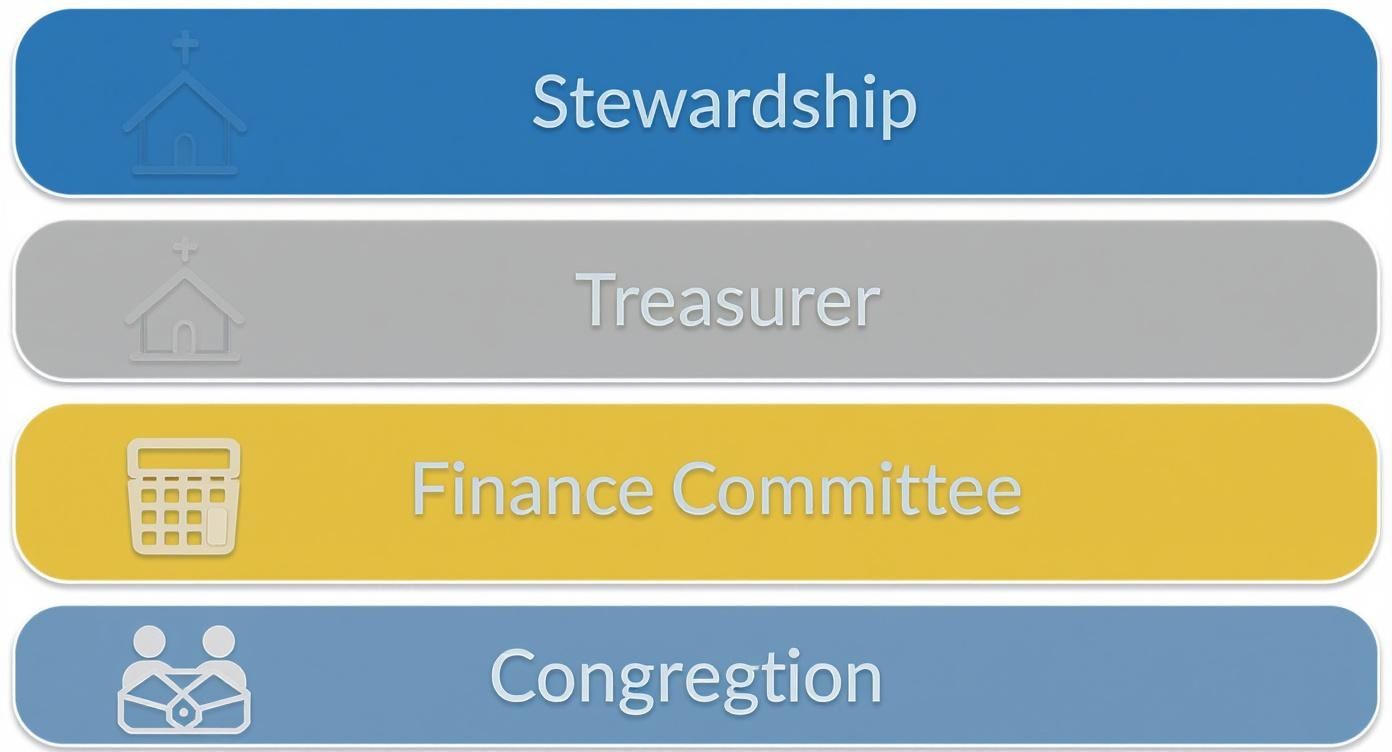

The People Behind the Numbers

A healthy church financial system isn't run by one person. It's a team effort, with different people playing crucial roles to ensure integrity and accountability.

- The Treasurer: Usually a dedicated volunteer, this person is the hands-on steward of the church's finances. They’re the ones paying the bills, making deposits, and putting together the initial financial reports.

- The Finance Committee: This group is the essential oversight layer. They review the budget, dig into financial statements, and help the leadership make smart, long-term decisions. Think of them as the treasurer's accountability partner.

- The Congregation: As the ones giving the funds, the congregation deserves total transparency. Clear, easy-to-understand financial reporting gives them confidence that their contributions are being managed wisely.

Stewardship is the moral and financial bedrock of church finance. It’s about accountability to both the donors and the mission, ensuring that every dollar accomplishes its intended purpose with integrity.

The need for better financial tools in this space is growing fast. The global Church Accounting Software Market, currently valued at around USD 2.85 billion, is expected to more than double to USD 5.95 billion by 2033. This isn't just a random statistic; it shows a massive shift toward specialized systems designed to handle the unique quirks of fund accounting and keep churches compliant. You can discover more about the growth of this market and what it means for financial management.

In the end, what makes church accounting unique is that it's built on trust, clear communication, and unwavering integrity. It’s so much more than balancing the books; it’s about honoring the faith and generosity of every single person who supports the mission.

Building Your Church Chart of Accounts

If fund accounting is the language your church uses to tell its financial story, then the Chart of Accounts (COA) is its alphabet. It's so much more than a list of categories; it’s the entire framework that organizes every dollar coming in and going out, making sure everything is tracked with total clarity. A solid COA brings logic and transparency to your church's finances.

Think of it like the shelving system in a library. Without clear labels for "Fiction," "History," and "Science," finding a specific book would be a nightmare. In the same way, without a well-organized COA, tracking income and expenses becomes a jumbled mess. You simply can't see the true financial health of your ministries. The goal is to build a system where every number has a home.

This structure is crucial for the leaders entrusted with the church's resources, from the congregation's initial giving to the financial oversight from the treasurer and finance committee.

A clear Chart of Accounts is the primary tool that allows the treasurer and finance committee to properly steward the congregation’s gifts and report back accurately.

The Five Pillars of Your COA

Every COA, no matter the size of the church, is built on five core account types. Getting these pillars right is the first step to building a system that really works for you.

Assets: This is everything the church owns. It includes the cash in your bank accounts, the church building and land, equipment, and even investments.

Liabilities: This is what the church owes to others. Think mortgages, outstanding loans, or accounts payable (those bills that have arrived but haven't been paid yet).

Net Assets (or Equity): This is the difference between what you own (Assets) and what you owe (Liabilities). In church accounting, this is where your funds live—like your Unrestricted Fund for general operations and various Restricted Funds for things like missions or a new building.

Income (Revenue): This is all the money coming in. The main source is usually tithes and offerings, but it also includes things like designated gifts for a specific project or rental income from the fellowship hall.

Expenses: This tracks all the money going out to run the church and its ministries. Common expenses are salaries, utilities, curriculum for the youth group, and building maintenance.

Structuring Your Accounts for Fund Tracking

The real magic happens in how you structure your COA. The most practical approach is using a numbering system that groups similar accounts together. A simple, logical system might assign a specific number range to each of the five pillars.

A well-structured Chart of Accounts does more than just organize transactions; it builds the framework for accountability. By integrating fund tracking directly into your account numbers, you create a system where financial transparency is the default, not an afterthought.

Here’s a common way to set it up:

- 1000s – Assets: (e.g., 1010 for General Checking, 1200 for Buildings)

- 2000s – Liabilities: (e.g., 2010 for Mortgage Payable)

- 3000s – Net Assets/Funds: (e.g., 3010 for Unrestricted Fund, 3020 for Building Fund)

- 4000s – Income: (e.g., 4010 for Tithes & Offerings, 4020 for Building Fund Donations)

- 5000s – Expenses: (e.g., 5010 for Pastor's Salary, 5100 for Utilities)

See how that works? Income and net asset accounts are tied directly to specific funds. When a $100 donation comes in for the building fund, it gets coded to account 4020. This simple act makes it incredibly easy to pull a report and see exactly how much money was given to that specific fund. This setup is the heart of effective accounting for churches.

This is just a starting point, of course. For a deeper dive with more complex examples, check out our complete guide on the chart of accounts for nonprofits.

Ultimately, your COA is a living document. It should be detailed enough to give you clear insight but simple enough for a volunteer treasurer to use without getting overwhelmed. Start with these foundational categories, and don't be afraid to add more detail as your church’s financial life grows.

Managing the Day-to-Day Flow of Church Finances

Having a solid Chart of Accounts is like having a good map, but the daily financial operations are the actual journey. This is where stewardship gets real. Consistent, well-documented routines for handling the money coming in and going out are what make or break your church's financial integrity. These daily habits are the foundation of trustworthy accounting, turning good intentions into solid practice.

Think of it like running a kitchen. You need a clear process for everything, from receiving ingredients to sending out finished plates. For a church, that means having a set way to collect the offering, pay the bills, and handle payroll. Without that clear roadmap, you're inviting errors, confusion, and a breakdown of the very trust your congregation places in you.

Workflows for Offerings and Deposits

Handling tithes and offerings is probably the most visible—and sensitive—financial task in any church. A disciplined, transparent process here isn't just a good idea; it's non-negotiable for keeping the trust of your members.

The absolute best practice involves having at least two unrelated people handle the collection and counting. This "two-person rule" is a cornerstone of internal controls. It protects the church’s money, and just as importantly, it protects the volunteers handling it from any potential suspicion.

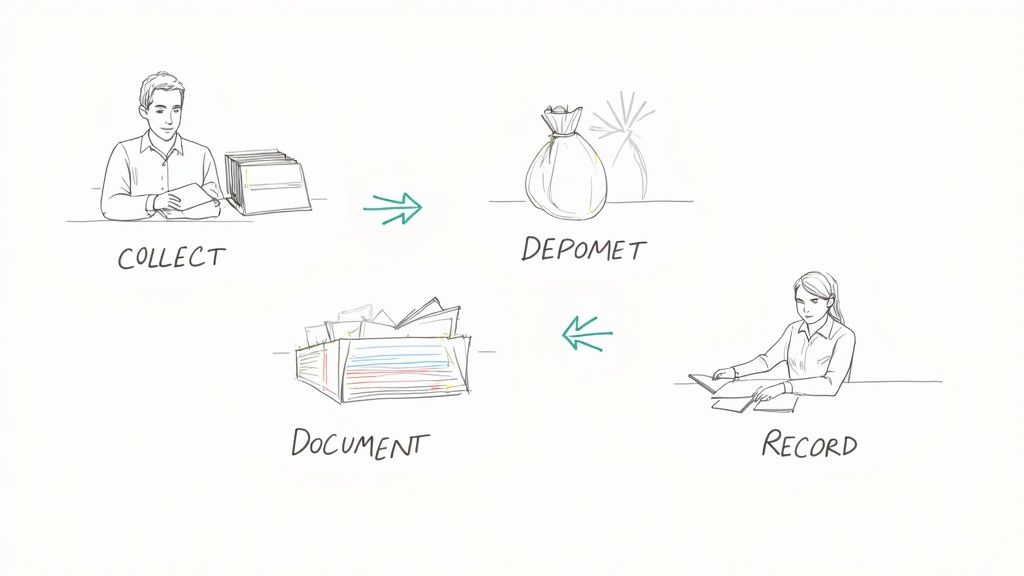

Here’s a straightforward workflow you can put in place this Sunday:

- Secure the Collection: Two or more designated counters gather the offering plates or donation boxes.

- Count Together: They immediately go to a secure room to count the cash and checks together.

- Document Everything: Using a detailed count sheet, they list the cash totals and each individual check. Both counters sign and date the form to confirm the amount is accurate.

- Prep the Deposit: One person prepares the bank deposit slip, making sure the total exactly matches the count sheet. No exceptions.

- Deposit Promptly: The funds go into a locked bag and are taken to the bank as soon as possible. A copy of the bank's deposit receipt is then stapled to the original count sheet and filed away.

A documented, consistent offering process is your first line of defense in financial stewardship. It removes ambiguity, protects volunteers from suspicion, and creates an unimpeachable record of every gift received.

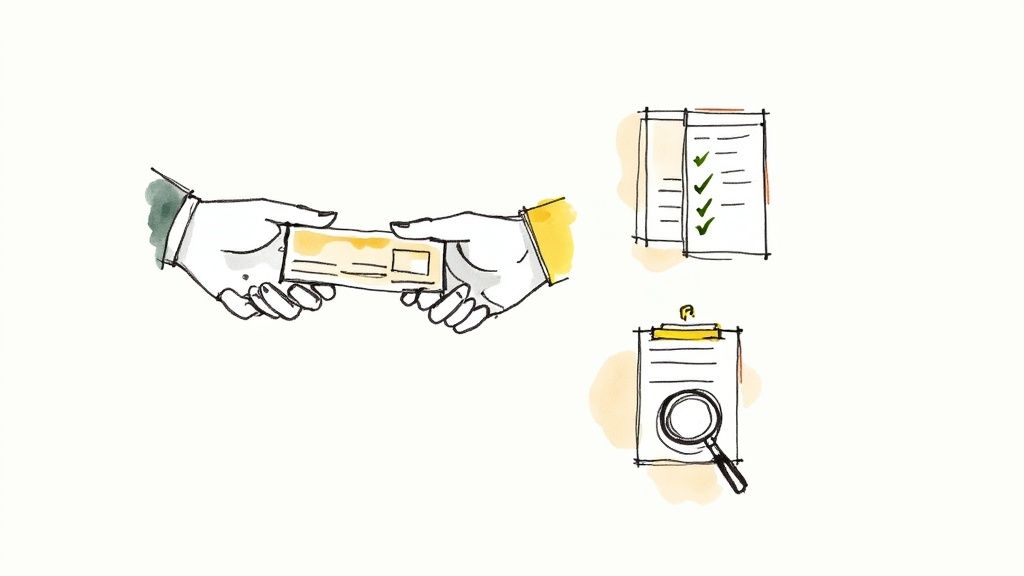

Processing Ministry Expenses and Payments

Just as crucial as tracking the money coming in is managing the money going out. Every single payment, whether it's for the light bill or for the new curriculum for the youth group, needs to be properly authorized and recorded. This stops unapproved spending in its tracks and ensures every dollar is booked to the correct fund.

Even in a small church, a simple purchase order or check request system works wonders. Before anyone writes a check, a form should be filled out explaining what the expense is for, its ministry purpose, and which budget it should come from. This creates a fantastic paper trail. Another great control is requiring two signatures on checks above a certain amount, like $500.

Managing Clergy Payroll and Housing Allowances

For most churches, payroll is the biggest line item in the budget, and it has its own unique wrinkles—especially when it comes to clergy. The pastor housing allowance is a huge tax benefit, but you have to administer it by the book to stay compliant.

The housing allowance lets an ordained minister receive a portion of their income tax-free for housing expenses. To do it right, your church must:

- Make it Official: The church board has to formally designate the housing allowance amount in writing before the calendar year begins.

- Keep it Reasonable: The allowance can't be more than the fair rental value of the home (furnished, plus utilities) or the pastor’s actual housing expenses—whichever is less.

- Report it Accurately: The allowance amount is noted on the pastor's W-2 form but isn't subject to federal income tax.

Getting the housing allowance wrong is a common mistake that can cause major tax headaches for your pastor. Proper documentation and following IRS rules are absolutely critical for everyone involved.

The principles of good stewardship are universal, but their application is global. With approximately 2.54 billion Christians worldwide, these financial practices are constantly adapting. As church communities grow, especially in regions like Africa and Latin America, financial leaders have to navigate a wide array of regulations and digital tools. Explore more about the state of church membership and what it means for finances.

Getting Financial Reports Everyone Can Understand

All your church's financial data is just a pile of numbers until you shape it into clear, useful reports. This is where the daily work of bookkeeping truly pays off, telling the real story of your church's financial health to your leadership, finance committee, and congregation. Without these reports, you’re just guessing.

Good financial reporting is the ultimate expression of transparency in church accounting. It answers the questions that are on everyone's mind: Are we on solid ground? Are we honoring the intent behind every donation? Can we afford to launch that new ministry we've been praying about? Getting this right builds trust and leads to much wiser decisions.

There are three essential reports every church needs: the Statement of Financial Position, the Statement of Activities, and the Statement of Cash Flows. Each one gives you a different, crucial view of your finances.

The Statement of Financial Position

Think of the Statement of Financial Position as a financial snapshot—a clear picture of your church's health on one specific day. It’s the nonprofit world’s version of a business balance sheet and boils down to a simple, powerful formula:

Assets = Liabilities + Net Assets

This report lays out what your church owns (Assets like cash in the bank or property), what it owes (Liabilities like a mortgage or outstanding bills), and what’s left over (Net Assets). Most importantly, this is where your fund balances are broken down clearly. A properly prepared statement will list the balance for your general unrestricted fund right next to every single restricted fund, whether it's for the building, missions, or youth camp.

Seeing these balances side-by-side is a game-changer. It lets your board know that even if the general fund is running low, the building fund has a healthy balance that can't be touched for operational needs. It prevents the accidental (and improper) use of restricted money.

The Statement of Activities

If the Statement of Financial Position is a snapshot, the Statement of Activities is the video. It shows your church's financial performance over a period of time—a month, a quarter, or a full year. This is your equivalent of an income statement, tracking all the money that came in and all the money that went out.

This is your go-to report for managing the budget. It answers critical questions like:

- Are tithes and offerings keeping pace with our budget?

- How much did we actually spend on the youth ministry last quarter?

- Did that special missions offering cover the entire cost of the project?

The real magic happens when you run this report by fund. Filtering the Statement of Activities to show only the "Building Fund" gives you a perfect record of every designated donation that came in and every single expense paid out from it. This creates an airtight audit trail and proves you’re stewarding donor funds exactly as promised.

A fund-based Statement of Activities is the cornerstone of accountability. It transforms a generic income and expense report into a powerful stewardship tool, proving that every restricted dollar was used exactly as the donor intended.

The Statement of Cash Flows

Finally, the Statement of Cash Flows tracks the actual movement of cash over a set period. It shows how cash entered your bank accounts and how it left, broken down into three main categories:

- Operating Activities: Cash flow from your primary ministry activities, like receiving offerings and paying staff salaries.

- Investing Activities: Cash used for buying or selling long-term assets, such as a new property, a vehicle, or sound equipment.

- Financing Activities: Cash from things like taking out a loan or making principal payments on a mortgage.

This statement is vital for managing your church's liquidity—its ability to pay the bills. A church can look profitable on the Statement of Activities but still face a cash crunch. This report helps you see those problems coming and avoid nasty surprises.

For a deeper dive into putting these documents together, you can find detailed guidance on essential financial reports for churches to help your team tell your financial story with complete clarity.

7. Putting Guardrails in Place: Internal Controls to Protect Your Church

Let's be clear: implementing internal controls isn't about a lack of trust. It's an act of profound stewardship. These procedures are your church's financial guardrails, protecting its resources from honest mistakes and, in rare cases, intentional misuse. For the dedicated people handling the money, these controls are a shield, removing any shadow of suspicion.

Think of it this way—you wouldn't leave the church doors unlocked overnight. Internal controls apply that same common sense to your finances. They are the practical locks and safeguards that ensure every dollar is handled with integrity, accountability, and transparency. This is a non-negotiable part of responsible accounting for churches.

The Cornerstone of Control: Separation of Duties

The single most effective internal control you can put in place is the separation of duties. At its core, this just means that no one person should have control over a financial transaction from start to finish. When one individual handles too much, it creates a massive blind spot where errors or even fraud can go completely unnoticed.

Breaking up these responsibilities is much easier than it sounds. Here’s a look at the key tasks to separate:

- Counting vs. Recording: The people who count the weekly offering should never be the same people who record the deposits in the accounting software.

- Approving vs. Paying: The person who gives the green light on an expense (like a ministry leader or pastor) should not be the one who signs the check to pay for it.

- Writing vs. Reconciling: The individual who writes checks must be different from the person who reconciles the bank statement at the end of the month.

This simple separation creates a natural system of checks and balances. With multiple sets of eyes on the process, it's highly likely that any discrepancy will be caught almost immediately.

Practical Controls Every Church Can Use

Beyond separating duties, a few other straightforward controls can dramatically boost your church's financial security. These aren't complicated procedures that require a CPA; they are simply good habits that build a culture of accountability.

Internal controls are the practical application of good stewardship. They are the policies and procedures that ensure a church's financial operations are transparent, accountable, and aligned with its mission, protecting both its resources and its reputation.

Consider making these essential practices your standard operating procedure:

Require Dual Signatures: For any check over a set amount (say, $500), require signatures from two authorized, unrelated people. This simple step prevents any single person from making large, unauthorized payments.

Conduct Independent Bank Reconciliations: Every month, the bank statement should be opened and reconciled by someone who has no check-signing authority or responsibility for recording transactions. This is a perfect job for a finance committee member or another trusted volunteer. You can learn more about who does what in our guide to church finance committee responsibilities.

Secure Your Offering Collections: Always have at least two unrelated people present when counting and documenting the offering. Both individuals should sign off on the final count sheet before it's handed off to the bookkeeper.

Use a Check Request System: Create a simple form that ministry leaders must fill out to request a payment. This form should explain the expense, its purpose, and the budget line it comes from, creating a clean paper trail for every dollar spent. It formalizes the approval process and ensures all spending is properly authorized.

Steering Clear of Common Church Accounting Pitfalls

Even with the best intentions, financial mistakes are bound to happen. When it comes to accounting for churches, a few specific errors tend to pop up again and again, usually because nonprofit finance has its own unique quirks. Getting ahead of these common pitfalls is a vital part of good stewardship—it protects your church's money, its reputation, and its legal standing.

These aren't just small bookkeeping slip-ups. They can snowball into serious compliance headaches, create confusion among your members, and erode the very trust you’ve worked so hard to earn. By knowing where things often go sideways, you can build smarter processes to keep your financial house in order.

Misclassifying Restricted and Designated Funds

One of the biggest and most common mistakes is mixing up restricted and designated funds. They might sound alike, but from a legal standpoint, they're worlds apart. Confusing them can lead to some serious problems.

- Restricted Funds: Think of these as gifts with legally binding strings attached. A donor gives money specifically "for the new roof," and the church has no choice but to use it for that exact purpose.

- Designated Funds: These are general, unrestricted donations that the church leadership chooses to set aside for a project, like a future missions trip. Because the board made the decision, they can also change it if ministry priorities shift.

The trouble starts when designated funds are treated as if they're legally restricted, which ties the church's hands unnecessarily. Even worse is when truly restricted funds get spent on general operating costs. That’s a breach of donor trust and can land the church in legal hot water. A well-organized Chart of Accounts and crystal-clear documentation for every major gift are your best defense here.

Improperly Handling Clergy Compensation

Clergy payroll can feel like navigating a minefield, especially when it comes to the pastor’s housing allowance. It’s a fantastic tax benefit for ministers, but the IRS has very specific rules you have to follow to the letter. Getting this wrong is a huge compliance risk.

The most common error we see is the church failing to formally designate the housing allowance in writing before the year begins. A handshake deal or a retroactive board vote won't cut it. To be compliant, it has to be documented in advance.

To stay on the right side of the rules, make sure your board passes a formal resolution every single year to approve the housing allowance. This decision must be recorded in the official meeting minutes before January 1st. Remember, the allowance can’t be more than the pastor's actual housing expenses or the fair rental value of their home—whichever is less. There's no room for guesswork here; diligent records are absolutely essential.

Failing to Track Designated Gifts Accurately

Beyond big capital campaign donations, your church probably receives smaller gifts meant for specific ministries—the youth group, the food pantry, or a particular missionary you support. A classic mistake is to just lump these donations into the general offering, where their original purpose gets lost in the shuffle.

This isn't just about sloppy bookkeeping; it dishonors the donor's wishes and makes it impossible to know if a ministry actually has the funds it was given. The fix is a straightforward, consistent process:

- Use giving envelopes or online donation forms that let people clearly mark where they want their gift to go.

- Train your offering counters to pull out and tally these designated gifts separately from the general fund donations.

- Enter each designated gift into its own income account in your accounting software.

This simple discipline ensures that when someone gives $50 to the youth camp fund, that money is set aside and ready to be used for exactly that. It’s a powerful way to maintain transparency and honor every single gift, big or small.

Your Top Church Accounting Questions, Answered

When you're managing church finances, a lot of the same questions tend to pop up. Let's tackle some of the most common ones head-on, giving you the clear answers your team needs to move forward confidently.

We're a Small Church. Do We Really Need Special Software?

You can certainly get by with spreadsheets for a while, but even for a small congregation, I’d strongly recommend dedicated church accounting software. Here’s why: it’s built from the ground up for fund accounting.

This means it's designed to track restricted gifts and automatically create the kinds of reports that nonprofits need. That built-in structure dramatically cuts down on the manual errors that creep into spreadsheets, saving you headaches and improving accuracy as your church grows.

What’s the Big Deal About "Restricted" vs. "Designated" Funds?

Getting this right is absolutely crucial for maintaining trust and staying compliant. The difference is all about who made the decision.

Restricted Funds: A donor gives money with a legally binding string attached. For example, they write a check with "for the new roof" in the memo line. Your church is legally obligated to use that money only for the roof.

Designated Funds: The church board or leadership decides to set aside money from the general fund for a specific purpose, like a future mission trip. Since the board made the decision, they can also change it if ministry priorities shift.

Think of it this way: a donor's restriction is a legal command. The board's designation is an internal intention. Confusing the two can get you into hot water fast.

How Do We Account for Donations That Aren't Cash?

These non-cash gifts, often called "in-kind donations," need to be recorded at their fair market value on the day you receive them.

If someone donates a used van, you'd look up what similar vans are selling for to determine its value. If you receive a gift of stock, its value is whatever the market price was on the day of the transfer. It's smart to have a clear, written policy for how you value these gifts. This keeps your financial records accurate and ensures you can give donors the proper acknowledgment they need for tax purposes.

Ready to bring true fund-based accounting to your ministry? Grain is built from the ground up to handle the unique financial needs of churches like yours. Unify your giving, banking, and bookkeeping to ensure every dollar is tracked to its purpose with complete transparency. Join the waitlist to be first to experience reporting that speaks the language of church finance at https://www.grainledger.com.

Ready to simplify your church finances?

Join the waitlist for early access to Grain - modern fund accounting built for ministry.